Overview

After COVID-19, supply chain security became a top priority for management. Two to three years later, cost reduction has taken precedence again, according PwC Survey about Digital Trends in Supply Chain. Reduced investment in supply chains lowers their resilience to natural disasters, unexpected technology outages, and political events, increasing the risk of business interruption losses. As the COVID-19 pandemic experience showed, supply chains can be heavily disrupted, bringing long-lasting implications, according to Swiss Re Institute’s SONAR Report.

The world is facing a poly-crisis of interconnected and complex new and emerging risks, driven by climate change, geopolitical instability, social inequality, digital transformation, and health challenges.

Supply chain resilience is preventing breakdowns in delivery value chains, and the ability to quickly recover, rearrange and/or mobilise alternative delivery routes.

Safeguarding supply chains can help companies maintain market share and profits, which a narrow focus on cutting spending on supply chains cannot. Looking back at former SONAR reports, supply chain risk has been a recurring theme (see New Opportunities for Transport & Logistics Supply Chains Insurance).

The majority of the articles have focused on external risk drivers like natural catastrophes or politics (ie, disruptive events that are beyond direct influence of supply chain management). For many of these drivers the current outlook is negative.

Effective use of technology in supply chains

In an increasingly digital world with ongoing operational disruptions, effective use of technology in supply chains is crucial. Digital investments not only reduce costs, improve efficiency, and build resilience but also mitigate risks and address environmental, social, and governance (ESG) issues.

However, PwC’s Survey indicates that many challenges persist, and companies can further enhance their supply chains in the digital era.

Over 300 executives and leaders surveyed acknowledge the benefits of digitizing supply chains and have made substantial commitments. The pressure to consistently meet customer demands has heightened scrutiny on supply chains across industries.

Lloyd’s explores the biggest threats to supply chains in transportation and logistics – an industry which underpins $89 bn of global trade and has a market value of $9.7 trillion.

The supply chain disruption experienced during the COVID-19 pandemic and more recently in relation to ongoing geopolitical conflict, has highlighted the fragility of supply chains to global impacts, and the importance of building resilience into risk management solutions.

The report, delivered in collaboration with WTW found that whilst over 90% of transport and logistics companies surveyed agree that insurance for supply chain risk is critical, 77% said a lack of access to supply chain insurance solutions, and a lack of data to understand these risks was among the greatest challenges to their businesses (see how War, Disruptions of Supply Chains & Climate Change Impacts on the Re/Insurance Industry).

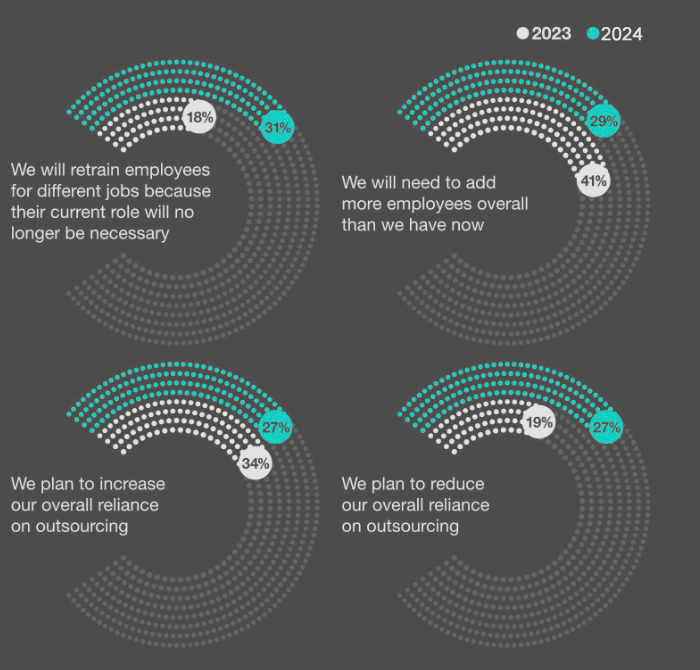

Working more with current supply chain workforce

Executives say their top priorities for the next 12-18 months are increasing efficiency and managing or reducing costs, with both named much more often than several other choices.

