Overview

The low interest rate years were challenging for people trying to save for retirement. Low rates made savings products and life insurance less appealing, and real savings growth of 1.1% in the pre-Covid-19 decade lagged behind economic growth. At the same time, the responsibility for retirement savings is shifting to individuals as traditional systems face funding issues.

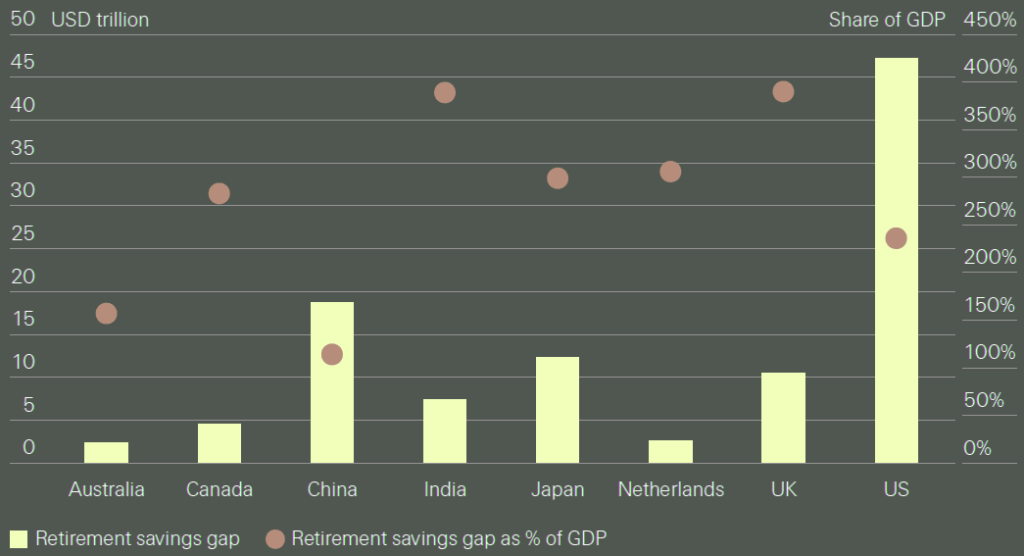

Swiss Re Institure estimate a retirement savings gap of USD 106 trillion in 2022 for six advanced economies, plus China and India.

Higher rates increase demand for life and annuity products by boosting investment yields and improving crediting rates on savings products, while gradually enhancing the pricing of protection business.

According to Outlook for Life Insurance, with life insurers managing an estimated USD 6 trillion in pension funds, the industry is set to play a key role in closing the retirement gap in the future.

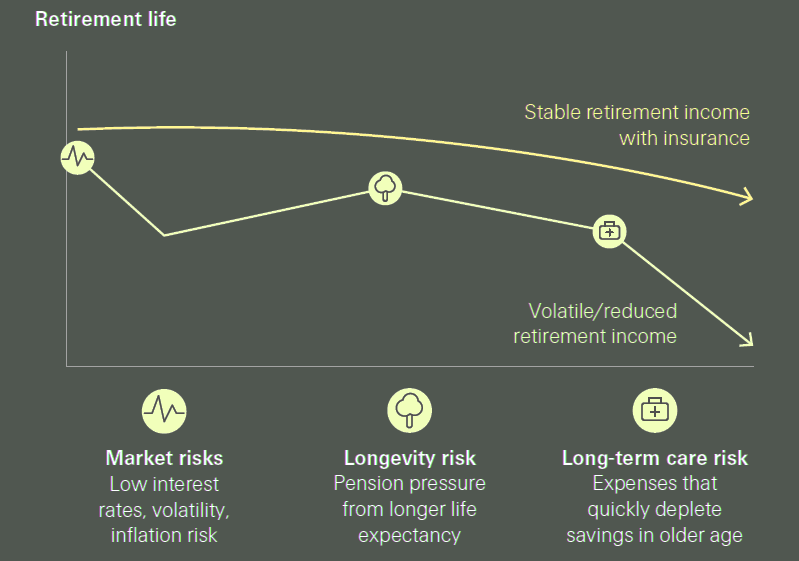

Life insurance provides products for retirement

The low-interest rate years were challenging for individuals looking to finance their retirements with products like annuities. Savings business is a core area for life insurers, but annual premium growth slowed significantly after 2010, with an average annual real growth rate of only 1.1% globally. The low-interest rate era made savings business less attractive, especially in Europe, where there was zero real growth.

