Overview

Global Insurance Market Report shares the outcome of the Global Monitoring Exercise, the International Association of Insurance Supervisors’ risk assessment framework to monitor key risks and trends and detect the potential build-up of systemic risk in the Global Insurance Sector.

According to IAIS, the data collected from approximately 60 of the largest international insurance groups, as well as aggregate data from sector-wide monitoring (SWM) from supervisors across the globe (27 jurisdictions), covering over 90% of global written premiums.

Through the GME, the IAIS monitors global insurance market trends and developments, detects the possible build-up of systemic risk and facilitates a collective discussion on the appropriate supervisory response at the sectoral and individual insurer level

Vicky Saporta, IAIS Executive Committee Chair

IAIS’ analysis concludes that systemic risk in the insurance sector is moderate on aggregate and low relative to that of the banking sector, however insurers’ total systemic risk scores are trending upward (see TOP 50 World’s Largest Insurance Companies by capitalization).

The trend toward higher total systemic risk scores is driven by increased exposures to illiquid, difficult-to-value assets (level 3 assets), over-the-counter derivatives, short-term funding (in particular repurchase transactions) and intra-financial assets (including reinsurance). This contributes to potential vulnerabilities for the insurance sector, notably in the face of rapidly increasing interest rates.

Risk Assessment for Life and Non-life insurers

Supervisors were requested to provide responses on impacts that had already materialised and those expected over the next one to three years.

For life insurers, supervisors indicated that the main impact has come from the rise in interest rates.

This has been positive for capital resources and led to higher profitability on life products, with potential to reduce the risk of reserve deficiencies. However, in many jurisdictions, higher interest rates expose insurers to a repricing of fixed-income securities and a rebalancing of interest rate hedges.

Supervisors expressed concerns over increased hedging costs due to higher volatility in financial markets. Insurers that hedge against a low interest rate environment may also be exposed to large margin calls in the event of sharp upward movements in interest rates.

Furthermore, some supervisors noted that higher discount rates and lower technical provisions are resulting in higher solvency ratios, with the latter dependent on the applicable accounting and regulatory framework.

In addition, for jurisdictions with market value-based solvency regimes, rising interest rates translate into bond value reductions from mark-to-market losses, which could trigger company de-leveraging actions if leverage ratios approach rating agency thresholds.

Non-life insurers have been affected by inflationary pressures through increases in expenses, higher claims severity and a revaluation of reserves, which can create challenges for insurers.

This could result in compressed margins as the ability to pass these extra costs onto policyholders might be limited by market structure, competition and regulation.

Higher inflation has also led to a reassessment of existing technical provisions, with more negative consequences for longer-tail business lines such as certain lines of health, general liability and workers compensation.

Interest rate changes are having a more modest impact on non-life insurers, as non-life insurers’ liabilities are less dependent on interest rates, plus an average shorter duration of liabilities and the low duration mismatch between assets and liabilities in some jurisdictions.

Life insurers expect premiums to rise in 2022 and 2023 according to responses collected in mid-2022 as part of the 2022 IIM.

Global life premiums are expected to decrease marginally in real terms in 2022 and increase by just below 2% in 2023. The results from the IAIS supervisor feedback loop conducted in July 2022 noted that a limited effect on earnings had materialised but some supervisors expressed concerns about future profitability, according to Global Insurance Market Index.

In the event that portfolios are gradually re-invested at higher returns, it is still likely that there will be continued pressure on costs, particularly for unit-linked products where cost increases might be difficult to pass on to policyholders.

Some supervisors pointed to the risk of increased lapses as other financial products (such as savings products) reflect changes in interest rates more quickly; however, this could be mitigated by tax and surrender penalties for early withdrawals in certain jurisdictions.

Non-life insurers also indicated expectations of premium increases in 2022 and 2023 as part of their IIM submissions in mid-2022; however, more recent data indicates that premium growth is under pressure as the economic slowdown and a multi-year inflation high has reduced premium income in real terms.

For example, Swiss Re expects 2022 inflation-adjusted non-life premia to grow by only 0.8% and 2.2% in 2022 and 2023, respectively. Additionally, supervisors noted that there have been some increases in loss costs and this trend is expected to continue if inflation remains high.

In terms of insurers’ assets, current inflation and interest rate conditions have negatively affected insurers’ asset portfolios. In jurisdictions where bonds are held at fair value, supervisors noted reduced bond values with the largest impact on longer duration bonds.

The sharp decline in equity prices has had a relatively limited impact on insurance capital, due to insurers’ relatively small equity allocations.

Qualitative responses to the IIM exercise in April 2022 indicate a reallocation of assets from public fixed-income portfolios and traditional listed equities towards alternative assets (such as infrastructure, private debt, private equity, hedge funds and real estate), with some responses citing an illiquidity premium and inflation protection as motivation.

Global insurance market developments

This section outlines the key global insurance market developments, covering assets and liabilities, solvency, profitability and liquidity.

Insurers and supervisors noted that potential positive effects on the insurance sector in the period ahead include a continued recovery from the Covid-19 pandemic, gradually rising interest rates and recovering financial markets.

However, several macroprudential factors create uncertainty around the insurance sector’s solvency, profitability and liquidity position for 2023.

