Overview

Swiss Re’s annual SONAR report identifies new or changed risks that are difficult to quantify and could have a major impact on society and industry. By providing early insights into evolving risks, the report helps businesses and insurers make better-informed strategy decisions. Beinsure selected the most important things from the report.

New report features eight emerging risks selected through Swiss Re’s regular risk identification process and seen as deserving of insurer attention for their novelty, dynamics and/or deemed urgency.

The choice is based on horizon scanning through monitoring tools for early signal detection and research, in-house vetting and input from external scientists, clients and industry peers.

Emerging risks reported in SONAR in earlier years feature again only if developments are deemed to be of significant degree to warrant renewed consideration.

Executive summary

- SONAR promotes awareness of risks that matter to insurers today and those that will in the future.

- Structural risks impacting the insurance industry already today include lack of consumer trust and excess mortality.

- In terms of risks for the future, rising global temperatures could increase claims in many lines of business.

- Plastics are another concern, given environmental and health impacts. Earliest claims traction is likely to show in liability insurance.

- Ultra-processed foods could trigger liability and health claims… while the broadening scope of use of digital technology in daily life presents both opportunities and challenges for insurers.

SONAR also flags new exposures we deem deserving of attention, but with potentially lower impact and maturation likely more in the longer than near term. These risks include the rapidly rising consumption of ultra-processed foods.

The latter could spark rising claims in liability and health, as evidence of associated negative health outcomes like obesity and diabetes mounts.

We also flag the potential insurance ramifications of digital innovation such as the deployment of deepfakes and the dissemination of disinformation through social media, and the growing role of digital technology in healthcare delivery, all of which will likely impact Life and Health insurance (L&H) and casualty lines of business.

Other technology-innovation context emerging risks are the use of drones for strategic purposes, and how artificial intelligence will likely influence workplace skill set needs in the future.

In addition to more claims in L&H and casualty, the latter could also increase the cost of providing insurance in situations where automation leaves a lack of sufficient job-specific human talent and where this, in turn, leads to an increase in operational errors.

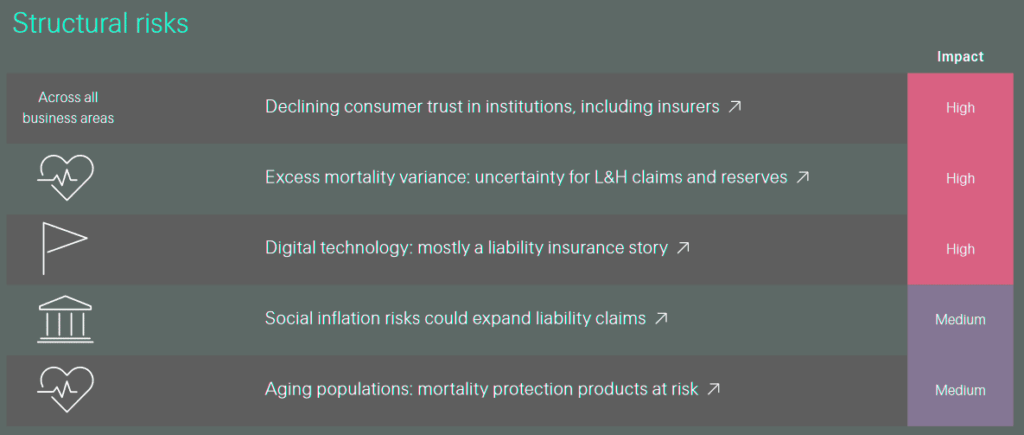

Existing challenges for the insurance industry

The insurance industry faces several ongoing challenges linked to long-term economic, social, and environmental trends. These structural risks require active management to ensure protection for policyholders, continued economic stability, and the sustainability of insurers’ business models.

Key risks currently affecting the sector include reduced public trust in institutions, population aging, increased claim severity driven by social inflation, shifting mortality trends, and the effects of digitalisation.

Each of these areas presents both operational risks and potential areas for strategic adaptation.

