Overview

S&P Global Ratings reports that U.S. insurers have sufficient capital and liquidity to absorb current market volatility, including disruptions linked to recent tariff measures, without any immediate effect on credit ratings or sector outlooks.

The announcement of wide-ranging tariffs by the US administration, followed by a temporary pause on April 9, triggered notable reactions across global financial markets.

According to S&P’s report Robust Capital Supports North American Insurers Amid Market Volatility, declines in investment values could affect insurers’ financial strength, but their risk management practices and defined risk thresholds support short-term stability (see How US tariffs could affect the insurance sector? J.P. Morgan forcast).

5 Key Takeaways

- A conservative asset mix and mostly investment-grade bond holdings allow insurers to withstand equity volatility and interest rate movements without significant capital strain.

- Despite tariff-related uncertainty and financial market shifts, U.S. insurers have the capital and liquidity needed to manage short-term instability.

- Major P&C insurers with exposure to California wildfires are reporting elevated combined ratios, with several exceeding 100%.

- New tariffs on auto imports and parts may lead to double-digit premium increases, affecting underwriting and claims costs across the sector.

- P&C insurers face equity market and catastrophe-related risks; life and health insurers deal with interest rate effects and operational stress in key programs.

The report notes that the property and casualty insurance sector in North America has maintained solid capital levels and stable underwriting results, which help mitigate market pressure.

As of year-end 2024, P&C insurers held an average portfolio allocation of 55% in bonds and loans, and 24% in equities. Their average investment yield from 2020 to 2024 stood at 3%, providing consistent capital support.

Most bond holdings remain investment-grade, limiting the risk of credit losses, though equity holdings—averaging 26.4% over the past five years—introduce greater sensitivity to market fluctuations.

Re/insurers Equipped to Absorb NatCat Losses

S&P states that reinsurance providers are also prepared to manage the first-quarter increase in natural catastrophe losses alongside financial market instability, primarily due to strong capital positions.

For life insurers, direct exposure to equity markets remains limited, though analysts are monitoring indirect effects of market shifts.

A sharp drop in interest rates could reduce sales and profitability, slow acquisition activity, and negatively affect bond portfolios through potential impairments and credit downgrades.

However, S&P indicates that interest rate movements have had minimal impact so far, and there is no current evidence of material adverse effects on capital.

In the health insurance segment, equity market downturns may weaken capital positions, particularly for mutual and not-for-profit insurers, which typically allocate up to 30% of investments to equities.

Publicly traded, for-profit insurers tend to carry limited or no equity exposure, offering greater protection from equity-driven capital strain.

The sector already faces pressure from operational challenges, with about one-third of ratings carrying a negative outlook.

These challenges include financial stress in commercial lines, Medicare Advantage, and Medicaid programs.

Tariff-related economic pressure

Tariff-related economic pressure could lower commercial enrolment but may raise enrolment in countercyclical programs such as ACA and Medicaid.

S&P also points to the upcoming 2026 Medicare Advantage rate increase of 5.06% as a supportive factor for earnings and enrolment expansion.

The effect will depend on insurers’ ability to price accurately in line with ongoing medical cost inflation.

While market volatility presents clear risks, North American insurers remain well positioned due to strong capital reserves, cautious investment strategies, and effective risk controls.

Ongoing assessment will focus on credit market behavior, interest rate trends, and broader economic conditions.

Commercial insurers face different risks and often operate with broader geographic exposure, making them less sensitive to tariff-driven price increases. Reinsurers also encounter some pressure from rising material costs but remain less directly affected than personal lines carriers.

Auto insurance premiums in the U.S. could rise 14% by the end of 2025 due to new tariffs on imported vehicles and parts.

The expected increase in claims costs—estimated between $26bn and $52bn—reflects rising repair prices, new car costs, and pressure on used car markets. Insurers are already responding with higher rates and cost controls, but face limits to further efficiency gains.

