Overview

The improving mid-year 2024 results for U.S. personal auto insurers are expected to persist through the rest of 2024 and into 2025. Significant price hikes and easing claims severity have strengthened the segment’s profitability, according to Fitch Ratings report.

The return to underwriting profitability may cause price increases to level off. As underwriting improves, competition and pressure from policyholders and regulators could limit further price hikes.

Personal auto insurance underwriting profitability appears to finally be headed in a positive direction after recent years of record underwriting losses. But while these gains show improvement, it will likely take time for them to be reflected in flattening premium rate

Outlook for the U.S. personal lines insurance

Insurers struggling to turn around their auto results, particularly some large mutual carriers, may find it challenging to implement necessary price adjustments while retaining customers in a more competitive market.

This progress underpins Fitch’s current “Improving” outlook for the U.S. personal lines insurance sector. Sustained auto profits will help several companies restore capital adequacy after profit declines in 2022 and 2024.

GAAP filings from nine publicly traded insurers show that the group’s combined ratio (CR) for the personal auto segment dropped to 89% in the first half of 2024, down from 100% in 1H2023 and 101% in 1H2022.

Personal Auto Underlying Growth and Replacement Costs

| Personal Auto (Change YoY%) | 2023 | 2024 | 2025 | 2026 |

| Underlying Growth | 10.2% | 4.0% | 4.7% | 5.5% |

| Auto and Light Truck Sales | 12.9% | 4.0% | 5.0% | 6.0% |

| Motor Vehicle Personal Expenditures | 4.8% | 4.0% | 4.2% | 4.5% |

| Replacement Costs | -0.2% | -0.5% | 1.8% | 2.7% |

| New Vehicles | 3.7% | 0.4% | 2.0% | 3.0% |

| Used Cars and Trucks | -7.1% | -1.4% | 1.5% | 2.5% |

| Motor Vehicle Parts and Equipment | 2.9% | -0.5% | 2.0% | 2.5% |

In 2024, new vehicle sales experienced their best year since 2019 – a development that benefited auto insurers’ DPW, as more cars sold means more cars insured.

U.S. personal auto insurers posted CR improvements

Progressive Corporation (PGR) and GEICO, the second and third largest auto insurers, reported particularly strong results, with CRs of 87% and 82%, respectively. Only Hartford Financial Services Corp. and Cincinnati Financial Corporation had segment CRs above 100% for the first half of 2024.

Nearly all insurers in this group posted CR improvements of 10 points or more year-over-year.

Loss severity trends in personal auto insurance have moderated after sharp increases that began in the second half of 2021 due to pandemic-related disruptions. Inflation has also driven up costs for auto parts, repairs, medical expenses, and used vehicles.

US Insurer Personal Auto Segment Results Improved

Aggregate GAAP written premiums rose 14.4%, combined ratio fell 11.6 points

GAAP Written Premium

| Insurer | Premiums, $mn | YoY Change |

|---|---|---|

| Progressive | 29,043 | 22.5% |

| GEICO | 21,254 | 8.9% |

| Allstate | 18,641 | 12.2% |

| Travelers | 4,079 | 10.8% |

| Kemper | 1,412 | -7.7% |

| Hartford | 1,217 | 13.5% |

| Hanover | 700 | 1.3% |

| Cincinnati Financial | 499 | 33.4% |

| Horace Mann | 239 | 15.0% |

| Group Aggregate | 77,084 | 14.4% |

Hanover and Cincinnati Financial do not break out expense ratio by segment; combined ratio based on personal lines expense ratio.

GAAP Combined Ratio

| Insurer | 2023 | 2024 |

| Progressive | 99.1 | 86.6 |

| GEICO | 93.7 | 82.1 |

| Allstate | 106.4 | 96.0 |

| Travelers | 106.6 | 96.5 |

| Kemper | 110.5 | 92.9 |

| Hartford | 113.3 | 104.7 |

| Hanover | 107.9 | 97.0 |

| Cincinnati Financial | 108.1 | 105.6 |

| Horace Mann | 112.8 | 99.0 |

| Group Aggregate | 100.4 | 88.8 |

U.S. auto insurers declines of claims

Major auto insurers saw notable declines in claims severity by mid-2024. PGR’s personal auto incurred severity dropped to 1% in 1H2024, down from 11% a year earlier.