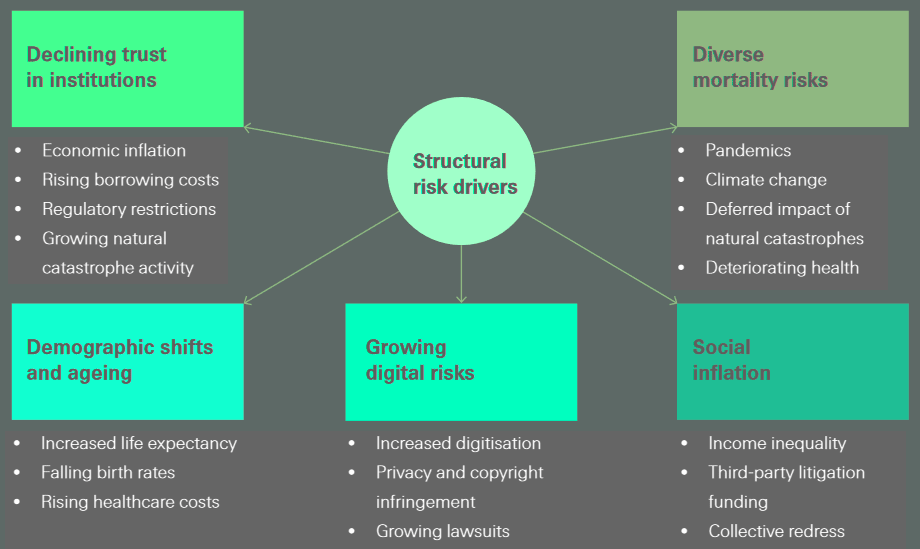

Structural risks and their underlying drivers

Declining consumer trust in institutions, including insurers

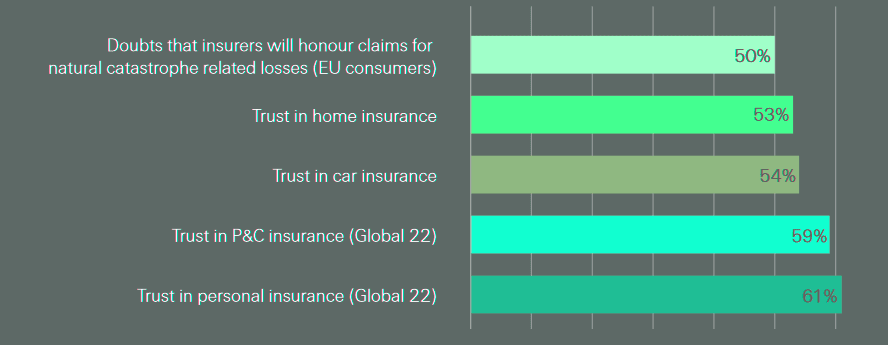

Consumer trust in institutions, including insurance companies, continues to decline. A 2025 Edelman Trust Barometer report found that 61% of respondents expressed moderate to high levels of grievance against businesses and governments.

Notably, 40% supported forms of hostile activism, including property damage and violence, as a way to demand change.

Trust remains a key factor in insurance purchasing decisions across most markets. Over 80% of commercial insurance buyers consider trust an important element when selecting a provider.

When trust is low, policyholders may choose to switch insurers or avoid purchasing coverage altogether for specific risks. For example, concerns about whether insurers will honor claims or confusion caused by complex policy language can make customers less likely to complete purchases.

A lack of trust also creates reputational risk for insurance companies

The sector has experienced significant public skepticism in recent years. Multiple surveys suggest that fewer than two-thirds of consumers trust insurers.

A study conducted by the European Insurance and Occupational Pensions Authority (EIOPA) revealed that only 50% of respondents believed insurers would pay claims linked to natural catastrophes.

This is especially relevant as insured losses from natural disasters continue to grow at an annual rate of 5–7% when adjusted for inflation. In this context, maintaining consumer trust will require consistent and targeted efforts from insurers.

Low levels of trust in institutions

Social inflation risks could expand liability claims

Social inflation refers to the rise in insurance claims severity driven by non-economic factors. In the US, such factors contributed to 57% of the growth in liability claims over the past decade.

Since 2020, the number of nuclear verdicts—defined as jury awards exceeding $10 mn—has more than quadrupled, with the median award rising to $51 mn.

By 2024, the average award in cases against corporate defendants reached $65.7 mn, up from $41.7 mn in 2023, based on LexisNexis data reported by the Financial Times.

These developments have sharply impacted liability insurance, particularly in lines exposed to bodily injury claims. Over the five years to 2024, these lines in the US recorded cumulative underwriting losses of $43 bn.

The increase in legal awards has eroded profitability and contributed to reduced risk transfer capacity across the industry.

Aging populations: mortality protection products at risk

The world’s ageing population is being driven by increases in life expectancy and declining birth rates. According to data from the UN, the share of persons aged 65 and above in high-income countries is forecast to trend up through to the mid-2040s.

The number of 25 to 49 year-olds is expected to shrink 5% by 2050. 24 As life events like birth of a child can spur life insurance purchases, a population that is ageing implies lacklustre growth in demand for mortality protection and accumulation savings premiums. Fewer and later family formations magnify this headwind.

For the L&H industry, growing longevity risk pools (ie, ageing populations seeking health and retirement security) are a large premium opportunity.