Additional tariffs on goods from China, Canada, and Mexico may push premium increases to 19%. As market leaders assess the impact, policyholders should expect continued volatility and limited room for rate relief in the near term.

U.S. auto insurance premiums could increase 14% on average by year-end due to new tariffs on imported vehicles and parts, according to US Auto Insurance Rates by States.

Insurers estimate the annual personal auto claims cost may grow by $26bn to $52bn. The 25% tariffs on imported passenger vehicles and light trucks take effect on April 3, and on key parts by May 3.

Economists expect these import levies to raise new car prices significantly, due to low profit margins and interconnected global supply chains.

Life insurers appear more insulated from immediate effects, though extended trade tensions may still present challenges.

Tariffs, wildfires to top US P&C insurers’ earnings season agenda

The fallout from the Southern California wildfires and the twists and turns of the tariff landscape will take center stage when US property and casualty insurers release first-quarter financial results.

Insurers are expected to detail the losses caused by and the response to wildfires that broke out on Jan. 7 and swept through the Los Angeles suburbs, according to S&P`s report.

The blazes, which were all 100% contained by Jan. 31, burned more than 57,000 acres, destroyed more than 16,000 structures, caused at least 30 deaths and generated estimated economic losses of between $250 bn and $275 bn.

Reciprocal tariffs announced by President Donald Trump earlier this month will also garner much attention.

While Trump paused many of those tariffs for 90 days, personal auto carriers would face the same issues that plagued them during and after the COVID pandemic — disrupted supply chains, claims cost inflation from labor shortages and elevated new and used auto prices — if they eventually do go into effect.

While the pause was a welcome relief, CFRA Research analyst Cathy Seifert said Trump “is still hell-bent on tariffs.”

The uncertainty is if these tariffs stay long term, they’ll be driving up [the cost of] everything, both cars and insurance. If new car prices go up, people will look for used, which will drive up the price and inventory will go down.

Insurtech Advisors analyst Kaenan Hertz

If tariffs end up being inflationary, the Federal Reserve could be forced to keep interest rates elevated and borrowing costs would move higher.

Wildfires Drive Up Combined Ratios for Major US Insurers

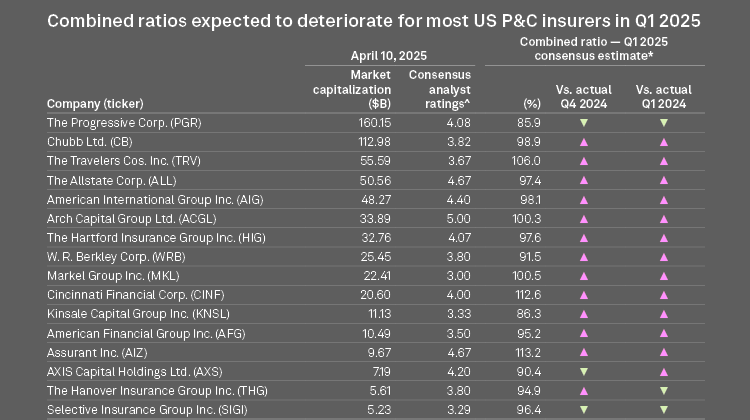

An analysis by S&P Global Market Intelligence shows that 13 of the 16 largest publicly traded US property and casualty and multiline insurers are expected to report higher combined ratios both sequentially and year over year.

The projections suggest widespread deterioration in underwriting performance across the sector. Five insurers are projected to report combined ratios above 100%, indicating underwriting losses.

These firms—each with significant exposure to the Los Angeles wildfires—include Assurant Inc. (113.2%), Cincinnati Financial Corp. (112.6%), The Travelers Companies Inc. (106.0%), Markel Group Inc. (100.5%), and Arch Capital Group Ltd. (100.3%).

State Farm General Insurance Co. recorded the highest estimated wildfire-related losses in January at $7.6 bn. Travelers followed with an estimated $1.7 bn in losses. Despite this, analyst Paul Newsome of Piper Sandler stated that the scale of the loss is unlikely to materially impact Travelers’ capital position.

