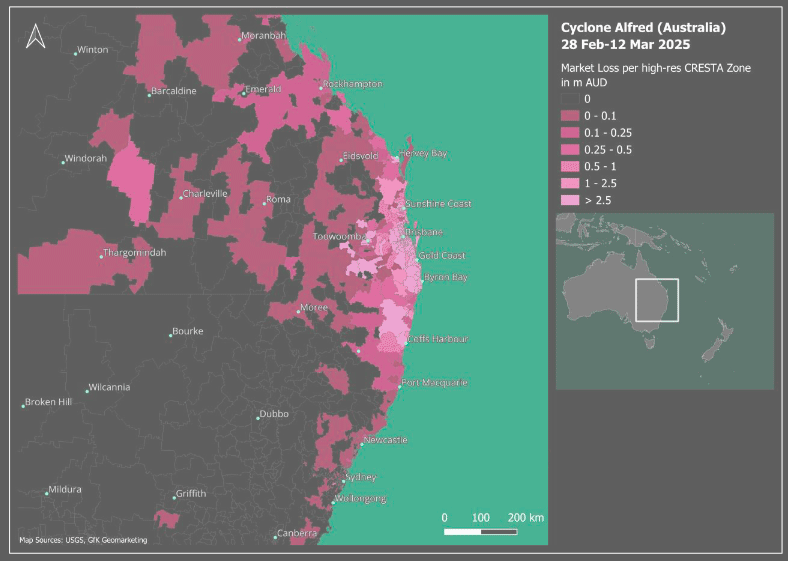

Zurich-based PERILS has lowered its industry loss estimate for Cyclone Alfred to AUD 1.92bn in its third report on the storm, which struck Queensland and New South Wales between Feb. 28 and Mar. 12, 2025.

The updated figure compares to prior estimates of AUD 2.57bn and AUD 2.25bn, released six weeks and three months after the event.

The loss estimate covers property and motor hull lines of business and reflects data gathered directly from affected insurers. According to PERILS, personal property claims account for 70% of the total, commercial property for 26%, and motor losses just 4%.

Cyclone Alfred reached peak intensity offshore as a Category 4 system before weakening to Category 1 at landfall near the Gold Coast on Mar. 7. Despite reduced wind speeds, the cyclone carried heavy tropical moisture that triggered prolonged rainfall and widespread flooding across Southeast Queensland and into northeastern New South Wales.

PERILS said the bulk of claims were rainfall-related rather than wind-driven. Darryl Pidcock, Head of Asia Pacific & Cyber at PERILS, noted that the fall in loss numbers compared with earlier estimates reflects both reduced claims volumes and cautious early reserving by insurers.

Since releasing our last loss report three months ago, we have observed a decrease in loss numbers and the number of claims provided by our insurance data providers, indicating cautious early reserving. Even though Alfred was a cyclone event, losses were primarily driven by intense and prolonged rainfall rather than by strong winds.

Darryl Pidcock, Head of Asia Pacific & Cyber at PERILS

“Personal property lines are the main contributor to the losses, followed by commercial lines property, and to a much smaller degree motor losses which only make up 4% of the total industry loss,” Darryl Pidcock said.

Pidcock added that the event provided valuable insight into vulnerabilities in southern Queensland and northern New South Wales, regions not typically exposed to tropical cyclone impacts.

Losses further south in New South Wales were largely flood-related, with lingering rains continuing to drive damage days after landfall.

The latest industry footprint includes postcode-level breakdowns of losses by line of business, combined with PERILS’ exposure database to help insurers refine their flood and wind risk models. A fourth and final update will be released on Mar. 12, 2026, marking one year since the event.

Cyclone Alfred built its strength offshore, lingering in the Coral Sea for several days as it edged south toward the Queensland coast.

At its peak intensity over water, it reached Category 4 status, carrying both strong winds and vast amounts of tropical moisture. By the time it came ashore near the Gold Coast on March 7, 2025, the cyclone had weakened to Category 1 in terms of wind speed, but the real danger came from the rain it dragged inland. Prolonged and heavy downpours saturated southern Queensland and spilled into northeastern New South Wales, causing extensive flooding across communities that rarely experience tropical cyclone conditions.

Unlike the violent windstorms often associated with landfalling cyclones, Alfred’s footprint was defined by water damage. Rivers swelled beyond capacity, flash floods swept through urban and semi-rural areas, and homes and businesses faced weeks of disruption.

The unusual southward track of Alfred also made it stand out, hitting regions more accustomed to temperate storms than tropical systems. For many residents, the flooding was compounded by lingering rainfall even after the cyclone had dissipated, keeping floodwaters high and extending the duration of loss events.

Insurance data showed that most claims originated from personal property—damaged homes, lost possessions, and flooded residences—while commercial properties faced interruptions and structural damage. Motor vehicles, although affected, represented only a small fraction of the total losses.

For insurers and reinsurers, Alfred became a case study in how tropical systems can deliver devastating impacts far from their usual corridors, especially when heavy rainfall lingers over populated areas.

The cyclone also highlighted gaps in preparedness, with infrastructure and communities in southern Queensland and northern New South Wales less familiar with managing cyclone-related floods.

For the insurance industry, Alfred reinforced the need for better flood modeling and resilience planning, since the event demonstrated that even relatively weak cyclones at landfall can generate billion-dollar losses when rainfall is intense and prolonged.