Even so, executives rank all other challenges much lower, including difficulty getting employees and teams to work differently (31% rank it as a top-three challenge) and difficulty attracting, developing and retaining the “digital native” talent needed to transform their supply chain (25%)

Those choices are notable as other responses suggest a tightening in workforces and that companies may be planning to work more with who they already have.

Potential impacts of main Supply Chain Risks

- Business, contingent and non-damage business interruption loss ratios could rise as less resilient supply chains lead to more business interruptions.

- The risk of D&O insurance claims increases if there is less investment in supply chain resilience, resulting in disruption to business operations. This could be considered as gross negligence or even intentional neglect by management.

- Morbidity and mortality rates can increase if deliveries of medical supplies are interrupted.

- Longer disruptions (eg, next pandemic, civil unrest in supplier countries, blockage of major trade routes, volcanic eruptions impacting air freight, earthquakes impacting major economic regions) can lead to economic and insurance market downturn.

Political Risks

Political instability is rising globally, affecting regions beyond high-profile conflicts like Ukraine, Gaza, the Red Sea, and Taiwan. The 2023 Fragile States Index shows increased fragility extending to affluent countries, suggesting key supply routes may become less secure.

The Fragile States Index, produced by The Fund for Peace, is a critical tool in highlighting not only the normal pressures that all states experience, but also in identifying when those pressures are pushing a state towards the brink of failure.

By highlighting pertinent issues in weak and failing states, The Fragile States Index—and the social science framework and software application upon which it is built—makes political risk assessment and early warning of conflict accessible to policy-makers and the public at large.

Nature-related Risks

Insurance against natural perils is on the rise annually. Increased occurrences of extreme weather, earthquakes, and volcanic eruptions pose threats to production facilities and transport routes.

Just three years ago, severe floods devastated several European countries, causing $54 bn in economic damages and leading to at least 243 deaths.

Natural disasters amplified by climate change continue to take a bitter toll on the global economy and caused more than $350 bn in economic losses, with insurance covering just over $100 bn.

Catastrophic events in 2024 already include severe convective storms in the U.S., major earthquakes striking Japan and Taiwan, exceptionally intense rainstorms in the Middle East, the largest wildfire ever in Texas’ northern Panhandle and severe flooding in southern Germany.

Technology Risks

Digitalization offers efficiency gains but also introduces systemic vulnerabilities. Constant updates to hardware, software, and procedures, along with trained staff, are essential to keep systems secure, according to NIST Updates.

A vulnerable spot in global commerce is the supply chain: It enables technology developers and vendors to create and deliver innovative products but can leave businesses, their finished wares, and ultimately their consumers open to cyberattacks.

A new update to the National Institute of Standards and Technology’s (NIST’s) foundational cybersecurity supply chain risk management (C-SCRM) guidance aims to help organizations protect themselves as they acquire and use technology products and services.

Modern products and services rely heavily on their supply chains, which link a global network of manufacturers, software developers, and service providers.

While essential for the global economy, these supply chains also expose companies and consumers to risks. Components and software for a single product often come from numerous sources worldwide.

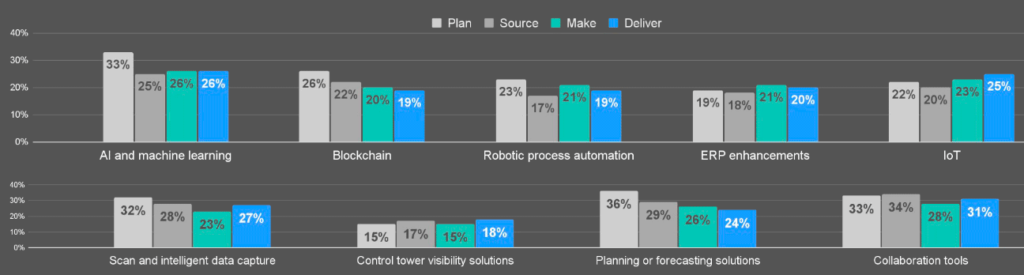

What techs are used in which parts of the supply chain?