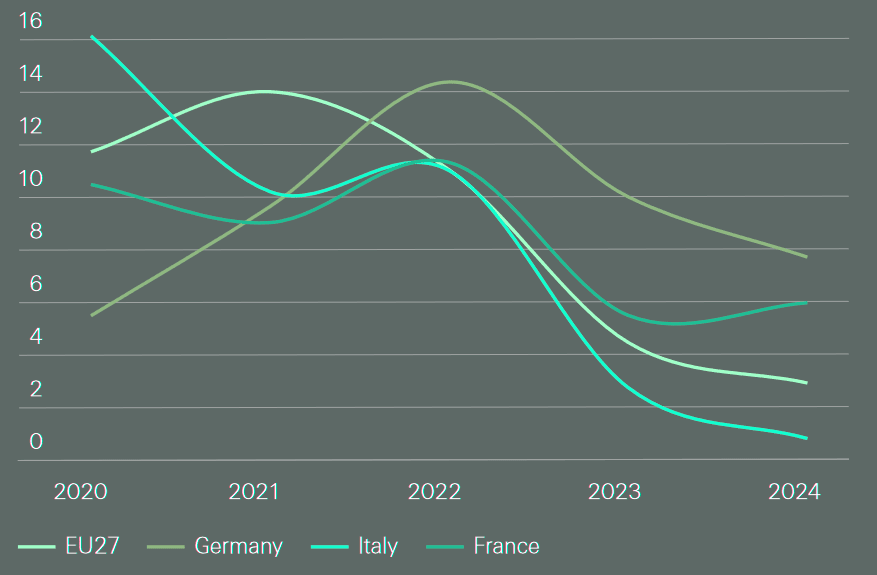

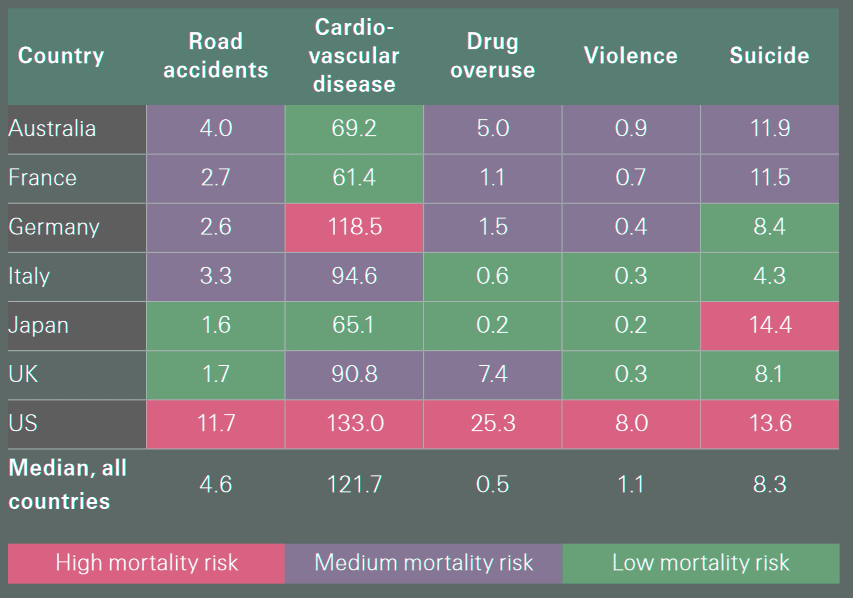

Tracking excess mortality in Europe over the years

A 65-year-old stopping work faces a 16% longer retirement than one who left the workforce in 2000, and nearly 40% more than someone who retired in 1975. This will continue as life expectancy post age 65 may rise to 20 years by 2050 (compared to 16.8 in 2020).

Using per capita medical expenses and proportion of population in age categories, we calculate that by 2050, the 65+ population in the US will account for almost 50% of health expenditure. In Japan, the 65+ age group already accounts for more than 60% of total spending on healthcare services.

Dispersion of factors driving excess mortality across countries, age-standardised death rates (per 100 000 population)

Long-tail liability lines are especially vulnerable to social inflation due to their exposure to legal system changes.

Between 2014 and 2023, median limits purchased for liability towers declined by nearly 25% in nominal terms and by 46% when adjusted for inflation, reflecting rising loss severity during that period.

Although the issue has primarily affected the US, similar trends are emerging in other regions. Europe is expected to see larger legal settlement awards in the next five years. This shift may be driven by greater access to litigation, expanding collective redress mechanisms, and a broader product liability framework.

Third-party litigation funding (TPLF), in the absence of specific regulation, could accelerate this trend. The European Union continues to promote collective actions across areas including data privacy, ESG, and product liability.

Digital technology: mostly a liability insurance story

Advancements in digital technology, especially artificial intelligence (AI), are changing liability exposure and may lead to increased demand for both first-party and third-party liability insurance.

