Overview

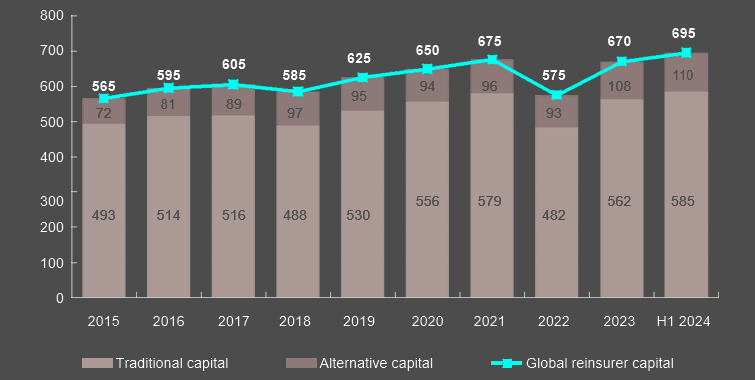

In 2024, global reinsurer capital, including both alternative and traditional sources, has reached peak levels. Reinsurer capital stood at $695 bn as of mid-2024, marking a $25 bn increase from the previous year. This significant rise reflects strong underwriting results, improved investment yields, and growing interest from investors in insurance-linked securities (ILS).

Aon estimates that global reinsurer capital totaled $695 bn at June 30, 2024, up $25 bn relative to the end of 2023. The increase was principally driven by retained earnings, recovering asset values and new inflows to the catastrophe bond market.

With capital at these peak levels, reinsurers are better positioned to meet growing demand for coverage. However, competition is increasing, and pricing conditions are expected to ease in 2025 renewals, especially if there are no major catastrophe events in the remaining months of 2024.

Global Reinsurer Capital

Reinsurance market’s capital strength

The reinsurance market’s capital strength in 2024 reflects both the robust performance of traditional reinsurers and the expanding role of alternative capital in addressing global risk needs.

- Traditional Capital: Traditional capital, derived from equity, retained earnings, and debt, remains the foundation of reinsurance capacity. Recent strong financial results, especially in property catastrophe lines, have boosted the ability of reinsurers to expand capacity. This increase is particularly notable given the above-average natural catastrophe losses during the first half of 2024.

- Alternative Capital: Alternative capital, which includes instruments such as catastrophe bonds, collateralized reinsurance, and sidecars, continues to gain traction. Investors are drawn to the sector by its non-correlated returns compared to traditional asset classes. The growing interest in ILS has helped increase the overall capital pool, contributing to more competition and flexibility in pricing.

Q2 Reinsurance Market Dynamics

Traditional capital: Equity at record levels and building

Aon estimates that equity reported by global reinsurers totaled $585 bn at June 30, 2024, up $23 bn relative to the end of 2023. Continued strong earnings in the second quarter were offset by the payment of annual dividends.

The strong returns achieved over the last 18 months as a result of the market ‘reset’ in 2023 continue to attract investor interest, but established reinsurers and the ILS market are still being favored over the formation of start-up companies.

Most major reinsurers display improved regulatory and rating agency capital adequacy metrics in 2024, taking deployable capacity to new peaks. The market’s willingness to deploy this capacity over the next few years to address currently unmet client need will define the sector’s long-term relevance.