Companies are investing in technology, but when it comes to specific technologies and solutions and different supply chain areas, a minority of respondents say they’re using technologies to automate and enhance execution of those areas.

For instance, a device might be designed in one country, assembled in another, and composed of parts from various regions, each with its own set of manufacturers.

This complexity increases the risk of malicious software and cyberattacks. Additionally, supply chain vulnerabilities can significantly impact a company’s financial performance.

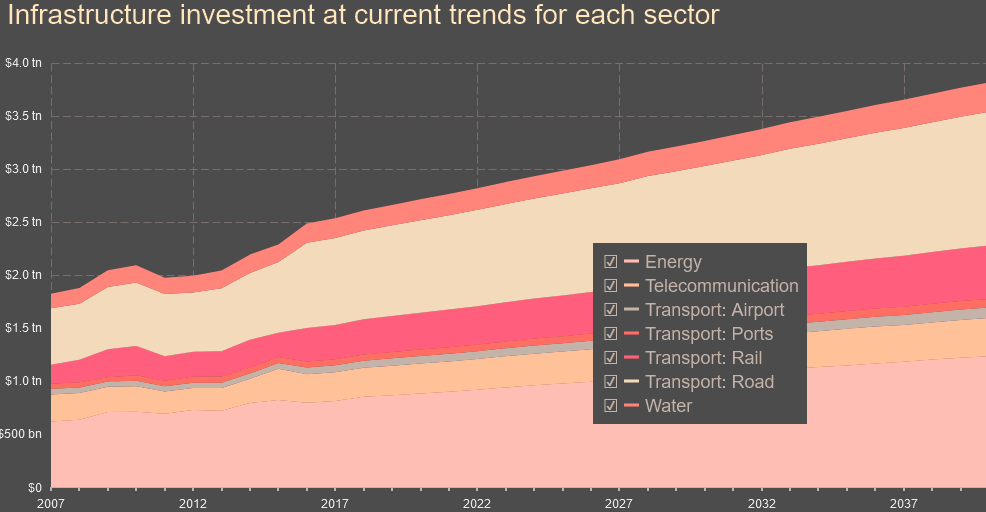

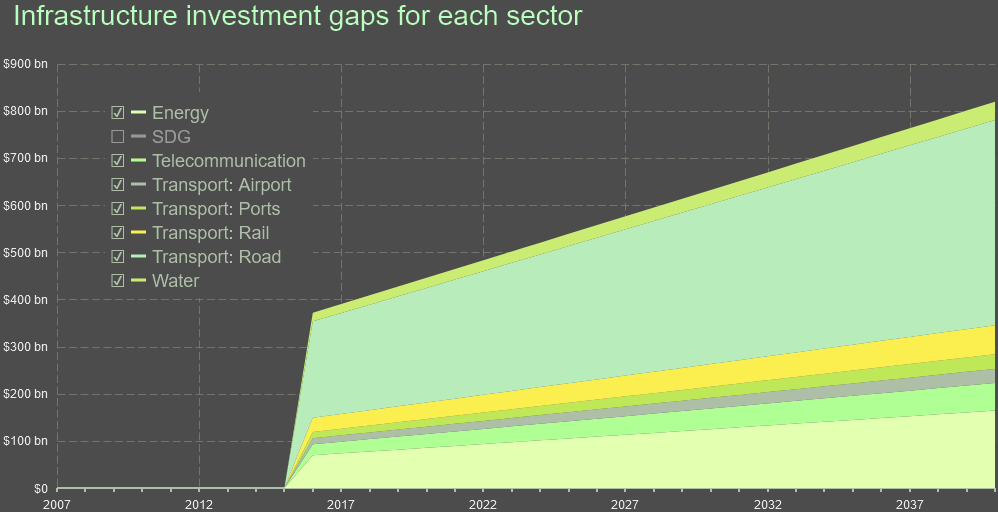

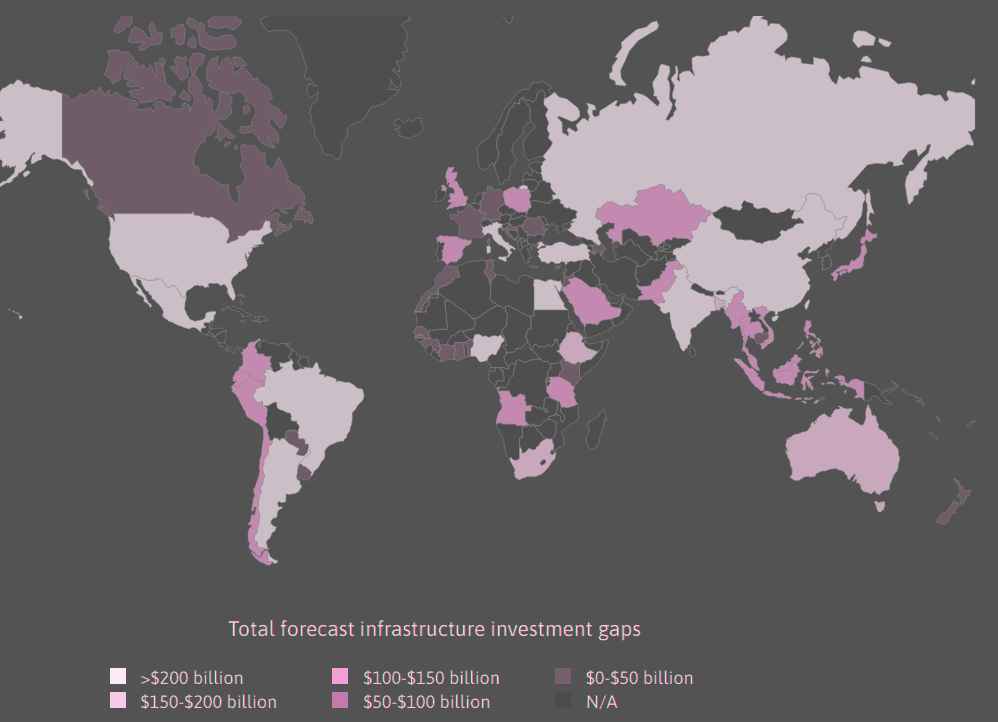

