Alternative investment managers are warming to catastrophe bonds tied to wildfire risk, a corner of the market many avoided not long ago because modeling looked shaky at best. That hesitation is fading.

More than $5 bn of cat bonds with some wildfire exposure priced this year, according to Artemis, which tracks insurance-linked securities issuance.

According to Insurance Journal, that figure more than doubles 2024 volumes. In prior years, wildfire-linked deals barely registered, often limited to isolated tranches measured in tens of millions.

Wildfire bonds remain a small slice of the market, yet they helped push total 2025 cat bond issuance to a record $23 bn jump. Outstanding volume now trends toward $60 bn by year-end.

Acrisure Re says the shift traces back to better modeling, which pulled fund managers into what it calls a once untouchable risk bucket.

Dirk Schmelzer, senior fund manager at Plenum Investments AG, says the change hints at a structural shift in how some catastrophe risk reaches capital markets. Wildfires, he argues, no longer fit neatly inside broader peril pools.

Historically, wildfire exposure sat alongside earthquake and hurricane risk. Schmelzer says the scale and frequency now justify standalone structures. The industry, he adds, increasingly leans on capital markets as fires grow more destructive.

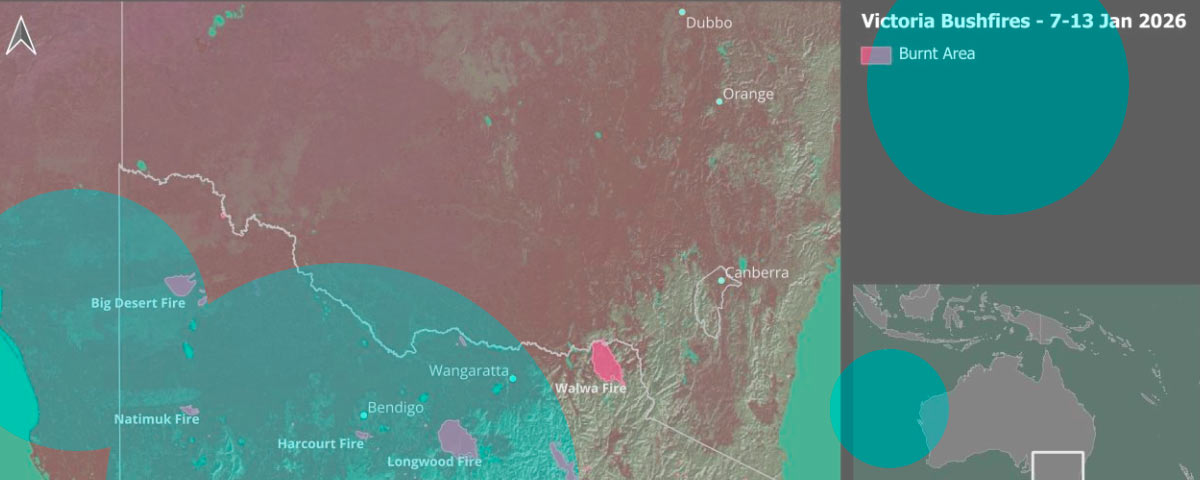

California sits at the center of this recalibration. Reinsurance tied to wildfire risk has grown expensive after consecutive severe seasons.

The January fires in Los Angeles destroyed more than 16,000 buildings and drove insured losses to a record $40 bn.

Those fires pushed global insured catastrophe losses beyond $100 bn in 2025, marking the sixth straight year above that line. Cat bond investors barely felt it. Fitch Ratings’ early estimate puts total losses to cat bond holders below $250 mn.

As climate-driven urban fires turn into a recurring threat, insurers and utilities look for relief beyond traditional reinsurance. Capital markets offer one outlet.

The California FAIR Plan Association recently tested that route. Its debut wildfire cat bond priced this month and is set to raise $750 mn of cover, triple the initial target, according to a person familiar with the deal who requested anonymity due to confidentiality.

The source described it as the largest pure wildfire cat bond to reach the market.

Other regions are watching closely. Colorado lawmakers have introduced legislation that would allow the use of cat bonds to manage growing wildfire exposure across the state.

Performance helps explain the demand. The Swiss Re Global Cat Bond Performance Index is up about 11% in 2025. A Bloomberg index tracking US corporate bonds gained roughly 7%.

US Treasuries returned about 6%. The S&P 500 rose close to 15%. Cat bonds also behave differently when markets wobble. When tariff announcements rattled markets in April, cat bonds largely held steady.

Twelve Securis expects primary issuance in 2026 to stay heavy as tighter spreads lower issuance costs. Etienne Schwartz, the firm’s CIO of liquid strategies, says reinsurers will likely move more risk, including secondary perils, into capital markets. We think wildfire risk sits squarely in that pipeline.