GEICO’s loss severity on physical damage claims decreased to 8-10% in 1H2024, compared to 21-23% in 1H23.

Successive auto insurance premium rate increases have also contributed significantly to improved underwriting performance.

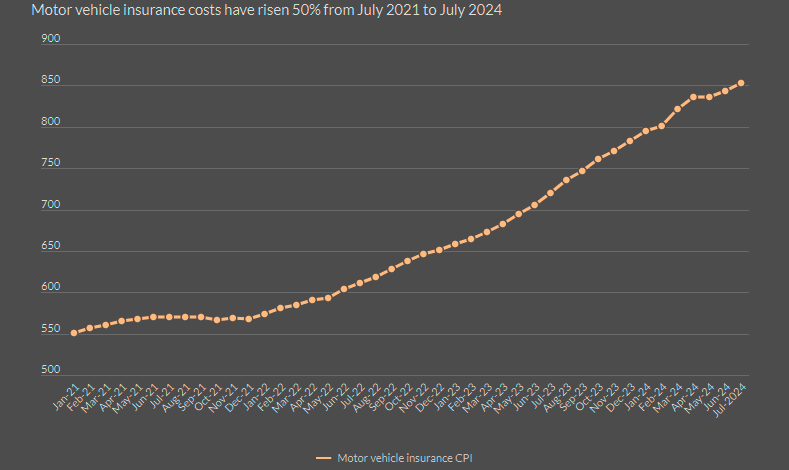

Consumer Price Index data shows motor vehicle insurance costs increased by 50% from July 2021 to July 2024.

Price growth has slowed slightly, with a 19% year-over-year rise in July 2024, compared to a 22% increase in March 2024.

These pricing actions led to a 14% year-over-year growth in net written premiums for the group, including 22% growth for PGR. The company’s early return to profitability positions it for near-term growth and a potential challenge to State Farm for the top market share in the segment in the coming years.

Motor Vehicle Insurance CPI Has Risen Meaningfully

U.S. auto and homeowners insurance premium rates lagged behind the inflation rate in 2020 and 2021, laying the groundwork for the premium increases which occurred last year and will continue into 2024, according to the Insurance Information Institute.

As material and labor costs rise, the cost to repair and replace damaged homes and vehicles increases.

If premium rates didn’t reflect these increased costs, insurers would quickly exhaust the funds they set aside— ‘policyholder surplus’—to ensure that they can afford to keep their promises to pay all claims.

But insurers do more than pay claims. They employ people (labor costs) and conduct business operations (supplies and energy costs); and, if they are to remain in business, they have to earn a reasonable profit. Each insurer’s policyholder surplus accounts for its total assets, after subtracting all of its liabilities.

FAQ

The segment’s profitability has strengthened due to significant price hikes and a reduction in claims severity, according to Fitch Ratings. This improvement is helping companies turn around their auto results.

As underwriting improves and competition increases, policyholders and regulators are exerting pressure that limits further price hikes. This could lead to a stabilization of premium rates.

Many insurers saw improvements in their combined ratios (CRs), with Progressive and GEICO leading the way. CRs dropped significantly, indicating improved underwriting performance, and written premiums saw strong growth

Insurers, especially large mutual carriers, may struggle to implement necessary price adjustments while retaining customers in an increasingly competitive market.

Claims severity trends have moderated after sharp increases in 2021. For example, Progressive’s claims severity dropped to 1% in the first half of 2024, significantly down from 11% a year earlier.

Inflation has driven up the costs of auto parts, repairs, and medical expenses. Between July 2021 and July 2024, motor vehicle insurance costs rose by 50%, though price growth slowed slightly in mid-2024.

Premium rates have risen in response to the rising costs of materials, labor, and vehicle repairs. Insurers need to reflect these costs in premiums to maintain financial stability and ensure they can cover future claims.

………………

AUTHORS: James Auden – Managing Director at Fitch Ratings, Laura Kaster, CFA – Senior Director of North and South American Financial Institutions, Fitch Ratings, Christopher Grimes – Director at Fitch Ratings,