Infrastructure Risks

Supply chain operations rely heavily on infrastructure, including energy, water, power, and health systems, which are crucial during disasters or pandemics.

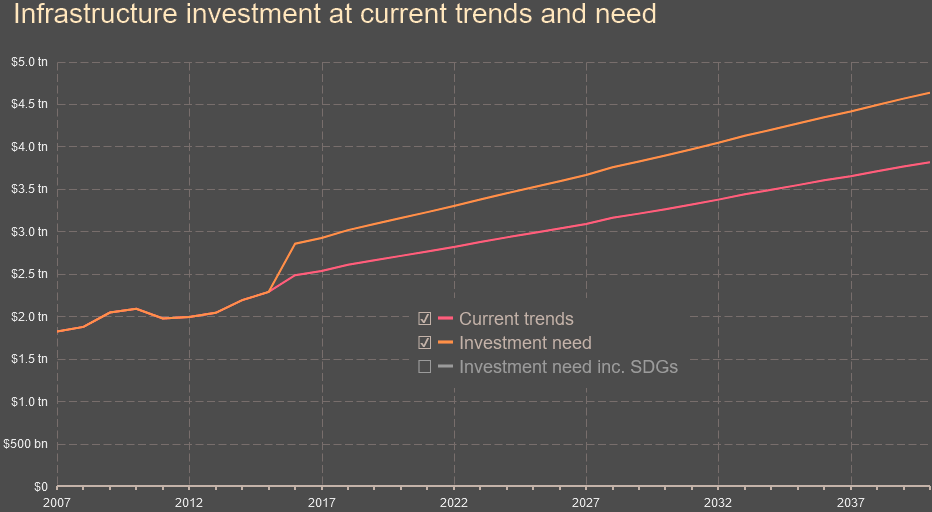

The G20 highlights a significant gap in Global Infrastructure Outlook between investment needs and actual spending, potentially weakening supply chain resilience.

Forecasting infrastructure investment needs and gaps

Economic Risks

Economic factors influence investments in supply chain infrastructure, and supply chain constraints affect the economic outlook. The Federal Bank of New York’s Global Supply Chain Pressure Index tracks these impacts.

