Overview

- P&I Clubs announced rate adjustments for marine insurance

- Global marine insurance industry-wide trends

- Structure of marine insurance premiums

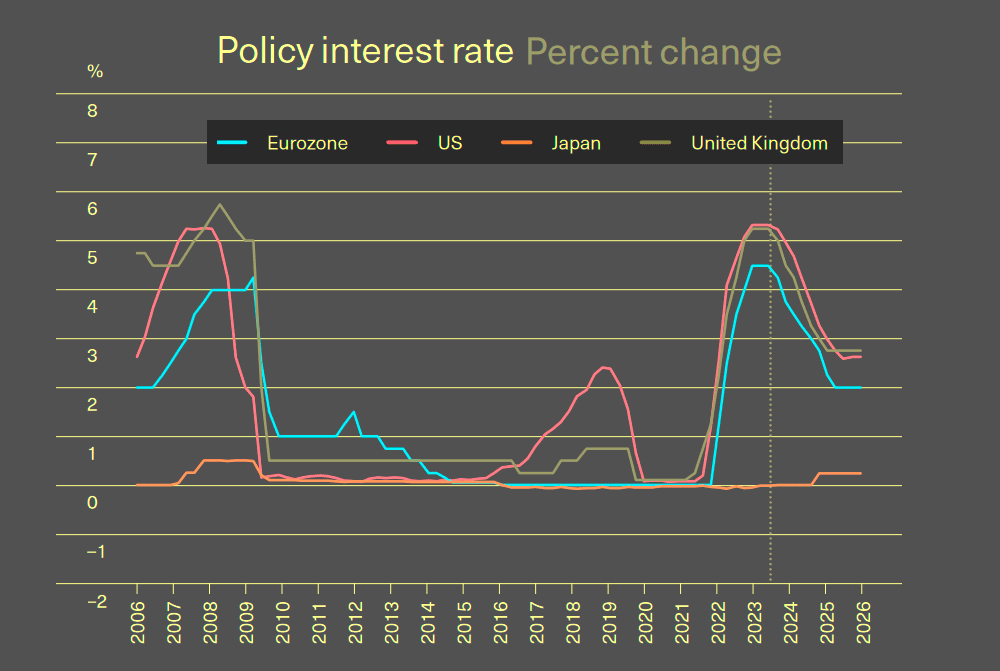

- Consumer prices and policy interest rate change

- American P&I Club adjusts rates for 2025

- Swedish P&I Club implements 5% rate increase

- London P&I Club targets 5% rate increase

Marine mutual insurers and P&I Clubs are planning rate hikes for 2025 year, driven by rising claims and inflation pressures. Marine mutuals are under growing pressure from inflation and increased claims severity, according to A.M. Best research. S&P Global Ratings expects most P&I clubs will achieve near-breakeven results in financial year 2025. Beinsure reviewed the reports and highlighted the key points.

Rate hikes and targeted adjustments aim to align premiums with rising risks, ensuring financial sustainability amid a volatile environment.

The 12 P&I clubs in the IG, which underwrites about 90% of the oceangoing fleet’s liability insurance globally, benefited from a low level of pool claims over the two past financial years (see Largest P&I Clubs Group).

IG members share claims of $10 mn-$100 mn under an excess-of-loss pooling arrangement. The historically low number of pool claims has improved operating performance in the P&I sector in financial years 2023 and 2024. In financial year 2025, however, the number of severe pool claims increased and will likely take a toll on clubs’ operating performance.

S&P expected an average combined ratio of 100-105% for financial year 2025. The average combined ratio was 95% in financial years 2024 and 2023.

Yet interim results from clubs that publish half-yearly reports suggest that the average combined ratio might deteriorate in financial year 2025.

The P&I insurance sector remains well capitalized. Many clubs hold surplus capital at the 99.99% confidence level, according to our revised risk-based capital model. Overall, capital levels have gradually recovered, supported by a strong underwriting performance over the past two years and robust investment returns.