The retirement savings market needs to evolve as the role of governments and employers in pension provision declines.

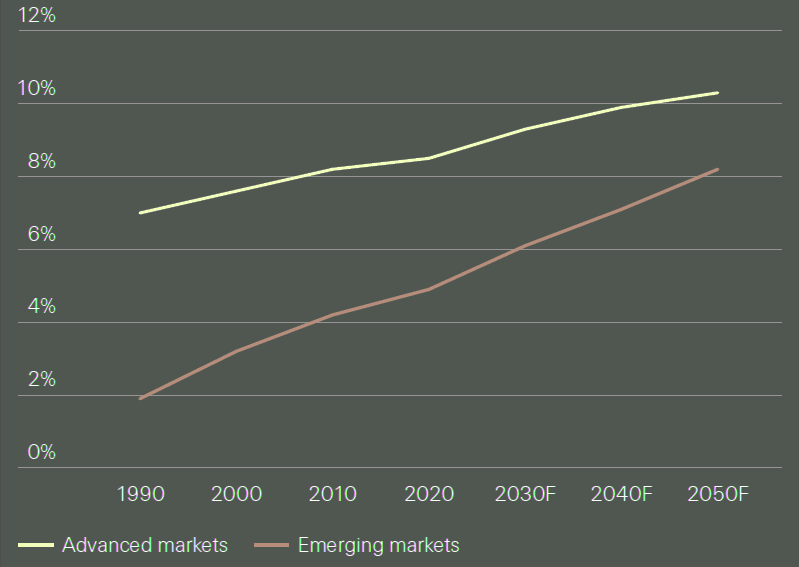

Aging populations challenge the funding of pension systems, as a smaller working-age population must support a growing number of retirees. Public spending on pensions is rising quickly as populations age.

In response, many governments are reforming pension systems to manage future public spending. These reforms include raising the retirement age, reducing benefits, and transferring funding risks to individuals.

For example, France and the Netherlands have recently increased the legal retirement age, and China is considering the same, according to Global Life Insurance Industry report.

Public pension spending of GDP

Higher interest rates improve the outlook for life insurers. Demand for savings-related products is surging, with US fixed annuity sales in 2023 more than twice as high as in any other year other than 2022. Insurers expect record sales in 2024 too (see Life Insurance & Retirement Savings Forecast for the U.S. & Europe).

Profitability is improving as well, with greater room for margins in new spread-based products and opportunity to reinvest assets backing legacy liabilities at a higher rate.

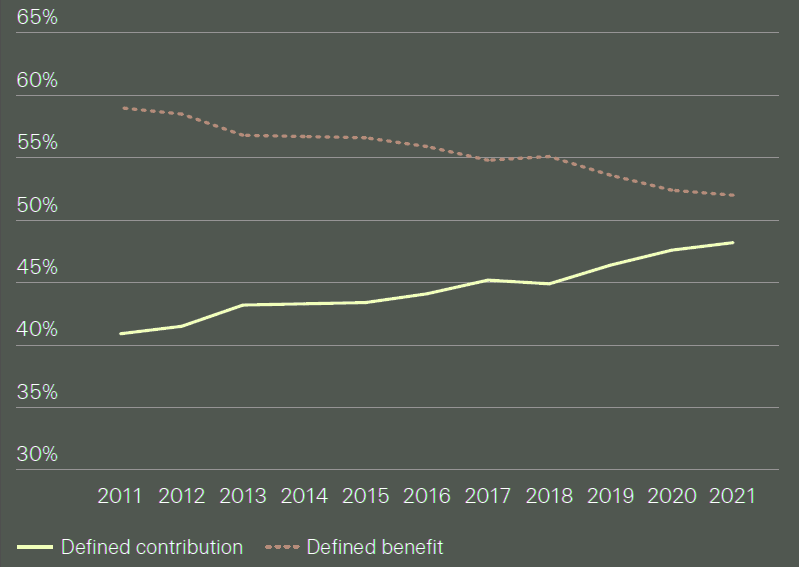

Defined benefit and contribution of US pension assets

The monetary policy tightening cycle initiated in 2022 has shifted the competitive and operational environment for life insurers from low yield and return to higher yields and returns, especially for asset-intensive businesses.

Higher yields increase demand for savings-related products and enhance the potential profitability of both savings- and protection-related products. Insurers experience rising sales and profits but must prepare for emerging risks.