Reinsurance Sector Performance

Global Reinsurance Premiums / Revenues

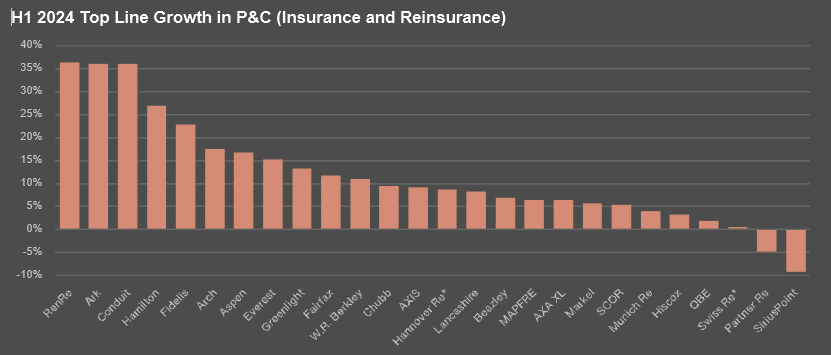

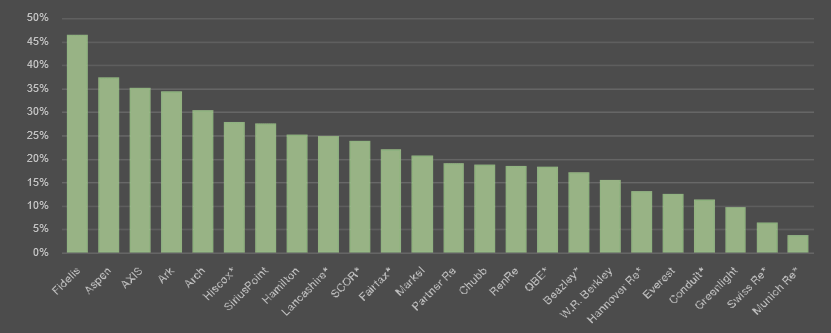

All but two of 26 companies tracked reported top line growth in property and casualty insurance and reinsurance business in the first half of 2024. The average increase was 11.8%.

Top Line Growth in P&C Re/Insurance

Inflationary factors continue to underpin both pricing and demand for coverage.

In commercial lines insurance, property reinsurance rate increases are now decelerating, while casualty rates are picking-up in response to reserve challenges. In personal lines, higher earned pricing is benefiting the auto sector, while natural catastrophe activity continues to challenge homeowners’ results.

The companies surveyed are still seeing growth opportunities on the direct side, particularly in the U.S. excess and surplus lines market.

Facultative business is also viewed as attractive. Pricing is viewed as remaining ahead of loss cost trends in most areas, although rate reductions continued in cyber, D&O liability and workers’ compensation business.

On the treaty side, rates have been broadly stable at relatively high levels through the 2024 renewals, with pricing past the peak for remote property catastrophe layers, despite increased demand.

Most of the companies surveyed are favoring short-tail property and specialty lines over casualty business, on the basis that ultimate loss costs can be established with greater certainty.

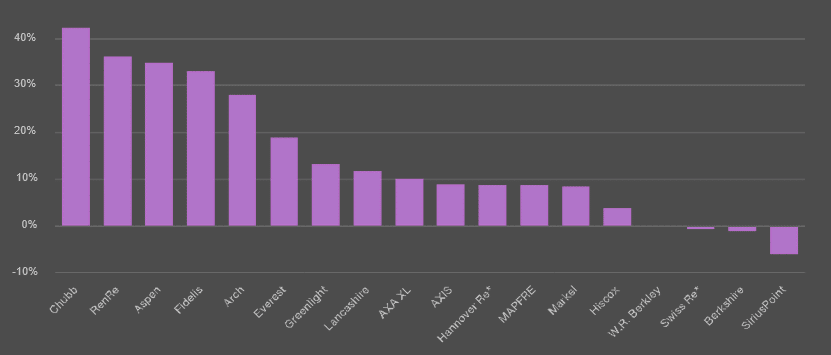

Top Line Growth in P&C Reinsurance

On a whole account basis, outwards cession ratios were relatively stable year-on-year. The average result across the 24 companies surveyed ticked up by 0.4%age points to 21.8%.

Increasing use of third-party capital management platforms is being observed, particularly on the reinsurance side, as companies look to manage volatility and bring down their overall costs of capital.

P&C Cession Ratios Re/Insurance

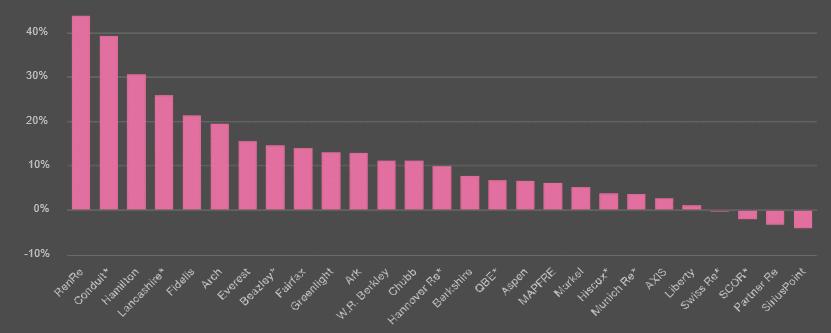

Reported underwriting results are being supported by continued net account growth in most cases. The average increase was 11.7% across the 27 companies surveyed.

