Overview

India’s Insurance industry is one of the premium sectors experiencing upward growth. This upward growth of the insurance industry can be attributed to growing incomes and increasing awareness in the industry.

India is the fifth largest life insurance market in the world’s emerging insurance markets, growing at a rate of 32-34% each year.

In recent years the industry has been experiencing fierce competition among its peers which has led to new and innovative products within the industry, according to Invest in India Report.

Key figures of the Indian insurance market:

- Total Written Premium (Life Insurance) $81.3 bn

- Gross Direct Premium Income (Non-Life Insurance) $27 bn

- Share of New Business Premium in Total Premium (Life Insurance) 45.25%

- Share of Motor Premium in Total Non-Life Premium 34.1%

Foreign Direct Investment (FDI) in the industry under the automatic method is allowed up to 26% and licensing of the industry is monitored by the insurance regulator the Insurance Regulatory and Development Authority of India (IRDAI).

Indian Insurance market stands at $131 bn as of FY2022. The Indian insurance industry grew at a CAGR of 17% over the last two decades and is expected to continue its commendable growth trajectory in the future years.

- The insurance industry in India has 58 insurance companies, including 34 non-life insurers (25 general insurers, 7 standalone health, 2 specialized insurers). The insurance industry in India has witnessed an impressive growth rate over the last two decades driven by the greater private sector participation and an improvement in distribution capabilities, along with substantial improvements in operational efficiencies

- Private Life Insurers are expected to grow their retail APE at a CAGR of over 17% between 2021-2023, and new retail term premiums are expected to double in 5 years. The Private Non-Life insurance segment is forecasted to grow at 16% in FY22 and 14% in FY23. Standalone Health Insurers are expected to grow by over 25% in FY22 due to the increased focus on healthcare.

- The New Business Premium for Life Insurers has grown at a CAGR of 14% over FY14-20 led by the financialization of savings and new product launches, and the insurance industry size in India is expected to grow at 12.5% CAGR over the next decade 2020-30 led by specialized products such as protection and annuities.

- Non-life insurers Collective gross direct premium underwritten for non-life insurance companies grew 22.99% y-o-y to INR 54,491.27 Cr for the first quarter this fiscal from INR 44,303.91 Cr for the same period last fiscal.

Among the life insurers, Life Insurance Corporation (LIC) is the sole public sector company. There are six public sector insurers in the non-life insurance segment. In addition to these, there is a sole national re-insurer, namely General Insurance Corporation of India (GIC Re).

Other stakeholders in the Indian Insurance market include agents (individual and corporate), brokers, surveyors and third party administrators servicing health insurance claims.

What are the classes of insurance business for which a registration application can be made?

- Life insurance business

- General insurance business

- Health insurance business exclusively

- Reinsurance business.

Indian isurance industry scenario

India is ranked 11th in Global Insurance business. India’s share in global insurance market was 1.72% and total insurance premium volume in India increased by 0.1%.

- India’s insurance penetration was pegged at 4.2%, with life insurance penetration at 3.2% and non-life insurance penetration at 1%.

- The market share of private sector companies in the non-life insurance market rose from 15% in FY2004 to 50%.

- In terms of the size of insurance industry in India, the share of life insurance in total premium in India is 75.24% and the share of non-life premium is 24.76%.

- Life insurers recorded new business premium of INR 2.78 Tn ($38 Bn) growing at 7.49% over the last year with private life insurers growing at 16.29%. Private Life Insurers account for 33.8% of the industry’s new business premium with the rest being accounted for by the Life Insurance Corporation of India (LIC).

- The Life Insurance Industry in India recorded a total premium of INR 5.73 Tn ($81.3 Bn) in FY20 witnessing a growth of 12.75% over the previous year and the private insurers accounted for 33.7% of total premium underwritten by the industry. New business premium contributed 45.25% of the total premium and witnessed a strong growth of 20.59%. 60% of the new business premium was derived from single premium with remaining 40% accounted for by first year premiums.

- During the last year, life insurers issued 288.47 lakh new individual policies, out of which LIC issued 75.9% of policies and the private life insurers issued 24.1% of policies.

- Non-life insurers (comprising general insurers, standalone health insurers and specialized insurers) recorded a 5.19% growth in gross direct premiums.