Assets and liabilities

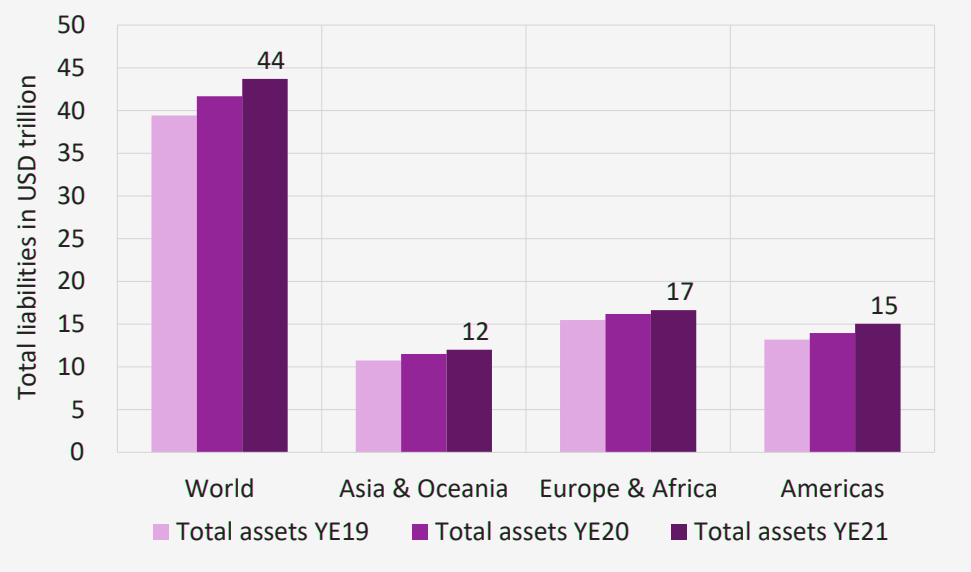

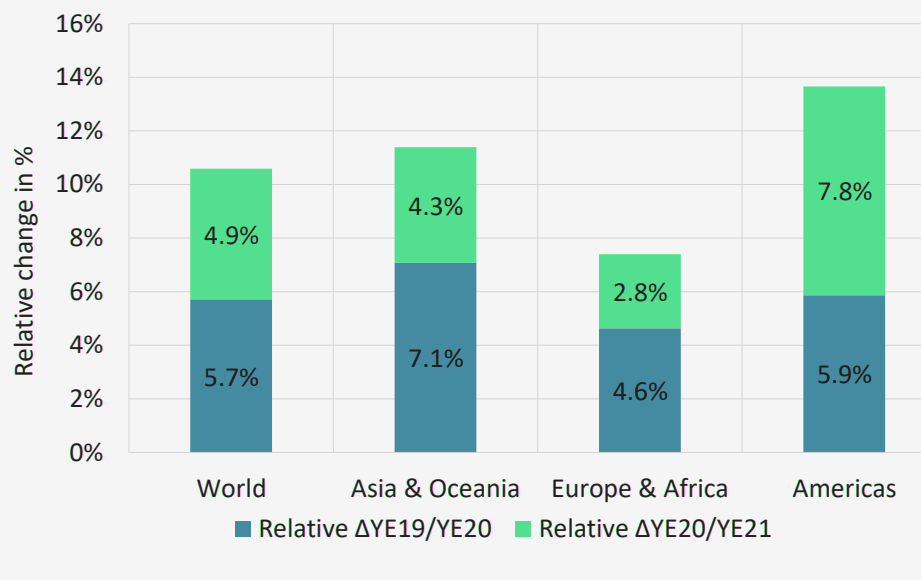

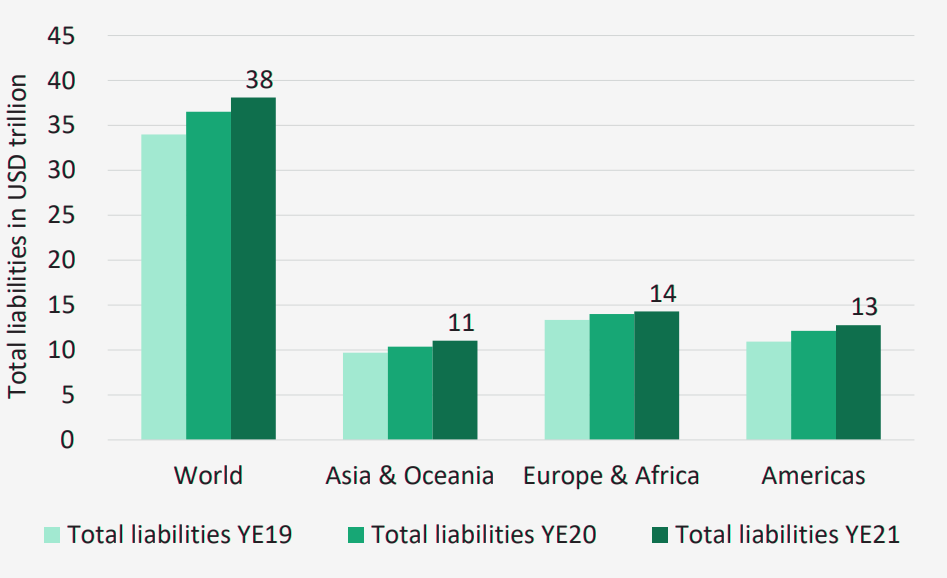

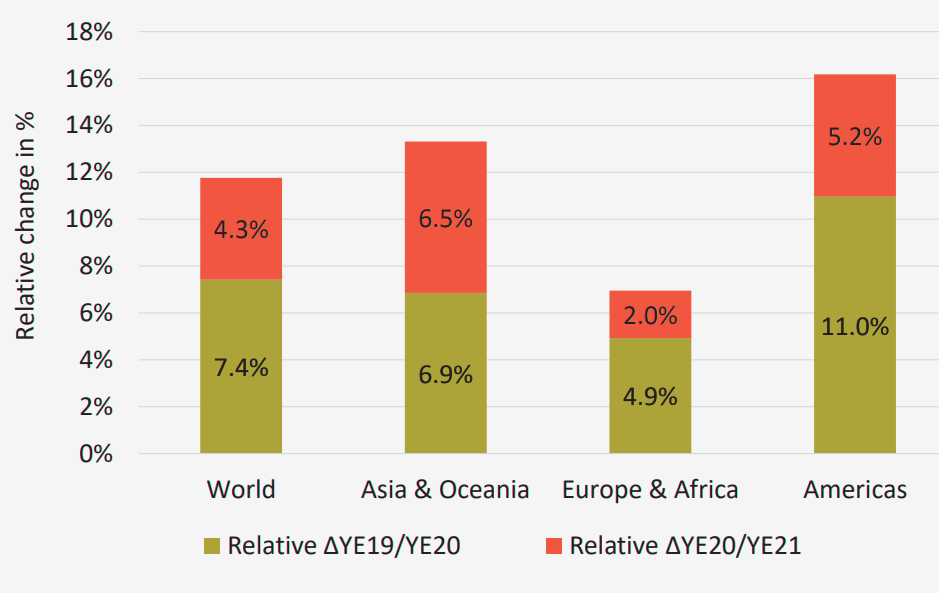

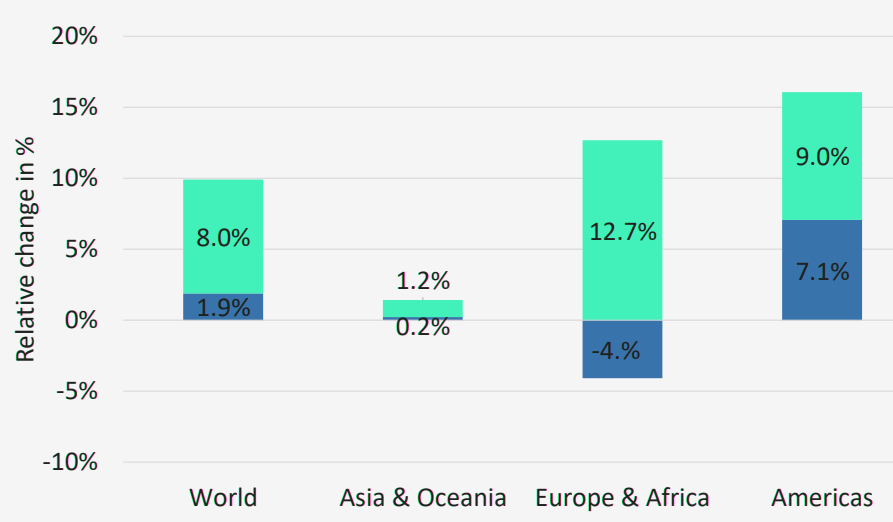

Total assets as reported rose by 4.9% to $44 trillion, whereas total liabilities have increased by 4.3% to $38 trillion.4 In the Asia and Oceania region, liabilities (+6.5%) increased more than assets (+4.3%), explaining the decrease in the