Overview

The insurance world has been pushed into uncharted territory in recent years, and 2024 will be no different. Advancements in everything from the speed at which product lines are being launched to the way customers are buying policies continues to change.

Accordint to Socotra Research, business leaders are tasked with improving customer retention, quickly launching new products, and delivering superior customer experiences, all while reducing their costs. The latest market trends outlined below can serve as a guidepost when it comes to navigating the changing market and remaining competitive.

Trends Insurers Should Expect

While the process of purchasing an insurance policy isn’t quite the same as buying a shirt from an online clothing retailer, today’s modern consumers expect better choices and more convenience.

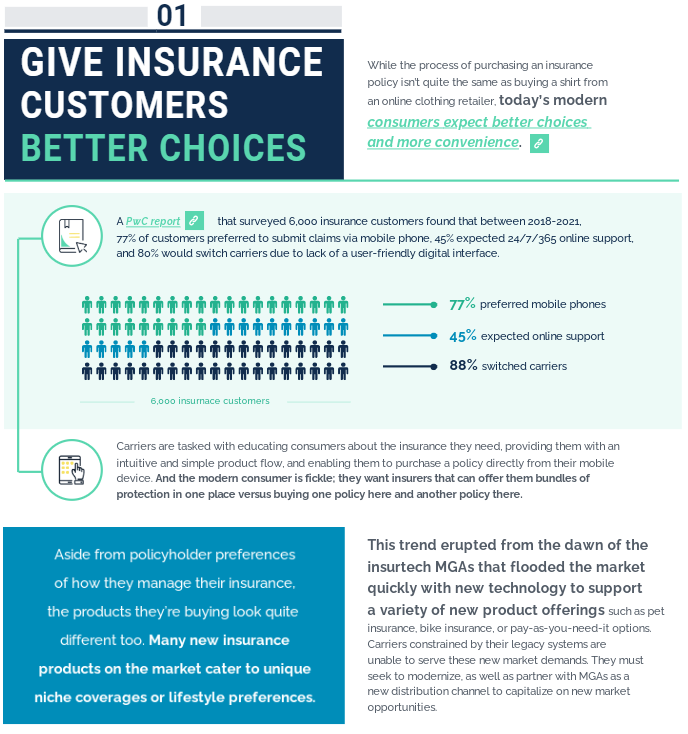

A PwC report that surveyed 6,000 insurance customers found that between 2018-2021, 77% of customers preferred to submit claims via mobile phone, 45% expected 24/7/365 online support, and 80% would switch carriers due to lack of a user-friendly digital interface.

Give insurance customers better choices

Carriers are tasked with educating consumers about the insurance they need, providing them with an intuitive and simple product flow, and enabling them to purchase a policy directly from their mobile device. And the modern consumer is fickle; they want insurers that can offer them bundles of protection in one place versus buying one policy here and another policy there (see 9 Key Customer Types that Will Define Insurance Market to 2030).

Aside from policyholder preferences of how they manage their insurance, the products they’re buying look quite different too.

Many new insurance products on the market cater to unique niche coverages or lifestyle preferences.

This trend erupted from the dawn of the insurtech MGAs that flooded the market quickly with new technology to support a variety of new product offerings such as pet insurance, bike insurance, or pay-as-you-need-it options. Carriers constrained by their legacy systems are unable to serve these new market demands. They must seek to modernize, as well as partner with MGAs as a new distribution channel to capitalize on new market opportunities.