That said, clubs’ significant capital levels could raise questions in the 2025 renewal period, considering subdued freight rates in the shipping sector. This decision arises from a resurgence in severe pool claims, which had been relatively low in the preceding two years. The uptick in claims is expected to push the average combined ratio—a key measure of underwriting profitability—to between 100% and 105%, indicating a potential underwriting loss for the sector.

P&I Clubs announced rate adjustments for marine insurance

- American P&I Club: Announced a 7% rate hike for 2025 to address inflation and claims trends.

- Swedish P&I Club: Implemented a 5% increase to manage premium adequacy and claims frequency.

- London P&I Club: Proposed a 5% rate hike citing inflation and severe claims, alongside adjustments tied to reinsurance program costs.

- UK P&I Club intends a 6.5% general increase across all premiums, accompanied by a 10% hike in deductibles, with a minimum increase of $1,000.

- Gard plans a 4% average increase and offers a 10% Owners General Discount for renewing members.

- NorthStandard has declared a 5% general increase for both mutual and fixed premium entries, including a minimum $1,000 deductible rise for all P&I deductibles below $30,000.

- West of England has set a 5% standard surcharge for mutual P&I entries, with no standard surcharge for Freight, Demurrage, and Defense (FD&D) risks, and deductibles remain unchanged.

These rate adjustments reflect the P&I Clubs’ efforts to maintain financial stability amid rising claims and evolving market conditions.

Shipping losses have sunk to the lowest number we have seen in the 12-year history of our annual study reflecting the positive impact safety programs, trainings, changes in ship design and regulation have had over time.

Fire and explosion incidents cause the most expensive insurance claims in the marine industry, while at a time of rising exposures and inflation, cargo damage is the most frequent cause of loss, according to AGCS’s Top Causes of Claims in Marine Insurance. Allianz analyzed more than 240,000 marine insurance claims worldwide, worth approximately €9.2 bn in value, and has identified a number of claims and risk trends that are driving major loss activity in the sector.

Inflation is another key concern for marine insurers and their policyholders as recent increases in the values of ships and cargos mean losses and repairs are becoming more expensive when things go wrong.

Global marine insurance industry-wide trends

The International Union of Marine Insurance reported that global marine insurance premiums in 2024 estimated $40 bn, a 6% increase from 2022. This growth was driven by a rise in global trade volumes and values, increases in vessel values, and heightened activity in the offshore energy sector due to higher oil prices.

However, the claims environment was relatively moderate in 2024, with no major weather events or vessel casualties significantly impacting overall costs, despite a few major fires.

Large vessel fires, particularly on containerships and car carriers, remain a growing concern for hull and cargo insurers.

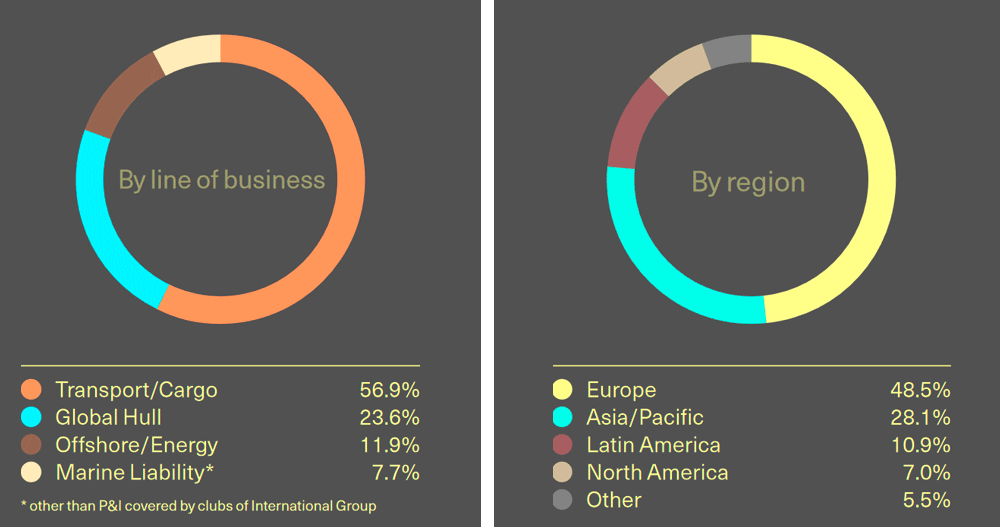

Structure of marine insurance premiums

- Ocean hull premiums were reported at ~$10 bn, up by 6.7% on the previous year. More activity, more vessels, rising values and reduced market capacity were responsible. Claims continued to be low resulting in positive loss ratios for nearly all regions.

