The life insurance industry’s response to the drivers discussed above has been highly varied. Some life insurers have been conservative while others have embraced innovation.

Life insurance is still dominated by traditional businesses that facilitate the accumulation or de-cumulation of savings through products such as annuities and endowments, which accounted for 81% of global life insurance premiums.

However, this share is down from 86% in 2008 when the Global Financial Crisis hit. Primarily as a result of low interest rates and a higher awareness of biometric risks, protection products have recently gained in market share.

Such products include term insurance, disability and critical illness insurance, all of which generally have a shorter duration than savings-type products and hence less exposure to changing interest rates.

How have life insurers reacted so far?

According to The Geneva Association Report Financial Wellbeing, in response to the changing macro-economic environment and higher solvency requirements for yield guarantees, life insurers have also steered their portfolios towards unit-linked or asset-management-type businesses, where the investment risk is largely with the policyholder.

This Report provides global insight into how life insurers perceive their role in financial wellbeing and the way in which they have applied the concept.

While increased risk sharing with customers may be consistent with the industry’s purpose of offering affordable coverage to as many people as possible, the relevance of this trend for retirement security varies across countries and depends on the institutional peculiarities of retirement systems.

In the U.S. the value of annuities and other savings-oriented life insurance obligations is less than 10% of defined-(i.e. guaranteed) benefit pension obligations.

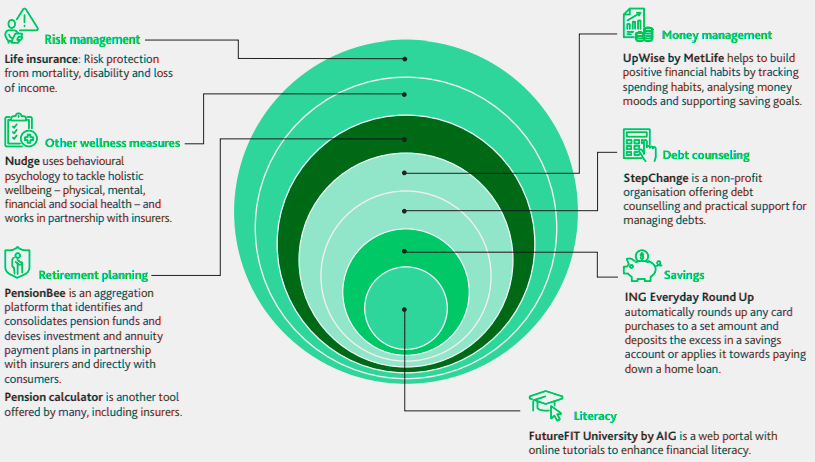

Financial wellbeing products serve a package of needs that often go beyond the traditional offerings of life insurers.

At the same time, a growing number of insurers have embraced innovations and developed products that support a broader spectrum of customer financial needs. For the purposes of this report, financial wellbeing products are defined as serving a package of needs thatoften go beyond the traditional offerings of life insurers.

These needs can be grouped into three categories:

- At the very core of financial wellbeing lies financial literacy.

- From there, the needs progress towards everyday financial demands such as spending, borrowing andsaving.

- Finally, they touch upon needs related to long-term financial security, including retirement planning,steps to ensure general wellness and risk protection from unforeseen life events.

Many life insurers have started to expand their role to address all parts of this spectrum. But for the vast majority of life insurers, the focus is concentrated on areas denoted in dark to moderately dark shades, such as retirement planning, savings and financial literacy, among others.

Financial wellbeing: Customer needs

Stress about money and finances may have a significant impact on Americans’ lives. Nearly 72% of adults report feeling stressed about money at least some of the time and nearly 25% say they experience extreme stress about money.

The American Psychological Association (APA) recognizes financial stress as the leading cause of unhealthy behaviors like smoking, weight gain, and alcohol and drug abuse. Other behaviors linked to financial stress are gambling and overextending credit balances. Each time an individual turns to these temporary stress relievers, the APA concludes that the stress returns and often at even greater intensity.

What is financial wellbeing?

Financial wellbeing is different to financial wealth. While wealth might be about bank balances and net worth, wellbeing is about how the way you manage money affects your life on the whole.

It’s about being able to meet your financial obligations, be financially prepared for an unexpected event, able to save for future goals including retirement and having the financial freedom to make choices that allow you to enjoy life – now, in the future and under adverse circumstances.