excess of assets over liabilities. The overall credit quality of assets is high, with a limited share of below-investment-grade assets (3% at the global level).

Total assets

Total assets changes in %

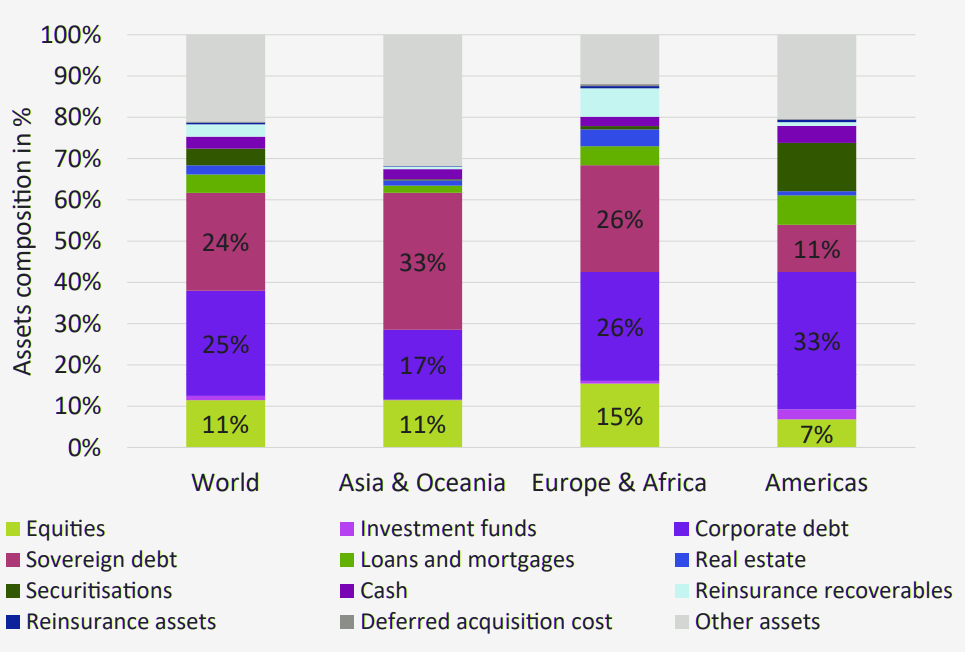

The vast majority of assets is still composed of corporate debt, sovereign debt and equities. A combination of asset reallocations and improvements in the granularity of SWM reporting led to a decrease in the “other assets” category.