- Premiums for cargo insurance reached ~$25 bn representing an 8.5% uptick on last year and continuing the trend for market development in this sector. This was on the back of a post-pandemic rebound in global trade. Loss ratios had returned to more normal levels, had started at their lowest point since 2015.

- The offshore energy sector continued its three-year run of premium base growth reporting ~$5 bn, an increase of 7.3%. The uptick in oil prices was largely responsible, translating into increased offshore activity and a rise in average day rates. Losses had remained relatively low and recent years’ loss ratios were currently positive.

Consumer prices and policy interest rate change

Consumer prices change

| Region | 2024 | 2025 | 2026 |

| World | 4.8 | 3.2 | 2.9 |

| United States | 3.0 | 2.1 | 2.7 |

| Canada | 2.9 | 1.9 | 2.0 |

| Brazil | 4.1 | 3.2 | 3.3 |

| Eurozone | 2.5 | 2.0 | 1.7 |

| United Kingdom | 2.5 | 2.3 | 1.7 |

| Russia | 5.9 | 5.0 | 4.4 |

| Mainland China | 1.0 | 1.7 | 2.0 |

| Japan | 2.3 | 1.9 | 1.6 |

| India | 5.1 | 4.9 | 5.5 |

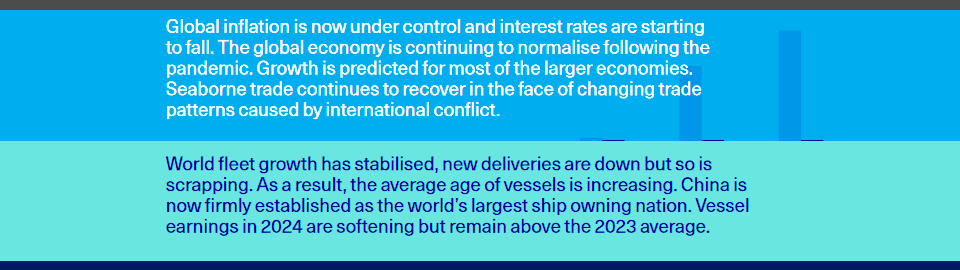

According to Global Marine P&I Sector report, year-on-year growth for the ocean carriage of cars has jumped by a massive 23% whereas the container trades appear to have shrunk by almost 4%. This is largely due to high inflationary pressures affecting consumer confidence. A 10.5% increase in coal trades is concerning in terms of global ESG ambitions.

The slowdown in global fleet growth has stabilised and is reported to be at 2.1% (gross tonnage) currently. New deliveries are down but so is scrap-ping activity.