Life-Insurance-Digital-Financial-Wellness Examples in Focus

Upwise

Upwise is a digital financial wellness app by MetLife that tracks financial concerns orstressors like monthly budgeting, debt or long-term savings and helps users prioritise financial goals. It suggests simple actions to develop good financial habits and make customers feel more optimistic about what their money can do for them.

The more consumers take advantage of the app’s features, the better Upwise understands their individual needs and delivers a personalised experience and recommendations toward financial wellness.

A key innovation of the app is the tracking of monetary moods: only after understanding customers’ emotional relationship to their money does Upwise dive into financial goals.

Vitality Money

Vitality Money, offered by Discovery, is a financial wellbeing plan with a focus onfive main financial behaviours: having enough savings, managing debt, accessing insurance, retirement planning and investment.

Through personalisation using real-time data, nudge techniques and incentives, the product identifies areas of improvement to unlock benefits. It incorporates dynamic adjustment of borrowing and saving rates, discounts on healthy lifestyle choices and Vitality Active Rewards for meeting a set of weekly goals.

Progress towards retirement saving is calculated by comparing monthly contributions, accumulated savings and income to a target in line with the age of the user. Products include annuities, provident funds and pension funds from Discovery Invest, including the Discovery Retirement Optimiser – a retirement savings investment that allows customers to convert life cover into extra income in retirement.

SNACK

SNACK is a Singapore-based digital micro-insurance product targeting Millennials thatbuilds insurance coverage in bite sizes through daily activities. Whenever customers shop at SNACK brands or perform a lifestyle activity, a micro-insurance policy is issued to them for term life, income or accident coverage through an app.

Coverage grows with each activity performed, with daily premiums as low as SGD 0.30. Clients have the flexibility to adjust premiums, add or remove lifestyle activities and withdraw their entire portfolio anytime without any fees or penalties.

With an easy-to-use, intuitive model and low entrance barriers, SNACK deepens protection for the young who may struggle with cash flow by integrating insurance with everyday activities.

Insights from 25 life insurers

The perspectives of 25 large life insurers (with combined annual gross premiums for the life segment amounting to over USD 550 billion) on the evolving concept of financial wellbeing.

- Insurers’ interpretations of and perceptions about financial wellbeing.

- How the concept of financial wellbeing is being applied in practice.

- Practitioner insights into the opportunities and challenges involved in cementing insurers’ role in financial wellbeing.

Defining financial wellbeing from an insurance perspective

Respondents were asked to share their understanding of the evolving concept of financial wellbeing from the perspective of life insurance and based on the needs in the countries/regions where they operate.

The first and most common theme that emerges is an acknowledgement that financial wellbeing is a dynamic phenomenon encompassing a range of needs over the life course. This is broadly in line with the academic definition cited at the beginning of this report.

However, despite this clear acknowledgement, the second most common theme is a distinct emphasis on the role of ‘retirement’ preparedness alone in promoting financialwellbeing, something that is strongly associated with the traditional role of life insurers.

Issues such as financial literacy or financial anxiety feature less explicitly or frequently, and only a few respondents allude to matters concerning day-to-day financial management.

What matters to life insurers in promoting financial wellbeing?

One could argue that the relative importance of insurance industry priorities suggested by the bolder words hardly comes as a surprise. But what is significant is that it reveals a large gap between what life insurers acknowledge as financial wellbeing needs and what they see as solutions.

Perhaps this gap also indicates that the life insurance industry as a whole has yet to meaningfully adjust to the new market realities and crystallise a new vision of its position in the financial wellbeing landscape.

The majority of respondents identify demographic shifts as the main driver of financial wellbeing, whereas technological shifts are seen as least important. This result could be partly explained by the composition of the sample, which has a higher representation of rapidly ageing markets.

Whatever the explanation, respondents view technology as more of an ‘enabler’ to develop better tools, products, marketing and distribution, rather than as a driver in and of itself. At the same time, some feel that the potential of digital technology in areas such as gamification of savings products and a more in-depth role for real time data-led innovations is still unrealised.

Life Insurance and Financial wellbeing in practice

Respondents identify insurers followed by banks as the most active players in the financial wellbeing space. Government comes third. Professional advisory firms, non-governmental organisations (NGOs) and independent digital platforms are seen as moderate or the least active players, perhaps not fully taking into account the recent growth in the age tech sector.

