Overview

Gallagher Re released a report on the impact of GLP-1 receptor agonists on medical trends and reinsurance. The report highlights how these therapies are altering medical practices and insurance structures, prompting reinsurance providers to adjust their strategies to align with emerging risk profiles. Beinsure analyzed the report and highlighted the key points.

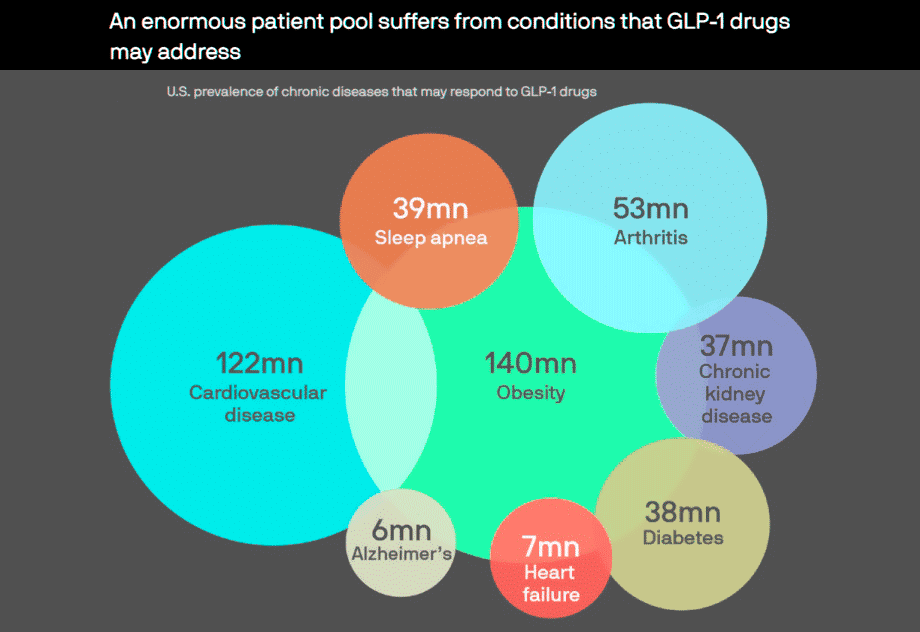

Glucagon-Like Peptide-1 (GLP-1) receptor agonists have emerged as transformative treatments for type 2 diabetes and, increasingly, for obesity management.

Following high-profile product launches such as Ozempic, Wegovy and Mounjaro, plan sponsors and reinsurers alike have seen a marked uptick in prescription spend on these medications.

In parallel, questions about the long-term medical cost implications — both positive and negative — have intensified.

Key Insights

- GLP-1 therapies now make up at least 9% of prescription spending in many employer-sponsored plans, significantly impacting overall healthcare costs.

- Despite rising usage, GLP-1 therapies have shown minimal immediate effects on specific stop-loss coverage. However, potential complications such as pancreatitis and gastrointestinal issues may still pose risks.

- Broader adoption of GLP-1 therapies, including for weight loss and pre-diabetes, is driving up per-member-per-month costs. For a group of 150 employees and 150 dependents, costs could rise by $600,000 if 20% use GLP-1 therapies.

- High discontinuation rates, reaching up to 85% within two years, challenge long-term savings projections. Many patients discontinue therapy due to side effects or lack of sustained weight loss, only to restart if weight is regained.

- New formulations, combination therapies, and expanded indications are expected to drive continued growth in GLP-1 usage. As regulatory approvals increase, insurers must update models to accommodate evolving risks and cost structures.

By synthesizing current research, survey responses from carriers, and early market data, this whitepaper aims to provide a clearer understanding of how GLP-1 therapies may influence medical trends, underwriting, and claim severity in both the near and long term (see Impact of Excess Mortality after COVID-19 on Life & Health Insurance).

Financial Implications of GLP-1 Therapies

While GLP-1 therapies show promise in improving health outcomes, rapid adoption has sparked concerns over rising prescription costs and long-term claims management challenges.

Initial findings suggest positive effects on obesity-related health issues, yet the broader financial impact on high-excess claims and aggregate stop-loss coverage remains uncertain.