Combined stressors on already strained supply chains can have significant business consequences.

Supply Chain Resilience

Despite the negative outlook on external risks and the lessons from the pandemic, supply chain resilience is not a top priority for many firms. A PWC survey reveals only one-third of executives prioritize investing in supply chain resilience, focusing instead on operational efficiency and cost reductions.

Safely and securely collate your data all in one place — whether for critical suppliers, one product or your entire supply chain.

By consolidating, cleaning and shaping your organisation’s data, we create a digital twin of your assets that you can use to experiment with risk and model business impact.

Supply chain disruptions are putting a drag on activity and trade at the global level. The most relevant elements are

- difficulties in the logistics and transportation sector

- semiconductor shortages

- pandemic-related restrictions on economic activity

- labour shortages.

Global shipping of merchandise goods has been severely disrupted owing to container misplacement and congestion on the back of not only the rapid recovery in the global economy, the rotation of consumption demand from services to goods, and the associated high import volumes, but also port closures because of localised and asynchronous outbreaks of COVID-19.[

Global Insurers’ Perspective

Insurers must consider this short-term focus when underwriting business interruption and contingent business interruption risks.

Accumulated risk drivers, such as a pandemic combined with drought, can significantly increase losses, disrupt supply chains, and reduce productivity due to health-related worker absences.

When companies invest significant dollars in different technologies to improve operations and supply chains, some trial and error is expected. But as PWC’s 2024 Digital trends in operations Survey shows, there’s still too much error, and that can be a hard pill for the C-suite and shareholders to swallow.

The survey of 600 operations and supply chain officers found a significant gap between what they expected new technology to deliver and the actual results.

For those who are outcomes obsessed, that harms efforts to create more value in the supply chain and operations overall. And that’s something few can afford in a world where 45% of CEOs believe their company won’t be viable in 10 years if it stays on its current path.

Many companies have invested in multiple technologies to digitize operations. Cloud (62%) and AI, including machine learning (55%), are clear leaders, while ERP enhancements (27%) and data ecosystems (33%) see the least investment.

Among different areas of operations, quality control uses technology the most, led by AI and operational visibility and analytics. Service and maintenance are seeing the least, and planning, sourcing, manufacturing and distribution are all at a similar level in between.

Even so, 69% of respondents selected at least one reason why their investments in operations technology haven’t fully delivered the expected results. More than half (59%) cited at least two reasons, and 37% cited at least three.

While the share of respondents who say their companies didn’t fully realize the expected results is down from previous surveys, the fact that more than two-thirds still claim shortcomings from tech investments indicates a persistent problem.

FAQ

After COVID-19, companies initially focused on strengthening supply chains to handle disruptions. However, recent PwC surveys show that cost reduction has regained priority as businesses aim to manage expenses, even if it lowers resilience to disruptions.

The pandemic underscored the fragility of global supply chains, leading to widespread interruptions. It highlighted the need for resilience against disruptions, yet investment in this area has decreased, increasing the risk of future losses.

Current threats include climate change, political instability, and digital risks. Events like extreme weather, geopolitical conflicts, and cyber threats expose supply chains to potential breakdowns and significant financial losses.

Digital investments in supply chains improve cost efficiency, streamline processes, and mitigate risks. Technology can also help address environmental and social governance (ESG) concerns, though challenges in implementation persist.

Insurance for supply chain risk is crucial, yet over 77% of companies struggle with access to these solutions and lack sufficient data for risk management. Effective insurance helps protect against major losses from disruptions.

Rising political instability increases the likelihood of supply chain disruptions, especially in regions prone to conflict. The Fragile States Index highlights the vulnerabilities, showing that even affluent nations face growing instability.

Many executives prioritize operational efficiency and cost reduction over resilience. A PwC survey reveals that only a third of companies see resilience as a top investment area, despite the ongoing disruptions in global trade and logistics.

………………

AUTHORS: Patrick Raaflaub – Chief Risk Officer at Swiss Re, Rainer Egloff – Senior Risk Manager at Swiss Re Institute