The insurance sector faces a new playbook. Verisk set the modeled global average annual insured property loss at $152bn for 2025, warning that industry exposure may run far higher.

Natural catastrophe events once considered freak outliers now shape the baseline, according to Verisk’s’ Modeling Insured Catastrophe Losses: A Global Perspective for 2025.

Rob Newbold, president of Verisk Extreme Event Solutions, said the data captures a fundamental shift in risk. Frequent, geographically broad perils drive sustained heavy losses. Insurers must adapt strategies or fall behind.

This year’s modeled losses reflect a fundamental shift in the risk landscape. Frequency perils are driving sustained, high-impact losses across geographies, and insurers must evolve their strategies to meet this challenge head-on

Rob Newbold, Verisk Extreme Event Solutions President

Fueling this surge: inflation, rapid development in hazard-prone zones, and climate change. Exposure climbed 7% a year between 2019 and 2024, with climate effects layering on an extra 1% annually.

In North America, insured claims make up nearly half of economic losses. Wildfire risk keeps climbing, aggravated by droughts and urban creep into fire-prone corridors.

Verisk said California’s wildland-urban interface added 240,000 homes from 2010 to 2020. The U.S. overall saw homes lost to wildfire double from 1990 to 2020.

Europe and Oceania aren’t immune. Urban growth and inflation lifted exposures more than 8% in some pockets. Severe thunderstorms dominate the model, now 42% of frequency peril share. Cyclones take 25%, earthquakes 10%, winter storms 8%, flood and wildfire about 7% each.

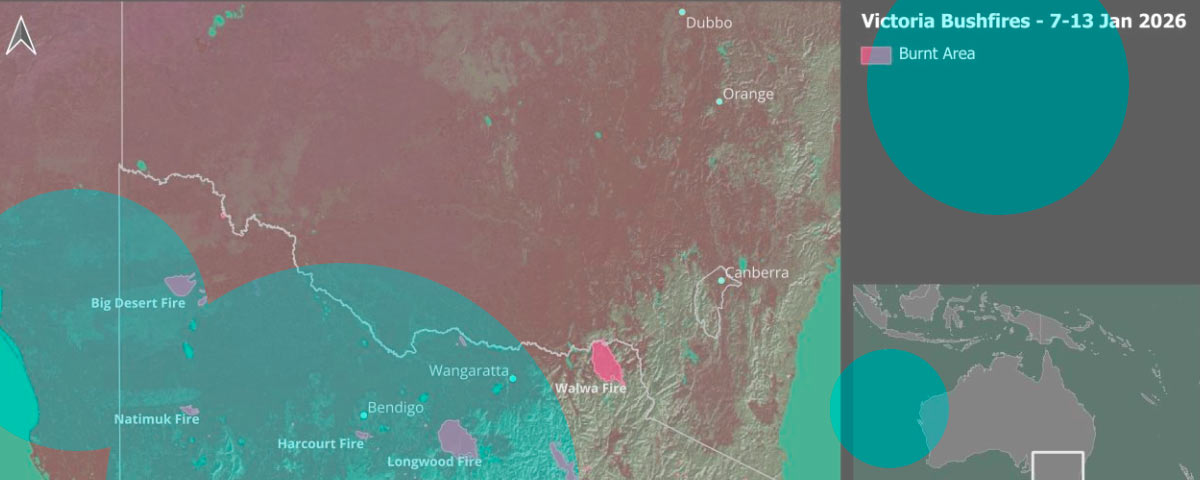

Fresh disasters underline the math. The Eaton and Palisades fires in Los Angeles, plus Hurricane Helene’s flooding, delivered losses rarely seen in decades. Verisk called the California fires equivalent to a 35-year return period, with damage striking high-value neighborhoods.

This is especially critical given recent events such as Hurricane Helene’s devastating flooding and the destruction caused by the Eaton and Palisades fires” in Los Angeles in January, said Verisk.

From 2020 to 2024, severe thunderstorm events spiked 59%. Analysts admit the science can’t yet pin down exact drivers. Some trends echo expected late-century climate impacts, others appear tied to ocean-atmosphere variability. The scale, though, is bigger than models once suggested.

Verisk closed its outlook with a blunt note: recent activity sharpened understanding of frequency peril risk corridors.

That clarity comes with a cost. Insurers now carry a world where volatility looks less like exception, more like rule.