- Motor insurance accounted for 34.1% of the non-life insurance premiums earned, followed by health insurance at 29.5%, Post-Covid rising demand for personal mobility space is leading to a shift in vehicle ownership patterns and may create an opportunity for motor insurers.

- Health insurance witnessed 13.3% growth in GDPI, while fire insurance and liability insurance observed 28.1% and 16.4% growth respectively in the same period.

- AB PM-JAY is an entitlement-based scheme under Ayushman Bharat and is fully funded by the Government. It is the largest health assurance scheme in the world and aims at providing a health cover of INR 500,000 ($6,900) per family per year for secondary and tertiary care hospitalization to over 107 Mn vulnerable families (approximately 500 Mn beneficiaries).

- Digital issuance and online channels are expected to witness continued growth, the share of web aggregators within digital insurance has been constantly increasing and web-aggregators currently originate 30-40% of digital insurance.

- The total mortality protection gap in India stands at $16.5 Tn with an estimated protection gap of 83% of total protection need. This offers a huge opportunity to life insurers with an estimated additional life premium opportunity of average $78.2 Bn annually

- The retail protection sum assured is estimated to grow 8X by over 2020-30, implying 23% premium CAGR

- India is the 2nd largest InsurTech market in the APAC region, accounting for 35% of the $3.66 Bn capital invested in this region. The online individual insurance market opportunity is estimated to be $1.25 Bn by FY25 more than tripling from $365 Mn in FY22.

Indian Life & Health Insurance

Indian Life and Health Insurance Market recorded year-over-year profit improvement, a trend that is set to continue thanks to rising interest rates and claims normalization, according to S&P Global Market Intelligence analysis.

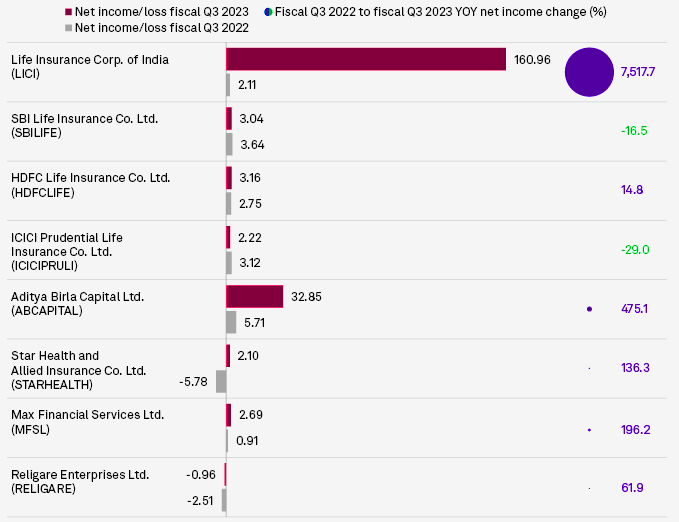

Life Insurance Corp. of India had the largest year-over-year profit growth of eight insurers. The company’s net income surged to 160.96 bn rupees from 2.11 bn rupees in the prior-year quarter.

Aditya Birla Capital followed with a 475% year-over-year profit growth. The insurer booked a net profit of 32.85 bn rupees in the fiscal third quarter, up from 5.7 bn rupees in the year-ago quarter.

Net income/loss of Indian Life & Health Insurers

Two of the eight insurers, ICICI Prudential Life Insurance Co. and SBI Life Insurance Co. Ltd., reported year-over-year declines in net income during the quarter.

ICICI Prudential Life reported net income of 2.22 bn rupees, down 29% from 3.12 bn rupees in the year-ago period, while SBI Life’s fiscal third-quarter net income declined 16.5% year over year to 3.04 bn rupees from 3.64 bn rupees.

Life Insurance in India

India is a huge leader in terms of life insurance uptake. A 3.2% penetration means India ranks 10th in the global life insurance market and ahead of China (at 2.4%) and the UK (at 3%).

Adoption of life insurance in India is expected to increase because there is great awareness of the need for financial security, regulations regarding approval, product customisation and distribution have been updated, and mobile-ready insurtech products are far more palatable to the consumer.