Embedded takes center stage

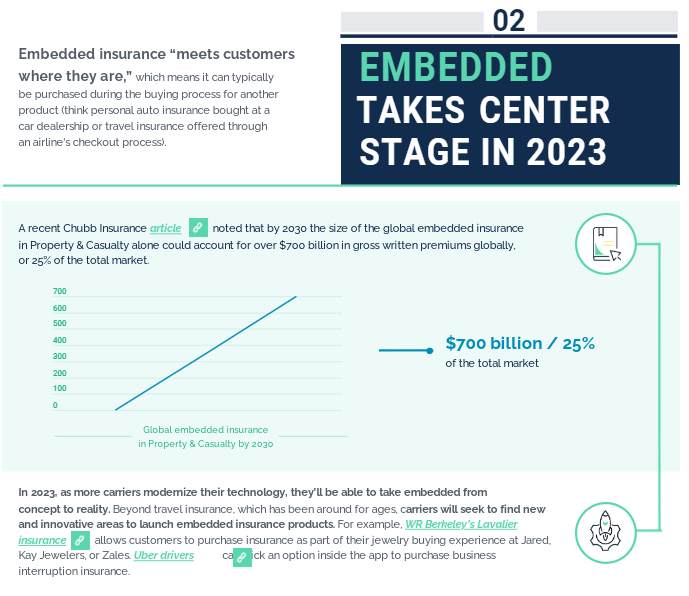

Embedded insurance “meets customers where they are,” which means it can typically be purchased during the buying process for another product (think personal auto insurance bought at a car dealership or travel insurance offered through an airline’s checkout process).

Chubb Insurance noted that by 2030 the size of the global embedded insurance in Property & Casualty alone could account for over $700 billion in gross written premiums globally, or 25% of the total market.

In 2024, as more carriers modernize their technology, they’ll be able to take embedded from concept to reality. Beyond travel insurance, which has been around for ages, carriers will seek to find new and innovative areas to launch embedded insurance products.

For example, WR Berkeley’s Lavalier insurance allows customers to purchase insurance as part of their jewelry buying experience at Jared, Kay Jewelers, or Zales. Uber drivers can click an option inside the app to purchase business interruption insurance (see New Era of Insurance Customers Experience).

Speed-to-market is more important than ever

It’s no secret that speed-to-market is crucial in today’s insurance industry. In 2024, attaining first-mover advantage with new product lines will be at the top of business leaders’ minds as they’re pressed to remain competitive in a changing market. Long gone are the days of legacy system launches that took years to come to market.

Carriers are now tasked with being the first to bring innovative products so that they can realize a faster increase in gross written premiums.

Deciding to rip and replace an outdated legacy system can be a hard choice for many business leaders to make. Many spend millions to maintain their legacy systems, build out whole teams to manage them, and feel that the potential updates are too much of a hassle.

But with the market moving at an ever-increasing pace, the real risk to business growth lies in doing nothing as these systems become more difficult and expensive to maintain. A recent Forbes article highlighted the point that when mission-critical hardware is offline for even one hour, the average cost of the resulting lost business is $300,000.

Usage-based insurance expands beyond auto

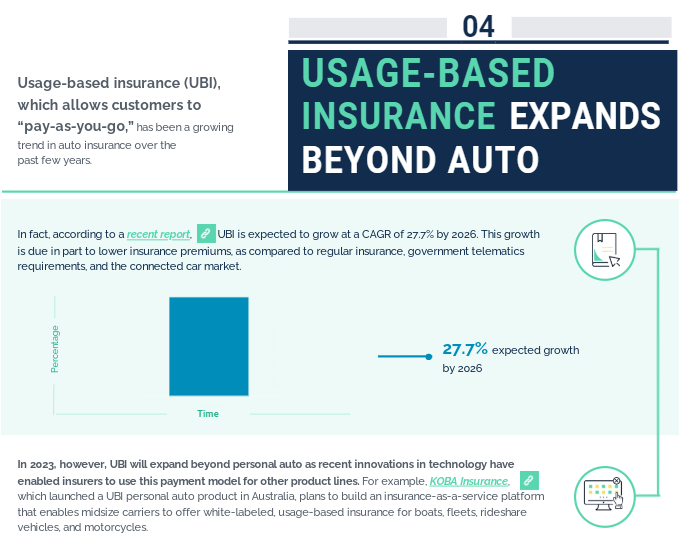

Usage-based insurance (UBI), which allows customers to “pay-as-you-go,” has been a growing trend in auto insurance over the past few years. In fact, according to a recent report, UBI is expected to grow at a CAGR of 27.7% by 2026. This growth is due in part to lower insurance premiums, as compared to regular insurance, government telematics requirements, and the connected car market.

