Overview

With the rise of insurance technology and shifting customer demands, insurance brokers wanting to stay relevant need to constantly adapt and reinvent their strategies to help them achieve growth and profitability.

Brokers will continue to be a central part of insurance distribution and insurance companies will continue outsourcing insurance distribution and processing activities to them instead of building their direct insurance distribution system.

Insurance brokers are an essential part of the insurance industry, and their share in insurance premiums is significant. Insurance sold by brokers represents around 19% on average, but this rate can be as high as 80% for selected lines of insurance.

Insurance distribution will be heavily dependent on technology. It will drive business operations optimization and make customer interaction much more efficient.

Insurance companies and brokers will be increasingly more interconnected to be able to deliver real-time information and conclude policies and contracts online.

Insurance brokers face new challenges

- Regulatory Compliance: Keeping up with changing regulations requires constant vigilance and adaptation. Failure to comply can result in hefty fines and legal issues.

- Technological Advancements: Rapid technological changes demand continuous investment in new tools and platforms. Brokers must stay updated to remain competitive and meet clients’ expectations.

- Market Competition: Increasing competition from direct insurers and online platforms pressures brokers to differentiate themselves. Offering unique value propositions becomes essential.

- Customer Expectations: Clients now demand more personalized and faster services. Brokers need to enhance their customer service and engagement strategies to retain clients.

- Data Management: Managing and protecting large volumes of data poses a significant challenge. Brokers must invest in robust cybersecurity measures to prevent data breaches.

- Talent Acquisition and Retention: Attracting and retaining skilled professionals is crucial. Brokers need to offer competitive benefits and career growth opportunities to maintain a talented workforce.

- Economic Factors: Economic instability affects clients’ insurance purchasing decisions. Brokers must adapt their strategies to navigate economic fluctuations effectively.

Addressing these challenges requires strategic planning and a proactive approach.

Shifting customer expectations

Insurance customers’ requirements and demands have changed considerably over recent years. They want more information about insurance products than ever before to make an informed decision on the best insurance product for them.

The offering needs to be personalized, delivered through their preferred channel (digital, in-person, sales partner), and fast.

Failing to live up to these expectations will increasingly result in lost business.

Complex regulatory requirements

Regulatory constraints and changes are a fact of life in the insurance industry, and brokers are no exception.

The dynamic environment has seen new regulations regarding personal data protection, sales standards, and solvency requirements.

Keeping up with different regulatory requirements in different countries can be a challenge for brokers unfamiliar with the regulations in different countries.

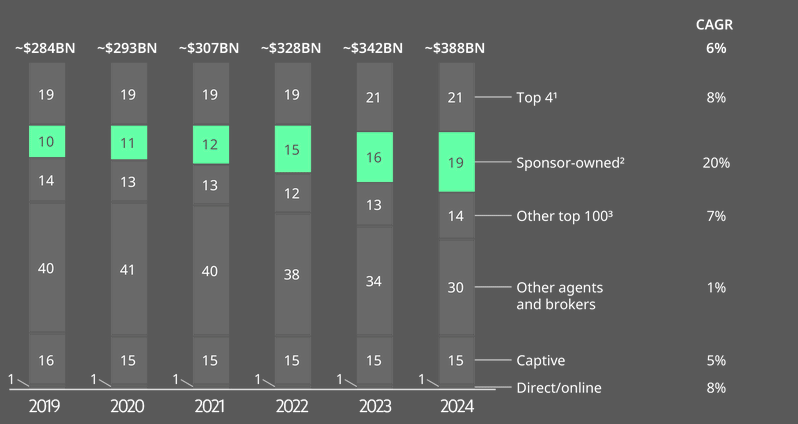

US P&C insurance Direct Written Premium by insurance broker segment

Sponsor-backed brokers now account for more than half of the top 30 brokers in the US across commercial, personal and employee benefits (EB) lines.

While a plurality of integration approaches has worked until now, financial sponsors and the management teams they support will have to work harder to integrate businesses and drive cross-organizational effectiveness to realize continued growth, especially considering the turning economic environment.

Technology shift

There is no doubt that the industry is under pressure from digitalization. Insurers need insurance brokers who understand technology to use it as an asset for their insurance company.

They need to be able to offer insurance products through digital channels and have a good understanding of how technology can help insurance companies grow.