The Allstate Corp. reported estimated wildfire losses of $1.07 bn, while Cincinnati Financial and Assurant reported $487.5 mn and $150 mn, respectively. Markel’s estimated losses stood at $110 mn.

Conversely, The Progressive Corp. is expected to report the lowest combined ratio at 85.9%, followed by Kinsale Capital Group Inc. (86.3%) and AXIS Capital Holdings Ltd. (90.4%). Progressive and Selective Insurance Group Inc. are the only companies projected to post improvement in combined ratios both sequentially and compared to the previous year.

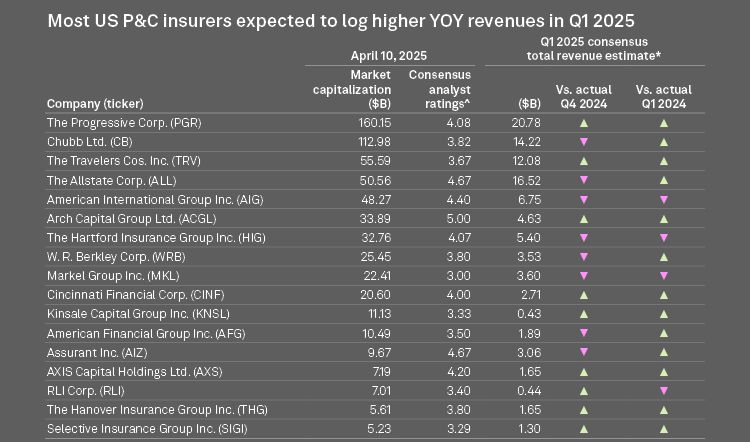

A majority of the companies in this analysis are projected to show revenue increases on both sequential and year-over-year bases.

Progressive had the highest estimate for the first quarter at $20.78 bn and is one of four companies expected to have revenues of more than $10 bn. Allstate was second with a $16.52 bn estimate, followed by Chubb Ltd. at $14.22 bn and Travelers at $12.08 bn.

The Hartford Insurance Group Inc., American International Group Inc. and Markel are the only companies expected to show declines in revenue from both last quarter and a year ago.

FAQ

S&P Global Ratings states that U.S. insurers have adequate capital and liquidity to manage current volatility without affecting their credit ratings or outlooks. Their risk management practices and stable underwriting margins support short-term resilience.

New tariffs, especially on imported vehicles and parts, are expected to increase auto insurance premiums by 14% by the end of 2025. Additional tariffs on goods from China, Canada, and Mexico could raise this to 19%, increasing claims costs by an estimated $26–52 bn.

Wildfires in Southern California have significantly impacted underwriting results, with five major insurers projected to post combined ratios above 100%, indicating underwriting losses. State Farm faced the highest losses at $7.6 bn, followed by Travelers at $1.7 bn.

A combined ratio measures underwriting profitability. Ratios above 100% indicate a company is paying out more in claims and expenses than it earns in premiums. Thirteen of the sixteen largest U.S. insurers are expected to report deteriorating combined ratios.

No. Property and casualty (P&C) insurers face volatility due to equity market exposure and natural catastrophes. Life insurers are less exposed to equity fluctuations but are sensitive to interest rate movements. Mutual and not-for-profit health insurers are more exposed to equity market risk than their for-profit counterparts.

As of year-end 2024, P&C insurers had 55% of assets in bonds and loans and 24% in equities. Their investment portfolios are primarily composed of investment-grade bonds, supporting capital stability despite market swings.

The 5.06% rate increase for Medicare Advantage in 2026 could support enrolment growth and improve earnings. However, outcomes depend on insurers’ ability to align pricing with elevated medical cost inflation.

…………………..

AUTHORS: Tom Jacobs – Insurance Reporter II for S&P Global Market Intelligence, Noor Ul Ain Adeel – Research Associate, FI Research, Data analytics for S&P Global Market Intelligence