In 2024, UBI will expand beyond personal auto as recent innovations in technology have enabled insurers to use this payment model for other product lines.

For example, KOBA Insurance, which launched a UBI personal auto product in Australia, plans to build an insurance-as-a-service platform that enables midsize carriers to offer white-labeled, usage-based insurance for boats, fleets, rideshare vehicles, and motorcycles (see how Usage-Based Auto Insurance Programs Have a Dramatic Increase).

The carrier-MGA relationship will continue to evolve

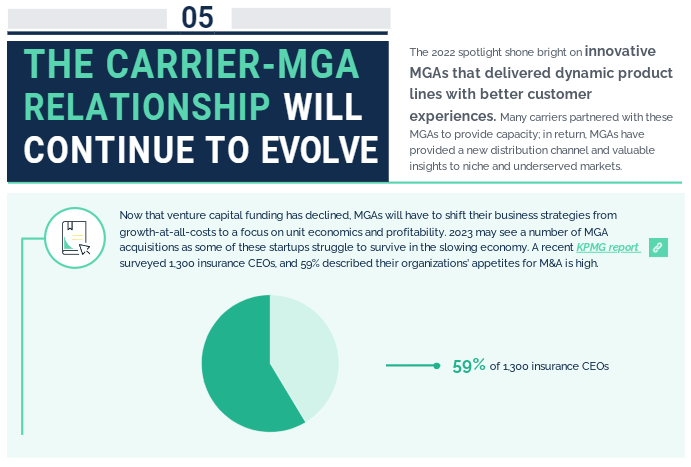

The 2022 spotlight shone bright on innovative MGAs that delivered dynamic product lines with better customer experiences. Many carriers partnered with these MGAs to provide capacity; in return, MGAs have provided a new distribution channel and valuable insights to niche and underserved markets.

Now that venture capital funding has declined, MGAs will have to shift their business strategies from growth-at-all-costs to a focus on unit economics and profitability. 2023 may see a number of MGA acquisitions as some of these startups struggle to survive in the slowing economy. A recent KPMG report surveyed 1,300 insurance CEOs, and 59% described their organizations’ appetites for M&A is high.

Mid-sized carriers will continue to feel the squeeze

2023 will see mid-sized carriers feeling the pressure from above and below as larger carriers increase market share and MGAs target niche markets. That’s because the big insurers in the U.S. are making strides in digital transformation and have the ability to compete on price and product delivery.

At the same time, smaller MGAs have the agility and tech to deliver innovative products faster to market, as well as better customer experiences. Meanwhile, mid-sized carriers will face challenges with scale to both invest in new systems and develop new products.

Looking ahead

In 2024 the insurance industry will continue to follow in the tech world’s steps by rapidly innovating and shifting the way it does business in order to better serve its modern customers. Carriers can remain competitive by establishing a plan to innovate now (see Сloud Technology for Insurance Industry).

Modernizing outdated legacy systems allows carriers to meet consumer expectations of choice and convenience, and remain competitive in this changing market by:

- Getting first mover advantage, improving customer retention, and quickly delivering the diverse lines of products and services modern customers expect

- Offering embedded products by leveraging open APIs that enable cross-industry collaborations and seamless ecosystems

- Expanding revenue streams with usage-based insurance products

- Distributing innovative white label products developed by partner MGAs

- Achieving a faster ROI by bringing new products to market quickly

……………………………

AUTHOR: Oleg Parashchak – CEO Finance Media & Editor-in-Chief at Beinsure Media by Socotra Data