Overview

Global life insurance premiums are projected to grow at an annual rate of 3% in 2025 and 2026, more than double the average growth of the past decade. The sigma report, Growth in the Shadow of (Geo-)Politics, attributes this rise to increasing real wages, sustained high interest rates in markets like the US, ageing populations, and the expanding middle class in emerging economies. Beinsure reviewed the report and highlighted the key points.

Baby boomers are entering retirement at a time when higher interest rates are revitalizing the insurance savings sector. This aligns well with retirees’ need for stable, worry-free income, and the insurance industry is responding to this demand

Paul Murray, Swiss Re’s CEO of Life & Health Reinsurance

Supported by the elevated US interest rate environment, global life insurance premiums are expected to grow from $3.1 tn in 2024 to $4.8 tn by 2035 (see Largest Life Insurance Companies in the U.S.).

Life Insurance Savings Products

Consumers are capitalizing on higher interest rates globally. The US leads this growth, with individual annuity sales forecast to surpass $400 bn in 2024, far exceeding the $234 bn average of the past decade. U.S. life insurers are prepared for lower interest rates, with stable earnings and capital that will remain within rating thresholds, according to Fitch Ratings report.

US life insurers are expected to report improving mortality results for the second quarter and field questions related to credit risk as concerns mount over the industry’s exposure to commercial real estate.

Although portfolio yield growth for rated life insurers will slow with rate cuts, outcomes will depend on the yield curve’s shape and changes in credit spreads from their current, historically low levels. Most of the leading US life insurers experienced a year-over-year drop in total revenues.

The UK is also seeing robust demand for fixed-rate annuities, which is expected to remain strong through 2024 before tapering off in 2025 and 2026.

In China, impending reductions in guaranteed interest rates for savings products are driving significant sales, a trend expected to continue as longer-term savings options retain their appeal.

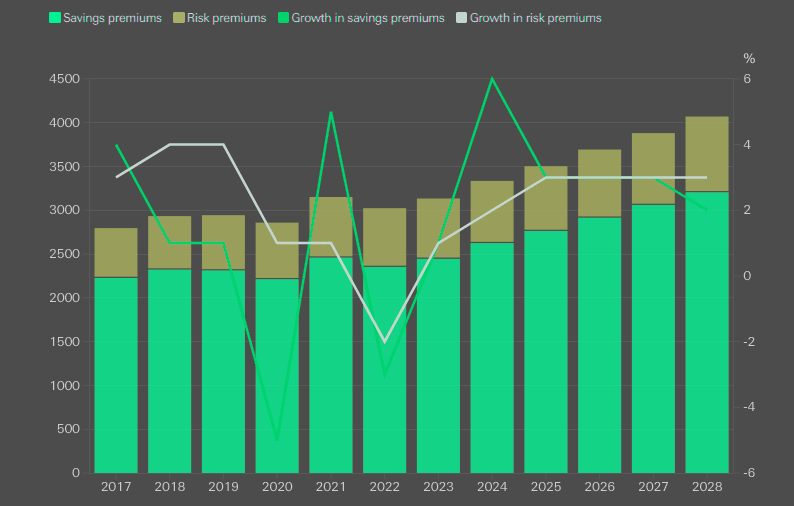

Evolution of life insurance saving and risk premiums in volume ($ bn)

Life risk protection stable, but growing below long-term trend

The life risk protection business has been growing more steadily than the savings business in recent years. Swiss Re Institute forecasts 2.7% annual premium growth in 2025 and 2026, below the long-term trend of 3.7% per year from 2014 to 2023.

In the US, individual life protection sales are expected to remain flat, while group life and health sales are slightly more resilient, supported by strong employment levels and wage gains.

According to the sigma report, the demand for protection products is generally less responsive to changes in interest rates, with re-pricing slower to materialise, but the opportunity to grow the business remains.

European markets see robust demand for disability and long-term care insurance. Looking ahead, the demand for risk protection will be driven by cyclical factors such as improving mortgage markets, and structural trends like rising costs of healthcare and nursing services, an aging population as well as attractive product bundling.

Life insurance premium growth forecast

| Region | 2024 | 2025–2026 |

| World | 5.0% | 3.0% |

| Advanced markets | 4.0% | 2.0% |

| North America | 7.1% | 1.8% |

| Western Europe | 2.5% | 1.9% |

| Asia Pacific | 1.9% | 2.5% |

| Emerging markets | 7.9% | 5.7% |

| Excl. China | 6.5% | 5.6% |

| China | 8.9% | 5.7% |

Shifts in Consumer Preferences

The report predicts a shift in advanced markets from fixed annuities to index-linked policies as central banks begin lowering interest rates. In Europe, unit-linked products are gaining traction, especially in Italy and France, with this trend likely to extend to the US and other regions by 2025.

Index-linked policies offer returns tied to specific financial indices, while unit-linked life insurance combines market-linked investments in equities, bonds, or mixed funds with life coverage.

These products are expected to meet the evolving preferences of consumers in the changing economic environment.