Total liabilities

Total liabilities changes in %

The overall credit quality of assets held by insurers remained high. On aggregate, 80% of insurer assets were of either investment grade or above. The share of below-investment-grade assets reported in the SWM remained limited at 3% at the global level.

Assets compositon in %

Assets compositon changes in %

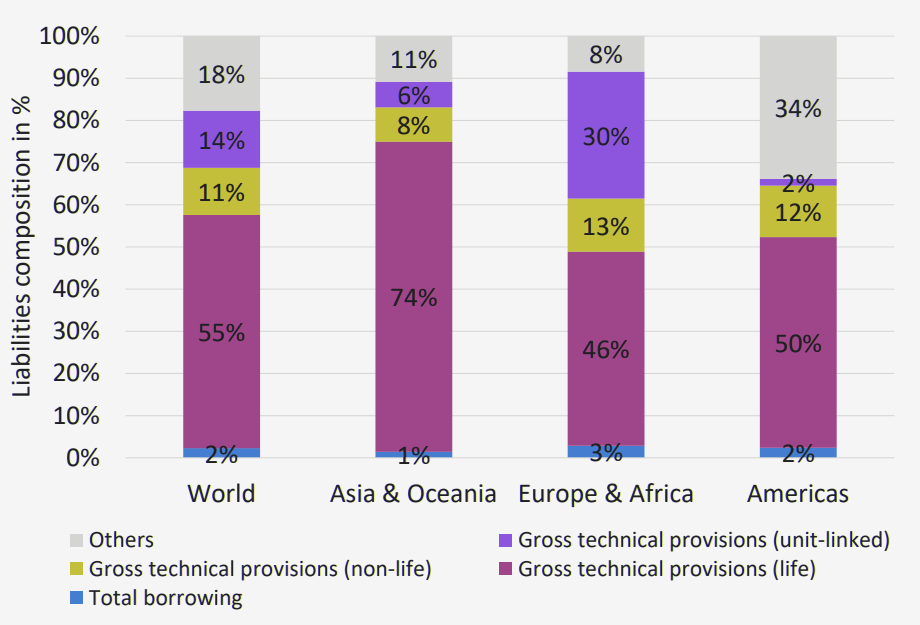

Turning to the composition of liabilities, on aggregate, liabilities were mostly composed of gross technical provisions for life insurance (55%), gross technical provisions for unit-linked insurance (14%) and gross technical provisions for non-life insurance (11%). The overall amount of borrowing remained limited at 2%, showing no change compared to last year.