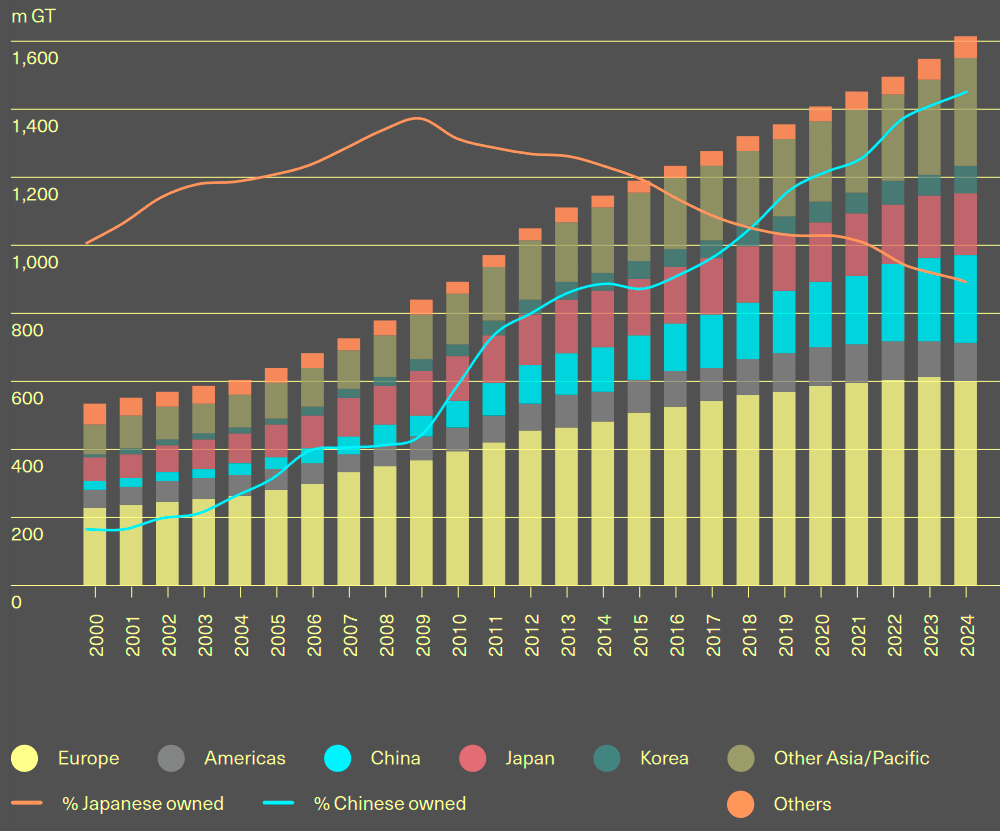

Long term regional fleet development

As a mutual insurance association, P&I clubs provide risk pooling, information and representation for members. P&I insurance covers risks that are not typically placed in the traditional insurance market.

Typical P&I cover can include a carrier’s third-party risks for damage caused to cargo during carriage, war risks, and risks of environmental damage such as oil spills and pollution.

P&I Clubs should adopt an analytical approach when seeking increases, rather than a unilateral approach. When working with organizations a more detailed analysis of each member’s risk profile hand-in-hand with the context of club performance and the marketplace is encouraged.

American P&I Club adjusts rates for 2025

The American Steamship Owners Mutual Protection and Indemnity Association (American Club) announced a 7% increase in expiring rates for all business classes in 2025. This adjustment reflects inflation and ongoing claims trends. The club noted that while the last renewal saw modestly lower premium and tonnage, premium income growth outpaced tonnage, improving relative premium rating levels.

The club stated that rising claims, inflation-driven people claims, and higher-value casualties in 2024 highlight the need for sustainable premium adjustments in an environment with long-tail liability exposures.

American Club noted its member-specific approach to renewals, assessing records, trade, and risk profiles when determining pricing and terms. Early higher-value claims in the 2024-2025 policy year exceeded expectations at both pool and retention levels. However, attritional exposures remained slightly below budget.

The club reserved judgment on whether these trends will persist, maintaining a 20% release call margin above estimated premiums for protection and indemnity (P&I) and freight, demurrage, and defense (FD&D) classes.

The American Steamship Owners Mutual Protection and Indemnity Association, known as the American Club, was established in New York in 1917. It is the sole mutual Protection and Indemnity (P&I) Club domiciled in the United States and the entire Americas.

As a member of the International Group of P&I Clubs, the American Club collaborates with twelve other mutuals to provide P&I insurance for approximately 90% of global shipping.

The club offers a range of services, including Protection and Indemnity insurance, Freight, Demurrage and Defense (FD&D) insurance, and insurance for charterers’ risks. It emphasizes personalized service and a proactive approach to meet the diverse needs of its members.

Swedish P&I Club implements 5% rate increase

The Swedish Club announced a 5% general rate increase for the 2025-2026 period. This measure addresses rising claims costs, premium adequacy, and portfolio balance. While its mutual P&I portfolio remained stable, the club observed a slight decline in tonnage offset by positive inflows earlier in the policy year.