Data from Brown & Brown’s 2024 Employee Benefits Market Trends Report shows rapid growth in GLP-1 usage. In many employer-sponsored plans, it now makes up at least 9% of prescription spending (see Costs for Employer Healthcare & Insurance. Top Trends).

The non-specialty prescription trend increased from 3.2% in 2023 to an estimated 10-12% in 2024, mainly due to GLP-1 receptor agonists.

Obesity will cost the US up to $9.1 trn in medical costs over the next decade, House GOP warns

Congressman David Schweikert, Arizona’s 1st District

The Business Group on Health predicts a 7.8% rise in overall healthcare spending in 2025, partly due to GLP-1 therapies.

Reinsurance Strategy Considerations

Specific (High-Excess) Claims – Per Member Exposure

Respondents to recent market surveys — compiled by Gallagher Re — were largely in agreement that the immediate effect of GLP-1s on specific stop-loss coverage is negligible (see about U.S. Employers Health Care Insurance Costs and how to reduce healthcare price?).

GLP-1 medications cost in the range of $10,000 to $12,000 per member per year, and they typically do not breach common high-excess deductibles.

However, costs tied to complications of using these therapies, such as pancreatitis, gallbladder disease or severe gastrointestinal issues, may increase exposure to large claims.

Thus far, insurers do not see a dramatic increase in catastrophic claims linked directly to GLP-1 usage, although some note that future expansions of GLP-1 indications (e.g., heart failure, Alzheimer’s) could alter (reduce) high-excess risk profiles over time.

Aggregate (Total Claim Exposure)

While GLP-1 use has not significantly affected specific stop-loss rates, most insurance carriers anticipate a modest impact on aggregate medical cost trends.

Because many employees and dependents are adopting GLP-1 therapies for weight loss or pre-diabetes — often beyond strictly type 2 diabetes indications — carriers forecast a rising aggregate PMPM.

As an example, for a group of 150 employees and 150 dependents, if even 20% of eligible members initiate a $10,000-per-year GLP-1 therapy, the aggregate spend exposure could increase by $600,000.

Although actual utilization rates may vary significantly, carriers are recalibrating their underwriting manuals each year to capture this evolving risk.

Cost Projections and Underwriting Adjustments

Gallagher Re projects that GLP-1 drugs could add 1-2% to medical trend costs. For instance, a group of 150 employees and 150 dependents, with 20% using GLP-1 therapies at $10,000 per year, may see up to $600,000 in additional spending exposure.

According to US Health Insurance Market Trends report, the year 2024 marks the tenth year of operation for the US health insurance exchanges since they launched as part of the Affordable Care Act in 2014. The individual market has remained fluid during this time, with insurer participation, pricing, and plans changing from year to year.

Average annual health insurance premiums in 2024 are $8,435 for single coverage and $23,968 for family coverage. These average premiums each increased 7% in 2024. The average family premium has increased 22% since 2018 and 47% since 2013.

This surge in costs prompts employers and reinsurers to revise underwriting models to manage emerging financial pressures.

Risk Factors and Complications

Gallagher Re’s research indicates that the immediate impact of GLP-1 therapies on specific stop-loss coverage is minimal. However, potential risks include pancreatitis, gallbladder disease, and severe gastrointestinal issues.

Insurers have not yet reported a significant rise in catastrophic claims linked directly to GLP-1 use.

Expansions in GLP-1 indications, such as for heart failure and Alzheimer’s, could alter future risk profiles.

Broader Adoption and Its Implications

While GLP-1 therapies’ impact on stop-loss rates remains modest, aggregate medical costs face more significant challenges.

Many employees and dependents now use GLP-1 therapies for weight loss or pre-diabetes, extending beyond the original indication for type 2 diabetes.

This broader adoption increases per-member-per-month (PMPM) costs.

As more individuals use these therapies, insurers update underwriting manuals to account for changing risks. Though the therapies could reduce long-term chronic condition costs, short-term financial impacts remain unpredictable.

Adherence and Discontinuation Challenges

Studies by Prime Therapeutics show that up to 85% of patients discontinue GLP-1 therapies within two years, primarily due to side effects, cost, or insufficient weight loss.