Liabilities composition in %

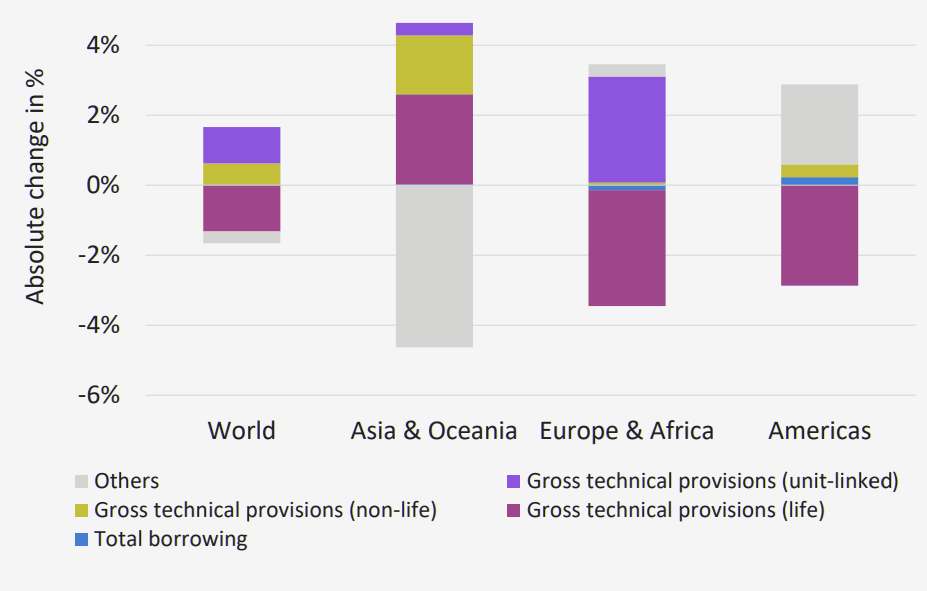

Liabilities composition changes in %

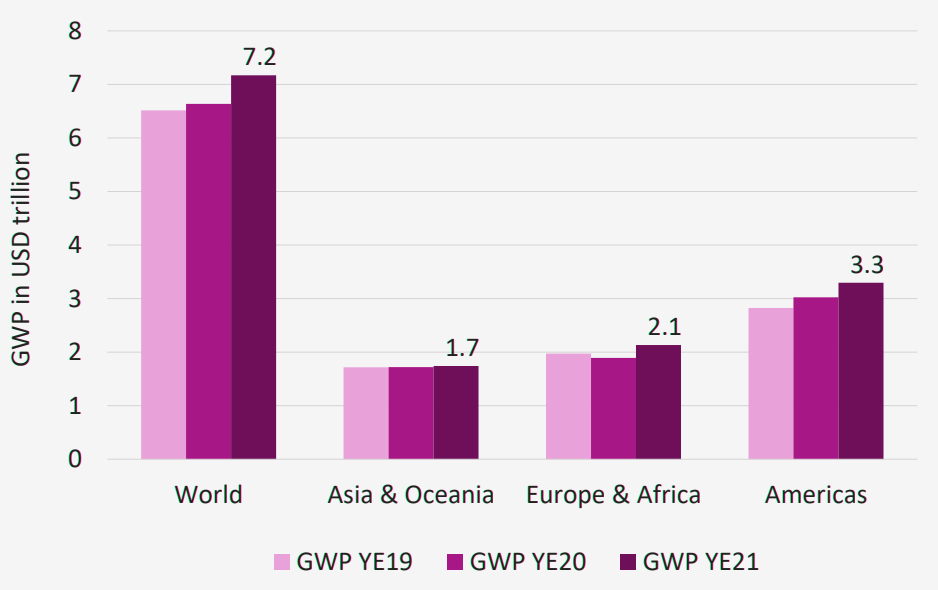

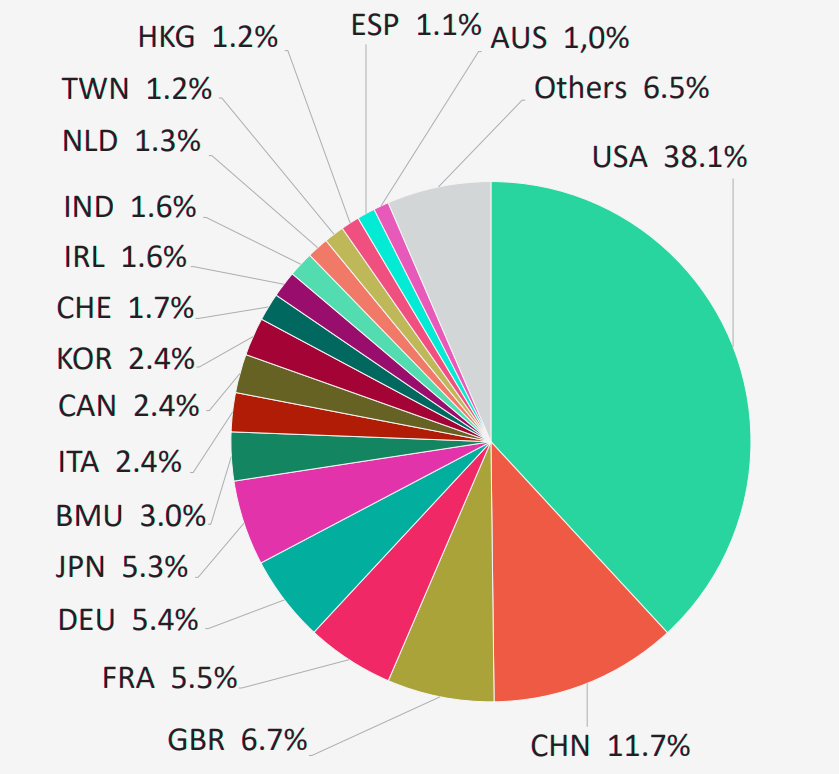

Gross written premiums increased by 8%. In terms of geographic distribution of gross written premiums, most premiums at year-end 2022 were underwritten in the United States (US) (38.1%), followed by China (11.7%), the United Kingdom (UK) (6.7%), France (5.5%), Germany (5.4%) and Japan (5.3%).

Gross written premiums

Gross written premiums changes in %

Share of global GWP

Solvency

In all regions solvency ratios improved. In many jurisdictions, a slightly higher aggregate solvency level can be observed. No jurisdiction in the SWM reported any major concerns with their local aggregate solvency requirements. Overall, the increase in interest rates and the strong performance of financial markets contributed to an improvement in insurers’ solvency.

Most supervisors increased solvency reporting requirements during the Covid-19 crisis to cover additional details, a higher reporting frequency or a combination of both. This heightened supervisory attention to solvency continued in many jurisdictions.

In some jurisdictions there was a change to the solvency regime in recent years, or else such a change is planned for the near future. Depending on the jurisdiction, transitional measures were also put in place. In addition, the introduction of International Financial Reporting Standards (IFRS) 9 and IFRS 17 is expected to influence the solvency calculation in several jurisdictions.

Measures taken by insurers were mainly guided by individual situations rather than by global market developments. In terms of capital management, different types of measures were taken, with several insurers proceeding with share buybacks or redemptions of subordinated debt. In contrast, some insurers continued to issue subordinated debt to strengthen solvency positions or to optimise their capital structures.

Several insurers continued to buy back shares and/or redeem subordinated debt. Others issued capital and/or subordinated debt to strengthen capital and liquidity positions.

Similarly, in terms of asset allocation, different paths were taken by insurers depending on their individual situation. Some increased the risk profile of their investment portfolios while others sold equity and invested in long-term bonds to limit the share of market risks in their capital requirement. Risk mitigation techniques such as reinsurance and dynamic hedging strategies were also used to manage capital positions.