P&C Net Account Growth Re/Insurance

Reinsurance Underwriting

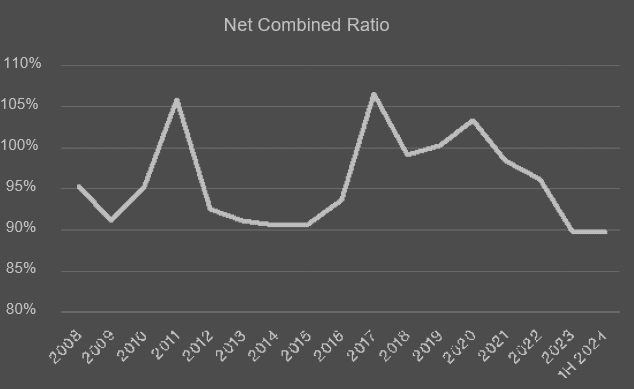

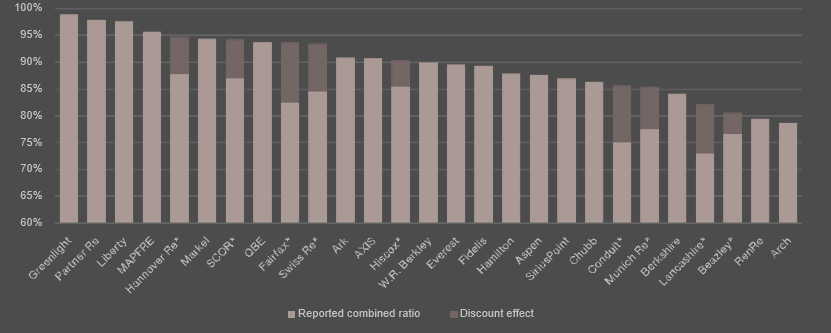

The reported combined ratios across 27 companies surveyed are shown in Exhibit 7. The average ticked up by 0.3%age points to 89.7% year-on-year, still a very positive outcome, demonstrating the continuing strong margins available in the business.

P&C Combined Ratios Re/Insurance

In stark contrast to the 2017-2022 period, major losses reported by reinsurers have generally been well within budget over the last 18 months.

Higher retentions have provided protection against record secondary peril losses, while primary peril losses have remained at very manageable levels.

The average major loss ratio across 22 companies surveyed was 5.2% in the first half of 2024. Reporting thresholds vary across the industry and therefore these ratios are not directly comparable.

Casualty loss cost trends were the leading topic for equity analysts (and investors) on recent earnings calls. Pockets of adverse reserve development in lines most exposed to social inflation, such as general liability and commercial auto, have been widely acknowledged, but in most cases favorable development in other classes continues to mask these deficiencies.

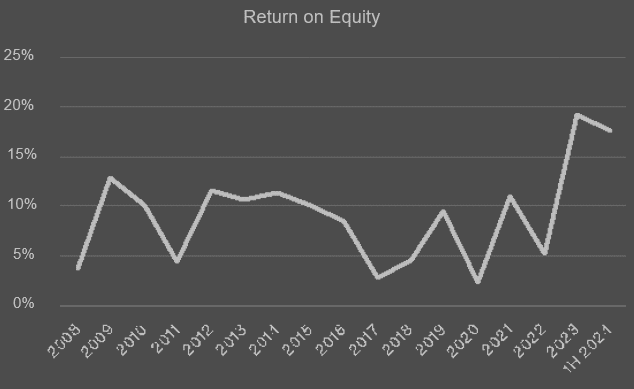

Return on Equity

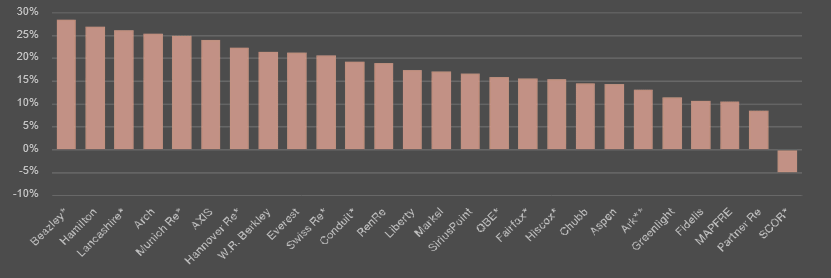

In most cases, business growth, moderate major losses and favorable capital markets combined to generate strong returns on equity in the first half of 2024. Across the 26 companies, the average outcome was 17.6%, which was in-line with the prior year period and around double the estimated average cost of equity.

Annualized Return on Common Equity

A significant amount of new capital has been generated via strong earnings over the last 18 months. This has allowed most reinsurers to reward their investors with higher dividends and/or share buybacks and, at the same time, to consider deploying additional capacity into the marketplace.

………………..

AUTHORS: Mike Van Slooten – Head of Business Intelligence at Aon, Richard Pennay – CEO of Insurance-Linked Securities at Aon