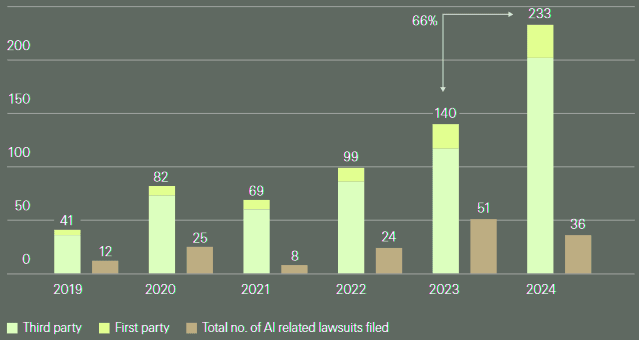

Between 2023 and 2024, reported AI-related incidents rose by over 60%, with one-third linked to system failures. As AI becomes more embedded in business operations and everyday use, the volume of associated legal claims is expected to grow.

Recent legal actions have included allegations of intellectual property infringement and defamation, with some cases involving large language models such as ChatGPT. These developments may contribute to broader social inflation effects.

Emerging technologies like generative AI (GenAI) also present new liability challenges, including exposure to advanced fraud schemes such as deepfakes.

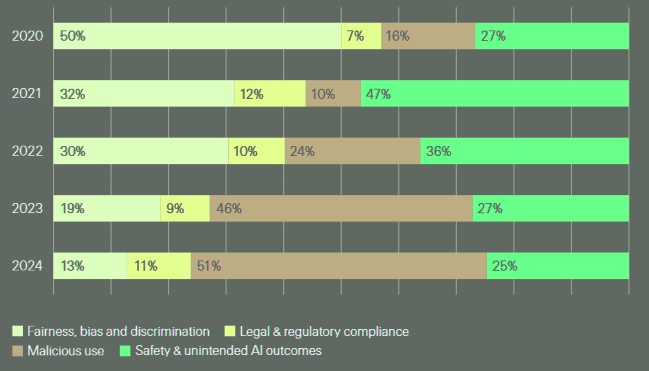

These risks generally fall into four categories: fairness, bias, and discrimination; legal and regulatory compliance; malicious use and safety; and unintended outcomes or product malfunction. Over time, incidents linked to bias and discrimination have declined, while those associated with malicious use have increased.

Insurers are still at the early stages of building products that address these risks. Current offerings lack consistency in coverage definitions, exclusions, and policy wording.

This uncertainty limits insurers’ ability to provide clear terms and manage claims effectively across digital technology-related exposures.

Number of AI incidents

Loss categories’ share of total losses

Elevated levels of excess mortality are a potential challenge for L&H insurance, with potentially several years of elevated mortality claims ahead, depending on how general population trends translate into the insured population.

Ongoing excess mortality can have implications for L&H claims and reserves. Excess mortality that continues to exceed expectations may affect the long-term performance of in-force life portfolios, and also the pricing of new life policies.

FAQ

SONAR highlights long-term emerging exposures that may have lower near-term impact but could become significant over time. Examples include increased consumption of ultra-processed foods, which may drive higher liability and health claims as links to obesity, diabetes, and other conditions strengthen.

Disinformation campaigns and deepfake content, especially through social media, are likely to increase liability exposures. These developments may affect Life & Health (L&H) and casualty lines due to reputational harm, fraud, and misinformation affecting decision-making in healthcare and business.

The integration of digital tools in healthcare, including AI-based diagnostics and remote monitoring, may result in operational and liability risks. Errors due to system failure or lack of regulatory clarity could increase claims in L&H and professional indemnity lines.

AI adoption can shift required job skills, and where automation replaces human roles, a lack of qualified staff may lead to higher operational error rates. These changes may raise the cost of insurance coverage, particularly in casualty lines.

Aging demographics reduce demand for mortality protection while increasing health and retirement claims. This shift affects premium growth potential and raises the share of health-related spending, which could strain L&H portfolios if not priced appropriately.

Non-economic drivers—such as litigation trends and large jury awards—have pushed up claim severities. Nuclear verdicts in the US have surged, raising insurer losses and reducing risk transfer capacity. This trend may expand to Europe due to collective redress mechanisms and third-party litigation funding.

Current insurance offerings for AI-related risks remain underdeveloped. Inconsistencies in policy wording and uncertainty around coverage limit insurers’ ability to handle claims effectively. As AI-related incidents increase, insurers will need to clarify terms and develop more precise coverage options.

…………………

AUTHORS: Dr Jerome Jean Haegeli – Head Swiss Re Institute and Swiss Re Group Chief Economist, Dr Thomas Holzheu – Chief Economist Americas at Swiss Re Institute, Jonathan Anchen, Dr Victor Blanco Gonzalez, Mitali Chatterjee, Dr Rainer Egloff, Andreas Felderer, Anna Mejlerö, Dr Anja Vischer, Bernd Wilke