Profitability

For life insurance, profitability increased in some jurisdictions due to increases in sales and investment income. Other jurisdictions noted profitability was negatively impacted by increased mortality rates due to Covid-19 or (unrealised) investment losses driven by rising interest rates.

For non-life business, rising claims ratios and decreasing profit margins were observed across several jurisdictions, often attributed to increasing inflation and natural catastrophes.

On the other hand, improved business activity and higher pricing led to increasing revenues and, in some cases, greater profitability.

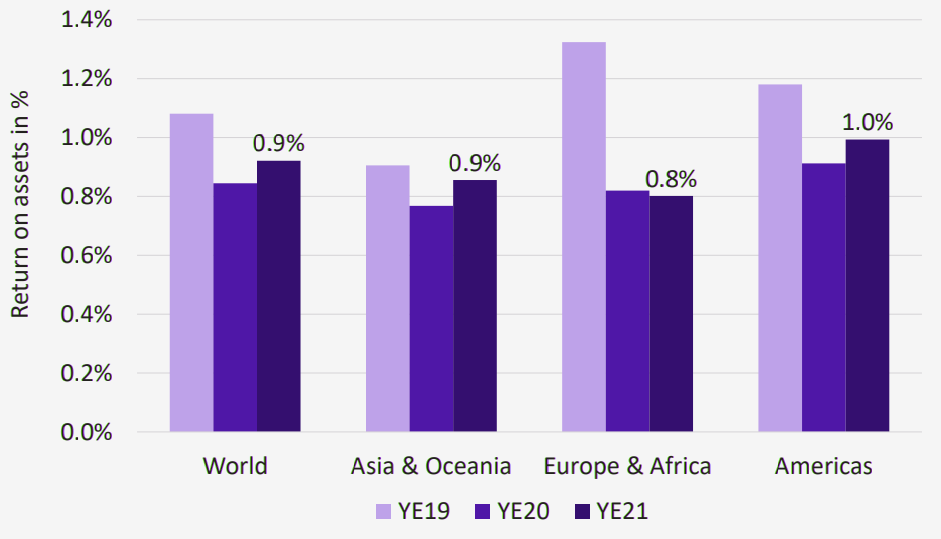

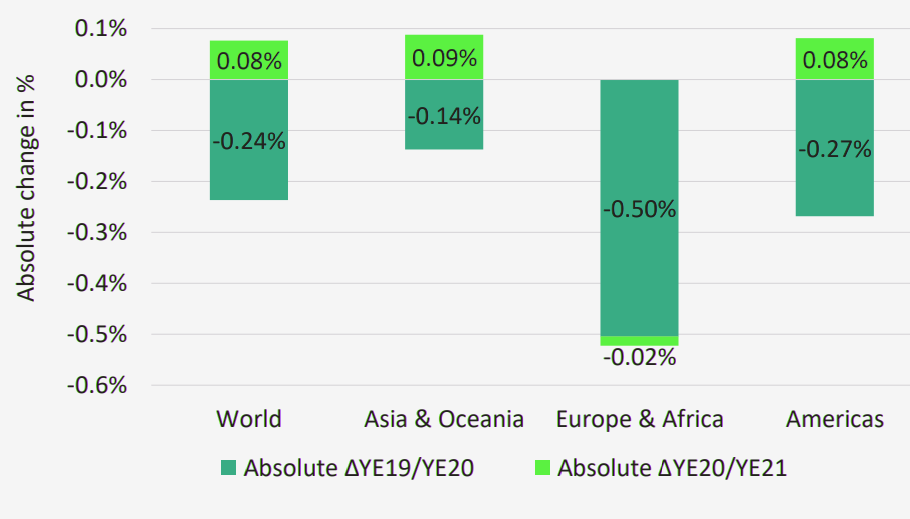

Return on assets

Return on assets changes in %

Globally, supervisors have increased their monitoring pertaining to the impact of inflation and higher interest rates, as well as potential economic recessionary pressures on insurers’ solvency and profitability.