Workflow and process efficiency

The business world is changing fast, but the nature and the way insurance brokers work haven’t changed.

As technology improves more than ever before, it’s important for them to evaluate their processes if they want to find success in an increasingly competitive market where slow growth projections are predicted.

For example, operational gaps and undefined sales processes can drag down the entire business. Successful brokers need to optimize their workflows to keep up with the sales demands and serve their customers.

An effective pipeline management process delivers tangible benefits – a recent study by VPP shows that companies who employ an effective pipeline management process were able to see 18% revenue growth – while those without show only 12%.

Insurance brokers are facing an increasingly challenging environment. Their industry and customers are changing along with increased competitive pressures from big tech companies and Fintech companies.

Transactional roles will simply not guarantee growth and success. Instead, insurance brokers need to play to their strengths and becoming trusted advisors that deliver a superior customer experience.

Technology will play a core role in this process. While more and more customers are ready to buy standard insurance products online and expect fast and sometimes contactless service, brokers can advise them about their risks and then help them locate the right products.

To do this, they need to focus on creating attractive digital experiences that create customer loyalty and drive satisfaction.

How the insurance brokering business is evolving in response to the challenges?

Here are some of the characteristics shared by insurance broker who want success and growth:

- Speed has become crucial for modern customers, who prioritize excellent service and dislike waiting for anything, including insurance quotes and policies. Insurance brokers need to provide digital solutions that offer insurance advice and empower insurance buyers to make the right decisions quickly. For example, digital quotes and digital policy documents allow customers to sign them electronically and conclude business faster.

- Customers are much better informed than in the past. This is a great opportunity since insurance brokers can bring their specific industry expertise to the table and recommend suitable products by various insurers that reflect actual risks. Well-informed customers also mean that brokers can provide much more detailed information and help their clients make better decisions that result in improved satisfaction.

- Growth often comes from complementary services and not just from growing the core business. No longer constrained to just brokerage services, insurance brokers now deliver additional value-added services, such as claims processing, risk management, or underwriting.

- Digital transformation should be at the top of the agenda. The failure to automate time-consuming processes insurance means falling behind and relying on manual processes reduces brokers’ competitive position and customer satisfaction.

- Insurance brokers will need new skills such as digital literacy and industry-specific information to advise customers about suitable insurance products from a range of insurers offering different policies. Brokers can leverage artificial intelligence and big data to deliver improved experiences and help their customers better manage risks.

Technology will also drive operational efficiencies and automate the processes that communicate information between the client and insurance companies.

Insurance brokers are looking at a bright future if they adapt to the changing landscape.

Digital transformation should truly be the top priority. Without it, the knowledge, the regulatory know-how and customer relationships will not count for much as customers shift to more agile start-ups and big tech competitors that deliver a better experience and more value.

FAQ

Insurance brokers face multiple challenges, including regulatory compliance, technological advancements, increased competition from direct insurers, and evolving customer expectations. Adapting to these demands requires brokers to stay updated, invest in new technologies, and continually enhance their service offerings.

Digital transformation is reshaping the industry by pushing brokers to optimize workflows, offer faster services, and meet clients through digital channels. By adopting digital tools, brokers can improve operational efficiency, reduce manual work, and create a seamless customer experience that keeps them competitive.

Compliance is essential to avoid legal issues and fines. With constantly changing regulations, especially around data protection and sales standards, brokers must remain vigilant and knowledgeable to operate effectively across different regions.

Customers now seek quick, personalized, and convenient insurance solutions. Brokers can meet these demands by offering digital quotes, electronic policy documents, and rapid response times, all of which align with modern expectations for efficiency and accessibility.

Technology enables brokers to provide real-time advice, personalized recommendations, and smooth policy management. With tools like artificial intelligence and data analytics, brokers can enhance the customer experience by offering tailored solutions that better align with individual risks.

Brokers can stand out by becoming trusted advisors rather than just transactional agents. Providing expert guidance, offering complementary services (like claims processing and risk management), and delivering a superior customer experience are key strategies to building long-term client relationships.

Digital literacy, regulatory knowledge, and an understanding of industry-specific risks are crucial for brokers. Leveraging data, staying informed about technological trends, and adopting new tools will help brokers deliver value-added services and adapt to the changing market.

……………………………

AUTHOR: Oleg Parashchak – CEO Finance Media & Editor-in-Chief at Beinsure Media