Overview

Despite the EU/G7 countries’ sanctions on Russian oil, a majority of vessels carrying Russian oil and oil products are owned and/or insured in the EU and G7 countries. Before the war, Russia was incredibly reliant on Western owned or insured tankers to transport Russian oil globally.

Despite the strong set of tools to cut revenues for the Kremlin’s war chest, EU/G7 countries have allowed the proliferation of the Russian oil trade by insuring tankers transporting Russian oil, according to CREA research.

Western insurers provides coverage for Russian tankers

Western insurers have provided coverage for Rosneft tankers transporting sub-sanctioned Russian crude. Despite the risks linked to the G7 price cap, which caused many in the trade sector to withdraw, some insurers continued their involvement, according to data from traders and shippers referenced by Reuters.

Five insurers, including American Club, West of England (based in Luxembourg), and Norway’s Gard, insured 10 tankers carrying Russian crude to Asia in 2024.

American Club and West of England insured two specific vessels, the Gioiosa and Orion I, which transported crude from Rosneft’s Baltic ports to China earlier this year (see How Many Insured Losses Drives the Francis Scott Key Bridge Collapse?).

Other insurers involved in covering Russian oil shipments include Maritime Mutual from New Zealand and London P&I Club, also an IG member. Both declined to comment on potential risks. The three non-profit mutuals, which provide ship insurance against oil spills, injuries, and fatalities, emphasized that they continue to serve their members’ needs.

The International Group (IG) of P&I Clubs, covering 90% of the global fleet, raised concerns in April about the flaws in the attestation process, warning it might expose members to price cap violations.

American Club, an IG member, stated that it lacked direct access to pricing information when it insured the Gioiosa. Gard reported that it relied on price cap attestations and also verified data (see about Risk Mitigation for Ukrainian Grain Exports in Global Insurance).

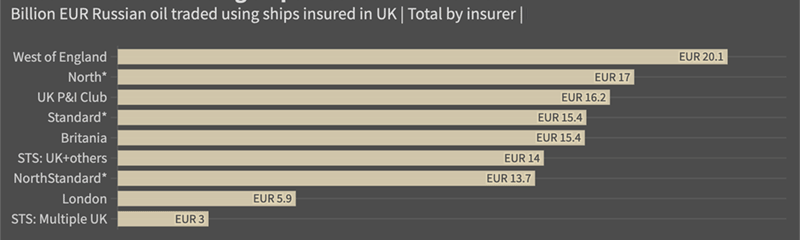

Russian oil tradet using ships insured in the UK

Western insurers’ ongoing involvement in specific Russian oil deals has remained underreported since the price cap’s implementation in 2022, following the start of the Ukraine war.

The G7 and its allies established the cap to limit Moscow’s war funding, allowing Western insurers and ships to participate only if the oil sells for under $60 per barrel.

Many who stopped trading such cargoes cited uncertainty about the insured oil’s price. Russia, which has prohibited its companies from adhering to the price cap, has sold Urals crude at an average of $69.4 per barrel at Baltic ports this year, according to LSEG data—well above the cap. Insurers and ship owners are not expected to investigate prices.

Global marine insurance premiums

According to Global Marine Insurance Market Review, marine insurance premiums totalled $35.8 bn an 8.3% uplift. European markets continued to enjoy growth whilst some Asian markets had slowed.

- Ocean hull premiums were reported at $8.4 bn, up by 5.7% on the previous year. More activity, more vessels, rising values and reduced market capacity were responsible. Claims continued to be low resulting in positive loss ratios for nearly all regions.

- Premiums for cargo insurance reached $20.5 bn representing an 8.3% uptick on last year and continuing the trend for market development in this sector. This was on the back of a post-pandemic rebound in global trade. Loss ratios had returned to more normal levels, had started at their lowest point since 2015.

- The offshore energy sector continued its three-year run of premium base growth reporting $4.1 bn, an increase of 7.3%. The uptick in oil prices was largely responsible, translating into increased offshore activity and a rise in average day rates. Losses had remained relatively low and recent years’ loss ratios were currently positive.

U.S. Treasury require insurers to obtain attestations

Western authorities, including the U.S. Treasury, require insurers to obtain attestations from buyers and sellers affirming that the oil sold below the price cap.

While there has been a decrease in insurance companies from the UK covering shipments of Russian crude, Russian oil still remains highly reliant on vessels insured in the UK for transport.

Russia is also heavily reliant on tankers that are owned or insured in countries that implement the oil price cap policy although this trend has decreased since Russia’s invasion of Ukraine.

62% of Russian oil products, chemicals, and liquefied petroleum gas (LPG) were carried on tankers owned or insured in countries that implement the price cap policy (see Shipping Safety & Key Risks for Marine & Cargo Insurance).

CREA’s analysis found that 33% of all Russian oil (by volume) was transported on tankers insured in the UKsince the sanctions were implemented until early November 2023. Ships insured in the UK transported EUR 3 bn of Russian oil products, with vessels shipping crude oil accounting for EUR 803 mn of the total.

The most important way to cut Russia’s export revenues will be to drive down the oil price cap and use their reliance on G7/EU insurance to do so.

Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

The movement toward stricter shipping measures

The movement toward stricter shipping measures is positive, but more actions are necessary to address violations and deter offenders.

The UK and Price Cap Coalition should require maritime insurers to verify, via bank statements, that oil prices were paid below the cap. This step would prevent the use of fraudulent documents to obtain Western insurance and enhance policy compliance.

Vessels owned or insured by G7 countries have continued to load Russian oil at all Russian ports, even when prices exceed the cap. These incidents clearly indicate violations of the price cap policy. However, there is limited public information on enforcement agencies imposing penalties on shippers, insurers, or vessel owners.

The UK Office of Financial Sanctions Implementation (OFSI) must investigate UK entities and insurers that facilitated the maritime transport of Russian oil above the cap. Sanctions must be imposed on firms that violate these rules and enable Russia to boost its oil export earnings, which in turn fund the war in Ukraine.

Penalties for violating the oil price cap remain insufficient. The UK and sanctioning countries should permanently ban maritime services for vessels that transport Russian crude without complying with the price cap.

The current 90-day ban on EU maritime services following a sanctions violation is too lenient. The UK’s enforcement agency can impose fines of up to GBP 1 mn or 50% of the breach’s value for violations of the price cap.

However, these penalties are weak compared to the value of tankers carrying crude oil, which often exceed GBP 100 mn.

by Yana Keller

by Yana Keller