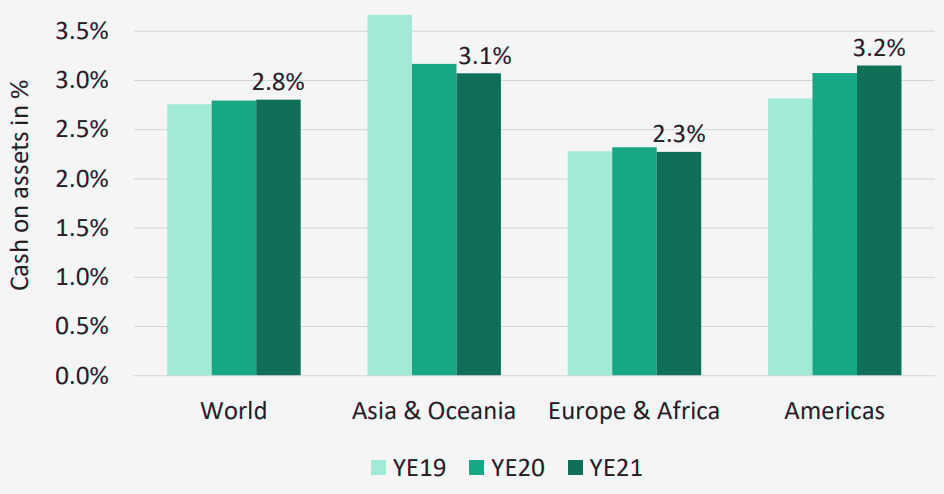

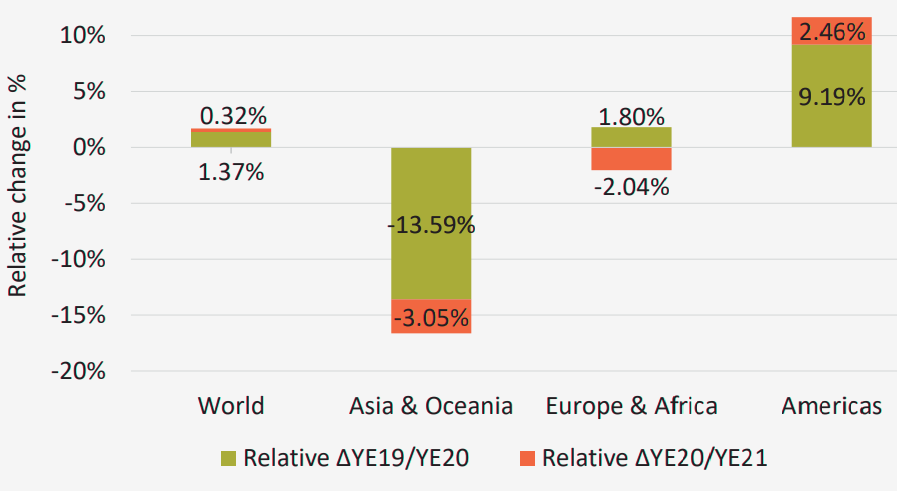

Liquidity

Insurers’ reported liquidity positions remained stable at year-end 2022 compared to year-end 2021. In some cases, a slight decrease in liquid assets was noted in the search for yield, which led to increased investment allocations to less liquid assets. Other insurers reported a strong increase in their liquidity positions, for example due to substantial increases in free cashflows.

Overall cash positions remained stable. Some insurers reported a decrease in cash buffers that were built up in 2021 by increasing investments in financial markets, in the context of the 2022 financial markets recovery.

Cash on assets

Cash on assets changes in %

Several macroprudential factors create uncertainty around the liquidity situation of the insurance sector for 2022 and 2023.

Geopolitical conflicts, particularly the war in Ukraine, create major uncertainty.

Rising interest rates in response to higher inflation are expected to impact the liquidity of certain insurers, for instance through increased derivative margin calls in those cases where hedges were put in place to mitigate the impact of decreasing rather than increasing interest rates, warranting increased attention.

Some insurers anticipate further decreases in their liquidity positions as a result of a shift in asset allocation from cash to financial market instruments in order to increase financial revenue.

Macroprudential themes

The IAIS identified three macroprudential themes based on supervisory priorities identified by the annual SWM:

- (1) lower macroeconomic outlook, high inflation and rising interest rates,

- (2) structural shifts in the life insurance sector, including the involvement of PE

- (3) climate-related risks

The highlights of the first two macroprudential themes are included in this section and are structured as follows:

- (1) theme description

- (2) risk assessment

- (3) supervisory measures

- (4) next steps

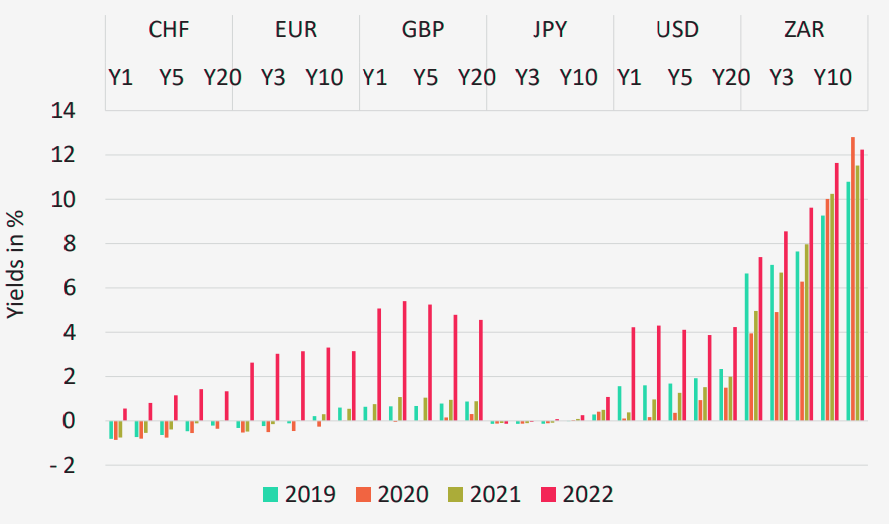

The past year has seen major changes in the global economy, with rapid rises in inflation and interest rates and sharply higher bond yields.

Theme 3 on climate-related risks is outlined in the next section and includes the follow-up analysis of the 2021 GIMAR special topic edition on climate change.

Lower macroeconomic outlook, high inflation and rising interest rates

2022 year has seen major changes in the global economy, with rapid rises in inflation and interest rates and sharply higher bond yields.