Low interest rate held back life insurance premium growth

The global rate of retirement savings is alarmingly low, falling significantly short of individual needs. A WEF study evaluates funding levels for government-provided systems, public employee systems, employer-based systems, and individual pension savings, highlighting the extent of this challenge.

Swiss Re estimates the retirement savings gap for six advanced economies, China, and India at $106 trillion in 2022, averaging 270% of GDP.

Life insurance offers various savings products to help accumulate or decumulate funds over time, often including a life protection component, known as “composite” or “hybrid” savings products.

Retirement savings gap

These composites combine investment and insurance protection, allowing policyholders to invest a portion of their premiums in investment funds. The added protection component sets life insurers apart from asset management competitors.

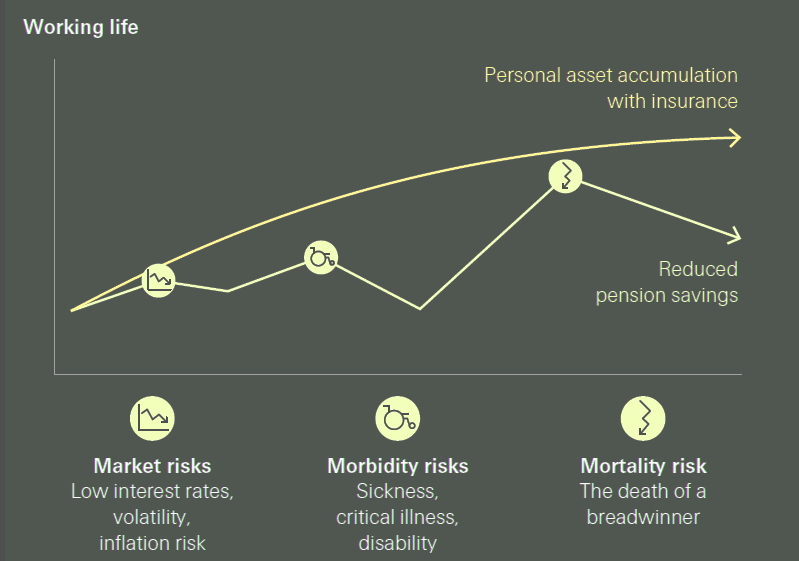

The protection element, or “rider,” can cover multiple life risks, including morbidity and mortality risks during the accumulation phase and longevity and long-term care risks during the decumulation phase.

Pension saving accumulation and decumulation risks

Long-term saving products for private individuals

The life insurance industry plays an important role providing products for retirement preparedness in the private saving market. With USD 3.1 trillion of global premiums in 2023, traditional life (life insurance and savings business, disability, critical illness, and long-term care) is the core of the L&H sector.

About USD 2.4 trillion (77% of premiums) account for savings business, i.e. the accumulation of retirement assets.

The other USD 0.7 trillion (23%) for mortality, morbidity and longevity risks provide income protection during the accumulation (savings) phase. About 80% of global savings premiums originate from advanced markets but the share of emerging markets is rising steadily.

We estimate that life insurers now manage some USD 6 trillion of assets under management, or about 12% of the USD 51.3 trillion private (funded) pension assets in 28 OECD countries as of 2022.

How to close the retirement savings gap

Since 2022, rising interest rates in most markets have reshaped the business environment for life insurers. Higher rates have lifted investment yields and improved crediting rates on saving products while gradually improving the pricing of protection business.

This notably sparked renewed interest in annuity-type products as consumers seek to capitalise immediately on more attractive returns.

Yet, higher interest rates will not be enough to close the retirement savings gap. To mobilise the large needed private retirement savings in the long-term requires life insurers to be agile in anticipating evolving consumer needs.

We see an opportunity for life insurers to develop new convertible life products that proactively anticipate consumers’ needs and market them through digital channels.

Low financial literacy can also hamper uptake of life insurance policies, and insurers could take steps to increase consumer knowledge of the life value proposition, while helping promote deeper capital markets in emerging economies.

Finally, saving and investing preferences evolve, particularly among younger cohorts in Europe and Asia and on the topic of sustainability. Life insurers may benefit from aligning their offerings with these new generational aspirations.

……………………

AUTHORS: Germante Boncaldo – Head of Reinsurance Business Development at Swiss Re, James Finucane – Senior Economist, Swiss Re Institute, Thomas Holzheu – Chief Economist Americas, Swiss Re Institute