Among patients with type 2 diabetes, 46% stop treatment within a year, and 65% without diabetes also discontinue.

Many restart therapy after regaining weight. These patterns make it challenging to project long-term savings, as short-term costs from complications might offset potential gains.

Elective Surgery Trends and Weight-Loss Outcomes

An emerging topic among medical risk experts, including Gallagher Re, is how GLP-1-induced weight loss may influence elective surgeries.

Some expect fewer joint replacements as patients lose weight, while others predict an increase once patients reach a lower BMI.

Additionally, skin reduction and hernia repair surgeries may become more common, impacting overall cost trends.

Underwriting Strategies and Cost Monitoring

Gallagher Re recommends closely monitoring cost drivers related to GLP-1 therapies. Coverage inconsistencies among third-party administrators (TPAs) make it essential to align plan design with underwriting assumptions to minimize unexpected exposures.

Given ongoing uncertainties around adherence and outcomes, most stop-loss and reinsurance carriers are waiting for more claims data before applying targeted surcharges or discounts for GLP-1 coverage.

Though the long-term potential for cost savings exists, carriers remain cautious about integrating these benefits into their underwriting models without solid evidence.

Future Developments and Market Outlook

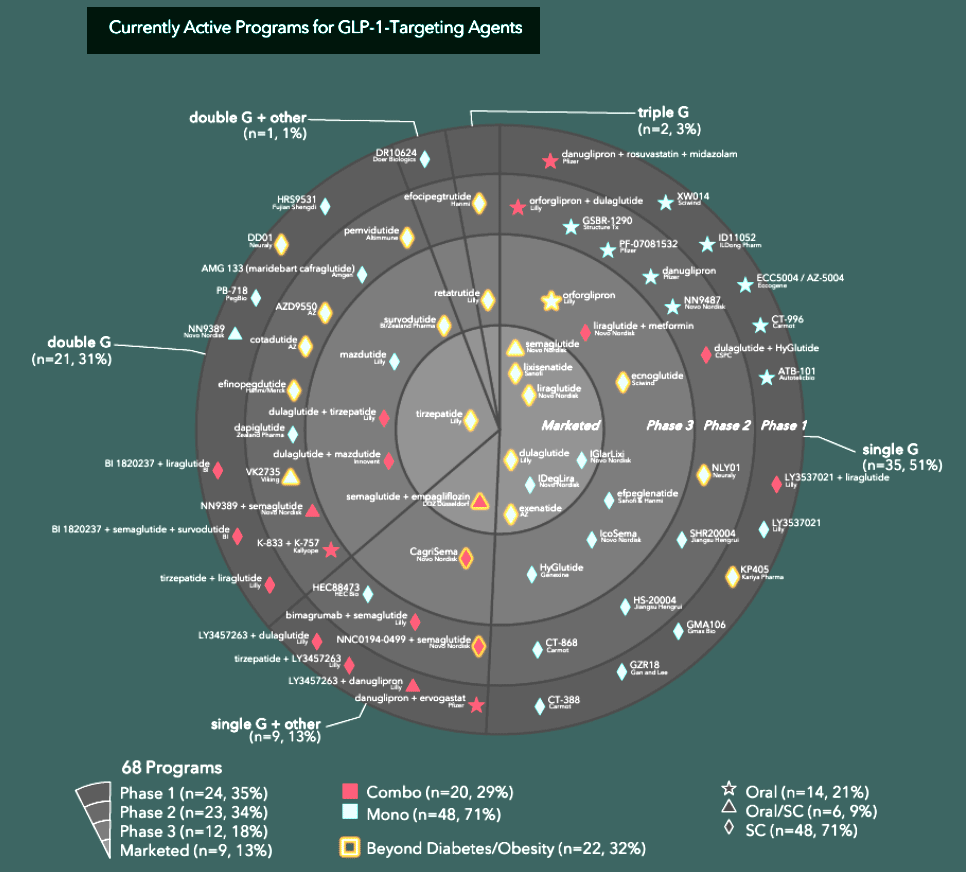

The pipeline for weight-management medications is expanding, including compounded GLP-1s and potential biosimilars. These treatments may lower costs but raise new safety and efficacy challenges.