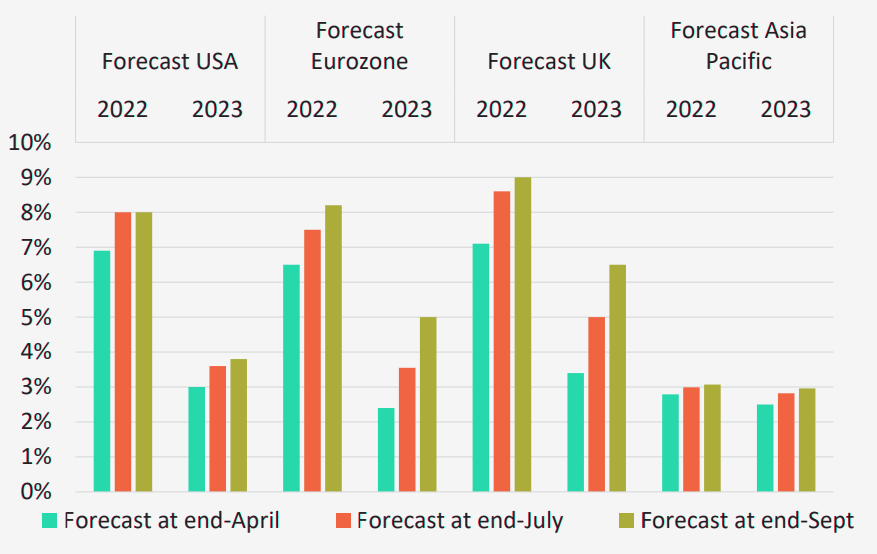

The International Monetary Fund (IMF) has revised its global growth forecast downwards for 2023 and cautioned that macro-financial conditions could deteriorate significantly.

Continued supply-related shocks to food and energy prices from the war in Ukraine could result in persistent increases in headline inflation and could pass through to core inflation, triggering further tightening in monetary policy.

This contrasts with the situation just one and a half years ago, when economies were contending with low inflation, lower-for-longer interest rates and ultra-low bond yields, which created risks of a different nature.

Recent developments are a stark reminder of how quicky financial conditions can change, presenting new challenges for financial institutions.

Changes in inflation forecast

Changes in sovereign bond yields (in %)

Although macro-financial conditions have worsened since the IIM data submission8 in May 2022 and the supervisory feedback loop in August 2022, the responses to the surveys provide a comprehensive overview of the initial impact on the insurance industry.

Steep increases in prices are likely to continue to strain living standards worldwide and affect business and household finances, which will negatively affect their ability to buy insurance coverage.

A study9 has indicated that the global insurance protection gap for health, mortality and natural catastrophe (NatCat) risks reached a new peak of $1.42 trillion in 2021 and could widen further in 2022 as higher interest rates and inflation tend to disproportionately affect the lowest-income households.

Potential impact on financial stability

In the current context, the IAIS is of the view that financial stability risks in the insurance sector are increasing as expectations of a global economic recession set in and there appears to be limited reprieve in inflation and interest rate conditions.

At this stage, while the risks to the insurance sector from macroeconomic conditions have increased, the financial stability risks from the insurance sector towards the rest of the financial system and the real economy are less pronounced.

Sovereign credit rating downgrades due to recent crisis episodes have resulted in credit rating downgrades for some insurers.

Sovereign credit rating downgrades due to recent crisis episodes have resulted in credit rating downgrades for some insurers.

The russian war in Ukraine has also had some impact, albeit relatively limited at this stage, on the insurance sector via increased claims in certain lines of business (eg aviation, trade credit insurance) and indirect exposures.

The War prompted many multinational corporations to voluntarily exit or sever business ties with Russia and triggered a broad set of international sanctions. Now, much of the focus has shifted from specific developments in Ukraine and Russia to economic inflation globally and a fracturing geopolitical order.

According to Marsh McLennan, businesses and governments should not lose sight of the indirect consequences of the Russia-Ukraine conflict, which may persist for a long time. This includes the continuing risk arising from the large volume of new economic, financial and trade sanctions; the global impact arising from the reduced availability of key commodities such as oil, fertilizer and grain; and potential insurance claims made as a result of the conflict.

When the war in Ukraine started in February this further fueled global inflationary and supply chain pressures, causing price shocks for a wide range of commodities, including energy, food and construction materials.

Claims under political risk and trade credit insurance policies typically take time to develop; the volume of claims associated with the conflict is nearly certain to increase, although that remains to be seen. Below is an industry-level look at how the conflict is introducing new risks to business operations and impacting insurance as a result.

The appreciation of the US dollar has likely had an impact on international insurers with exposures to the US market. However, overall, the financial stability impact of the war in Ukraine has been somewhat limited thus far (see How Russian War in Ukraine Impacts for Global Insurance Sector?).

But this scenario could change rapidly in the event of continued global unrest, heightened credit risks, continued increases in inflation or a rapid increase in interest rates, all of which would affect financial stability through liquidity, macro exposures, counterparty risk and substitutability channels.

Recently, there have been cases of higher margin calls, which can force asset sales to raise cash and have a knock-on effect on asset prices.

Higher interest rates could result in increased surrenders on certain products with guarantees, as the rise in guarantees tends to be outpaced by rising interest rates, potentially rendering guaranteed products less competitive.

A continued deterioration in macroeconomic conditions could trigger large volumes of margin calls, which in turn could have major implications for the liquidity management and funding needs of counterparties – and possibly even affect insurers’ solvency positions in a scenario where liquidity stresses would trigger forced sales of assets.

From a financial stability point of view, these risks will need to be closely monitored and analysed for potential liquidity and profitability strains. The interplay between these risks, the rest of the financial sector and the real economy will also need to be considered.

………………

AUTHOR: Victoria Saporta – Chair of the Executive Committee of the International Association of Insurance Supervisors and Executive Director, Prudential Regulation Authority (PRA) and the Bank of England