Total annuity insurance sales in the U.S. reached $114.6 bn in the third quarter of 2024, marking a 29% year-over-year increase. This represents the 16th straight quarter of growth, just below the record set in Q4 2023, based on data from LIMRA‘s U.S. Individual Annuity Sales Survey.

Even with the potential for further rate cuts, LIMRA expects fixed annuity products to surpass previous sales, setting new records in 2024. In the first three quarters of 2024, total annuity sales rose 23%, totaling $331.2 bn.

Non-life insurance: more profit, but less premium growth

Following the repricing of risk in response to elevated claims, Swiss Re Institute expects a decade-high 4.3% global premium growth in 2024. In the following two years, premium growth is expected to decelerate, with global non-life premiums forecast to grow 2.3% annually in real terms, below the 3.1% average of the last five years.

Further improvements in investment results from still elevated interest rates should support overall profitability of non-life insurers. Swiss Re Institute forecasts an industry return on equity (ROE) at 10% in 2025 and 2026 in the six largest non-life insurance markets, which would exceed the cost of capital.

Solid global economic growth

Global economic growth is set to continue at a solid pace. Swiss Re Institute forecasts global real GDP growth at 2.8% for 2025 and 2.7% for 2026, down from the 3.1% average growth of the pre-pandemic decade. However, there are significant regional divergences and risks are skewed to more adverse scenarios amid heightened geopolitical tensions and trade policy uncertainty.

We see higher inflation risks and chances of less interest rate cuts than previously assumed, particularly in the US given the election outcome and the continued strong economy

Jérôme Jean Haegeli, Swiss Re’s Group Chief Economist

“Still elevated interest rates could further boost primary insurance markets, especially in life insurance, but a more fragile overall economic environment and volatile geopolitical backdrop raises risks of adverse macro scenarios. Early and proactive scenario monitoring will be critical for the insurance industry”, Jérôme Jean Haegeli says.

Real GDP growth, annual avg.

| Real GDP | 2024 | 2025 | 2026 |

| Global | 2.8% | 2.8% | 2.7% |

| US | 2.8% | 2.2% | 2.1% |

| UK | 0.9% | 1.2% | 1.5% |

| Europe | 0.7% | 0.9% | 1.1% |

| Japan | -0.1% | 1.2% | 0.9% |

| China | 4.9% | 4.6% | 4.1% |

Inflation, all-items CPI, annual avg.

| Inflation, all-items CPI | 2024 | 2025 | 2026 |

| Global | 5.1% | 3.3% | 3.0% |

| US | 2.9% | 2.5% | 2.4% |

| UK | 2.5% | 2.2% | 2.3% |

| Europe | 2.3% | 2.0% | 2.1% |

| Japan | 2.6% | 2.0% | 2.0% |

| China | 0.4% | 1.1% | 1.5% |

US, Europe and China Life Insurance follow diverging paths

The 2024 US election outcome could widen global divergences in growth, inflation, and central bank policies over the next two years. US economic growth is expected to remain strong, even as momentum slows.

US real GDP is forecast to grow by 2.8% in 2024, 2.2% in 2025, and 2.1% in 2026. In contrast, Europe faces heightened risks from global trade tensions and economic uncertainty.

According to the sigma report, this outlook reflects solid consumer fundamentals, with net wealth near record highs—up about $50 tn from pre-pandemic levels—and higher savings revealed in recent GDP revisions.

European economies are expected to underperform both the US and their pre-pandemic trends.

Swiss Re projects Euro-area GDP growth at 0.7% in 2024, rising modestly to 0.9% in 2025 and 1.1% in 2026, though downside risks remain significant.

China’s economy is anticipated to continue its structural slowdown. Real GDP growth is forecast at 4.6% in 2025 and 4.1% in 2026. Recent monetary easing and fiscal stimulus measures introduced in the autumn are expected to bolster near-term business sentiment but are unlikely to address longer-term structural challenges.

FAQ

Global life insurance premiums are projected to grow at an annual rate of 3% in 2025 and 2026, more than double the average growth of the past decade.

The growth is supported by rising real wages, sustained high interest rates in key markets like the US, ageing populations, and the expanding middle class in emerging economies.

The US leads growth with individual annuity sales expected to exceed $400 bn in 2024, far surpassing the $234 bn average of the past decade. Elevated interest rates and strong consumer fundamentals support this performance.

Advanced markets are shifting from fixed annuities to index-linked and unit-linked policies. These products provide returns tied to financial indices or market-linked investments while offering life coverage.

The life risk protection sector is growing more steadily but at a slower rate than the long-term trend. Swiss Re forecasts 2.7% annual growth in 2025 and 2026, with demand driven by healthcare costs, aging populations, and bundled products.

Swiss Re projects global real GDP growth at 2.8% in 2025 and 2.7% in 2026. Regional divergences persist, with the US maintaining stronger growth, Europe facing underperformance, and China undergoing a structural slowdown.

Inflation risks and fewer interest rate cuts, particularly in the US, could influence consumer behavior and profitability in the insurance sector. Elevated rates, however, may continue to boost primary insurance markets, especially life insurance.

………….

AUTHORS: Jérôme Jean Haegeli – Swiss Re’s Group Chief Economist