Insurers must stay alert to these developments and update aggregate trend assumptions as needed.

GLP-1 therapies are expected to increase in use, driven by expanded indications, improved formulations, and personalized medicine approaches.

Rising rates of obesity and diabetes, along with regulatory approvals, will likely boost adoption, prompting ongoing adjustments to underwriting and pricing models.

- Though short-term stop-loss claims remain relatively stable, aggregate costs are susceptible to changes from higher usage rates, side effects, and elective surgery trends.

- Long-term savings may materialize if adherence rates improve and clinical outcomes are validated.

Insurers must remain agile, updating models and assumptions as new data emerges.

Expanded Indications and Applications

GLP-1 therapies are currently being explored for a range of conditions beyond type 2 diabetes and obesity, including non-alcoholic steatohepatitis (NASH), cardiovascular diseases, and neurodegenerative disorders such as Alzheimer’s disease.

These expanded indications could potentially alter the risk profiles and cost structures associated with these medications, significantly increasing risk exposure to both specific and aggregate stop-loss claims.

Improved Formulations and Patient Compliance

Advancements in GLP-1 formulations, such as longer-acting injections and oral versions, are expected to improve patient adherence and convenience.

This could lead to more consistent therapeutic outcomes and potentially reduce the incidence of obesity-related comorbidities, thereby influencing long-term claims trends.

Combination Therapies and Personalized Medicine

The development of combination therapies involving GLP-1s and other medications may enhance efficacy and broaden therapeutic applications.

Additionally, personalized medicine approaches could optimize treatment plans based on individual patient profiles, potentially improving outcomes and reducing costs.

Market Growth and Regulatory Approvals

The market for GLP-1s is projected to grow as more individuals are diagnosed with diabetes and obesity and as awareness of these therapies increases.

Continued regulatory approvals for new indications and formulations will likely expand their use, necessitating ongoing adjustments in underwriting and pricing models.

Potential Impact on Long-Term Medical Costs

While the short-term cost implications of GLP-1 therapies are still being assessed, their potential to reduce the burden of chronic diseases could lead to significant long-term savings.

However, this will depend on improved adherence rates and the realization of substantial clinical benefits.

For reinsurance carriers, monitoring these developments is crucial for refining aggregate trend assumptions and underwriting guidelines.

As the pipeline for weight-management medications expands, including potential biosimilars, carriers must remain vigilant about safety, efficacy, and cost implications.

FAQ

GLP-1 receptor agonists are medications used primarily for type 2 diabetes and obesity management. They have gained attention due to their potential to improve health outcomes but also raise concerns about rising prescription costs and long-term claims management.

Rapid adoption of GLP-1 therapies has led to higher prescription spending, with some employer-sponsored plans reporting up to 9% of prescription costs attributed to these medications. The overall healthcare spending is projected to rise by 7.8% in 2025, partly driven by GLP-1 usage.

While GLP-1 therapies generally show positive health outcomes, potential risks include pancreatitis, gallbladder disease, and gastrointestinal issues. Though insurers have not observed a significant rise in catastrophic claims linked directly to GLP-1 usage, future expansions of indications could alter risk profiles.

The immediate effect on specific stop-loss coverage is minimal, as most high-excess claims thresholds are not breached. However, aggregate costs may rise as more employees and dependents use these therapies for conditions beyond type 2 diabetes. For instance, a group of 150 employees and 150 dependents could see a $600,000 increase in aggregate spending if 20% use GLP-1 therapies.

Up to 85% of patients discontinue GLP-1 therapies within two years, often due to side effects, cost, or lack of sustained weight loss. High discontinuation rates make long-term cost projections uncertain, as many patients may resume treatment if weight is regained.

Weight loss from GLP-1 therapies could reduce the need for joint replacement surgeries. However, as patients reach lower BMI levels, some surgeries, like skin reduction or hernia repair, might become more common, impacting overall cost trends.

Advancements like longer-acting formulations, combination therapies, and new indications could improve adherence and expand applications. As the market grows and regulatory approvals increase, underwriting models and pricing strategies will need ongoing adjustments.