This is bourne out in the 91% of respondents who said their perception of life insurance has changed, from being viewed as an investment to being for protection. Furthermore, 55% revealed they’d purchased their cover through an insurance agent, while 23% bought it online, from bank portals, web aggregators, and website direct purchase

The instability of the covid-19 pandemic highlighted the necessity for consumers to invest in products that would increase financial security, one of them being life insurance.

Life Insurance Premiums in Indian Market

Premium income up nearly across the board

7 of the 8 Indian life and health insurers posted higher net premium income in the fiscal third quarter, while Aditya Birla’s premium income data was not available.

Life Insurance Corp. of India recorded 14.5% year-over-year growth in net premium income during the period. The insurer booked net premium income of 1.123 trln rupees during the quarter, compared with 980.52 bn rupees in the prior-year quarter.

Indian Life & Health insurers profit tailwinds

The Swiss Re Institute is cautiously optimistic about the continued normalization of Indian life insurers’ earnings after pandemic-related claims impacted earnings.

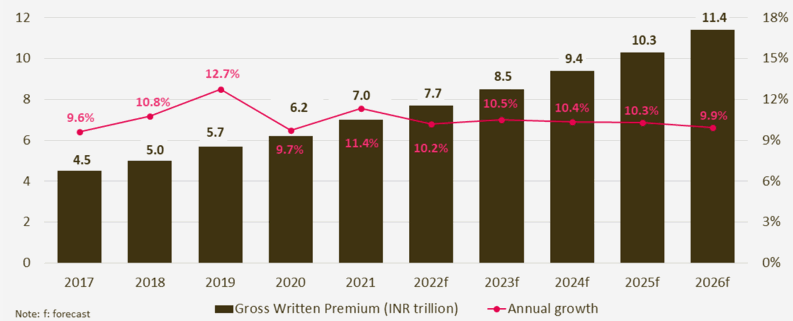

Full-year life insurance premium volumes to surpass US$100 bn for the first time, representing growth of 8% in real terms.

A series of regulatory developments introduced by India’s insurance regulator could also support sector growth, the organization said, including the introduction of risk-based capital solvency requirements.

The move to a risk-based capital approach would be “more sustainable” for Star Health and Allied Insurance Co. Ltd., allowing the company to keep growing its business because there is no pressure on solvency, CFO Nilesh Kambli said during an earnings call.

The risk-weighted approach for capital allocation should result in a freeing up of capital in certain cases, possibly for larger insurers with more diversified underwriting portfolio, while requiring higher capital requirements on insurers underwriting more risky business

Swiss Re Institute

ICICI Prudential Life will “not require external equity capital in the foreseeable future,” according to CEO N.S. Kannan, in light of the introduction of the risk-based capital requirement, combined with the insurer’s ability to raise further Tier 2 capital and its strong solvency position.

Foreign investments in Indian insurers

The Indian insurance regulator IRDAI has allowed foreign investors, including foreign portfolio investors (FPIs), to invest in preference shares and subordinated debt issued by Indian insurers.

The regulator has also now allowed the subordinated debt issued by the Indian insurers to be listed on local stock exchanges but not on overseas bourses.

According to Asia Insurance Review, in a new set of regulations titled “Other Forms of Capital) Regulations, 2022”, the regulator stipulates that the quantum of investments by foreign investors, including foreign institutional investors (FII)/ foreign portfolio investors (FPIs), in the two kinds of instruments — preference shares and subordinated debt— cannot exceed the sectoral cap specified by the Foreign Exchange Management Act (FEMA).

IRDAI stipulates that the total quantum of the instruments under ‘Other forms of capital’ taken together should be the lower (at any point in time) of 50% of the total paid-up equity share capital and securities premium of an insurer or 50% of the net worth of the insurer.

The Insurance Regulatory and Development Authority of India has said insurers will be allowed to classify their sovereign green bond purchases as infrastructure investments.

The regulator, in a circular dated Jan. 13, said the move was made with the objective of “de-concentration and diversification” of insurers’ infrastructure portfolios as well as “from the perspective of participation in environmental, social and governance (ESG) initiatives.”

……………………..

AUTHORS: Rozelle Alyssa Javier, Kris Elaine Figuracion – S&P Global Market Intelligence analytics, Atharv Mankotia – Insurance Sector Expert at BFSI Insurance

Edited & fact-checked by Oleg Parashchak – Editor-in-Chief Beinsure Media, CEO Finance Media Holding.