Marine insurance claims frequency stayed consistent but included more large claims, particularly within the International Group of P&I Clubs, returning to expected levels after two benign years.

Inflationary pressures drove attritional claims above budgeted levels. Geopolitical tensions and market volatility may add further challenges.

The Swedish Club noted strong investment performance over the past two years, which bolstered its financial position. However, it remains cautious about market unpredictability and global economic shifts.

The Swedish Club, established in 1872 by shipowners, is a leading marine mutual insurer headquartered in Gothenburg, Sweden, with offices in Oslo, London, Athens, Hong Kong, and Singapore. It offers a comprehensive range of marine insurance products and services, including Protection and Indemnity (P&I) insurance, Freight Demurrage and Defence (FD&D) insurance, Hull and Machinery (H&M) insurance, and specialized covers such as Cyber insurance and Loss of Hire insurance.

As a member of the International Group of P&I Clubs, The Swedish Club provides full mutual P&I cover on a group basis, ensuring that its members’ legal and contractual liabilities concerning third parties incurred during the operation of entered ships are adequately covered.

London P&I Club targets 5% rate increase

The London Steam-Ship Owners’ Mutual Insurance Association, commonly known as the London P&I Club, is a leading provider of Protection and Indemnity (P&I) insurance, Freight, Demurrage & Defence (FD&D) insurance, and War Risks cover to shipowners and charterers worldwide. Established in 1866 and incorporated in 1875, the club has a long-standing history in the maritime insurance industry.

The London P&I Club proposed a 5% increase in average rates, citing inflation and a few higher-severity claims. While technical performance improved due to prior adjustments in rates and deductibles, concerns remain about claims severity and inflationary impacts.

The London Club plans to continue renewal terms based on individual member loss records and risk profiles, ensuring fleet rating and deductible levels remain equitable.

Adjustments related to the International Group’s excess loss reinsurance program costs, pending finalization, will also be applied.

In the 2023/24 financial year, the London P&I Club reported an operating surplus of $36.3 mn, increasing its free reserves to $149.8 mn. Gross earned premium rose by 4.5% from the previous year, with positive underwriting contributions across all product lines, resulting in a combined ratio of 83%. The club also achieved a strong investment return of $17.4 mn, equivalent to a 5% return.

The club insures a diverse range of shipowners and charterers, providing tailored solutions and flexible insurance packages to meet specific member needs. As a member of the International Group of P&I Clubs, the London P&I Club plays a key role in coordinating and promoting the collective strength of the P&I industry on behalf of the global shipowning community.

The club continues to focus on providing high-quality, responsive support to its members, emphasizing the importance of tailored solutions and flexible insurance packages to address the evolving needs of the maritime industry.

FAQ

Rate hikes are driven by rising claims and inflation. Increasing severity of claims and higher costs for ship repairs and cargo losses have forced insurers to align premiums with escalating risks.

Fire and explosion incidents generate the highest claim costs, while cargo damage remains the most frequent cause. Rising values of ships and cargo have amplified claim expenses, according to Allianz’s analysis of 240,000 claims worth €9.2 bn.

Inflation increases ship and cargo values, making claims and repairs more expensive. Insurers face higher costs to cover these rising exposures, impacting premium rates and financial stability.

In 2024, global marine insurance premiums reached $40 bn, a 6% increase from 2022. This growth stems from higher trade volumes, vessel values, and offshore energy activity. However, claims remained moderate due to fewer major weather events or casualties.

Cargo Insurance: Premiums grew to ~$25 bn in 2024, an 8.5% increase, driven by trade recovery post-pandemic.

Ocean Hull Insurance: Premiums rose by 6.7% to ~$10 bn due to vessel activity and reduced market capacity.

Offshore Energy: Premiums grew by 7.3% to ~$5 bn, fueled by higher oil prices and increased offshore activity.

P&I Clubs focus on member-specific risk profiles, historical records, and trade activity when determining rates. Analytical assessments ensure equitable solutions tailored to individual member needs while addressing financial sustainability and market conditions.