The Geneva Association’s survey reveals a large gap between what life insurers acknowledge as financial wellbeing needs and what they see as solutions.

Improving risk exposure through preventive measures is insurers’ least cited motivating factor for offering financial wellbeing products. Assisting with retirement is the most cited goal.

Almost all respondents’ companies offer products and services to support financial wellbeing that go beyond traditional risk and savings solutions, with the main motivating factors being improving customer appeal, numbers and retention. However, one significant finding is that improving risk exposure through preventive measures is the least cited motivating factor for offering these products.

In the retirement space, innovations include:

- modular coverage for specific risks to avoid customers having to buy blanket life policies, with these products often targeting younger cohorts and gig workers;

- offers that combine lower guarantees with increased upside potential through investment returns;

- incentivising new ways of de-cumulating and deterring early drawdowns;

- behavioural-science-led nudges to encourage savings; mid-life wealth checks;

- payback and discounts for adopting healthy lifestyles that promote active ageing;

- ensuring ease of passing benefits to successors; and collaborating with social programmes and micro-insurers to cover vulnerable workers, among others.

Technology in this space is viewed as a means to develop creative interfaces and offer new online tools.

These include tools for comparing retirement scenarios and accessing financial resources, as well as app-based programmes to monitor and manage retirement savings or understand financial stress points to formulate better goals.

Promoting financial literacy is integral to most products, though it is usually tailored to the context of retirement planning and protection, as indicated before.

Only a handful of insurers target financial wellbeing solutions to all age groups. A minority addresses financial literacy among the young – even though people’s early years are the most formative years in their lives and significantly influence their later choices and life chances.

The majority of life insurance solutions target working-age adults, with slightly more emphasis on those aged 41–64. Focus on older adults aged 65 and over is moderate.

These findings pose two major concerns.

Firstly, insurers are missing an important opportunity to promote financial literacy and preparedness among the young and cement their role in the early years of people’s (working) lives, an oversight that may reflect an understanding of financial literacy that is focused on retirement and protection goals rather than a more holistic set of financial needs and products.

Secondly, while a number of insurers have identified the opportunities accorded by the longevity economy, attempts to harness the ‘grey dollar’ and recapture the elderly population with innovative solutions that meet needs in older age remain modest.

In terms of distribution channels, the use of digital channels by insurers appears to taper off at older ages, with more emphasis on direct contact with banks, agents and advisors for customers aged 65 and over.

This bias towards the young and the middle-aged when it comes to digitalisation seems to confirm the insufficient focus of the life insurance industry on the longevity economy and an assumption about older consumer preferences which may or may not prove to be correct.

In terms of the effect financial wellbeing products have had on key consumer metrics such as numbers, retention, behaviour, outcomes and experience, the overall survey feedback is measured, with no single area standing out.

A ‘fair’ effect is observed in areas such as consumer numbers, retention and experience as a result of rolling out financial wellbeing products and services. This is followed by ‘some’ effect in areas such as consumer engagement and behaviour.

The more positive effects in the areas of consumer numbers, retention and experience can be explained by a number of factors.

Cross-selling of products may have enabled insurers to capture consumers in different ways – for example, by combining non-financial with financial wellbeing products and services and rewarding better lifestyle through lowered premiums.

Equally, investment-linked products may have had a greater appeal for risk-taking and yield-minded consumers. Digital interfaces may also have helped to boost consumer awareness, access and experience. Nonetheless, there remain notable gaps with regards to increasing the number and quality of touchpoints with customers.

For instance, while there is a strong focus on consumer experience and access, the use of data generated by new technologies does not appear to

be widespread, and this may limit the ability of insurers to sufficiently understand and guide the consumer in real time or to make products simpler and easier to follow.

Reflection on the future: opportunities and challenges

There is almost a unanimous view that insurers are highly capable of fostering financial wellbeing and that more can be done to improve on the status quo despite the macro-economic head winds. As the onus of retirement and long-term savings shifts from the state and employers to individuals, individuals often do not have the capacity to assume this responsibility. This is where insurers are thought to have an important role to play in partnership with other stakeholders.

Rising to the challenge will require major innovations on the part of insurers, who may need to shift their focus to health and general wellbeing, as well as making sustainable investments and offering new incentives to improve the consumer appeal of their products and services.

Respondent feedback on opportunities can be categorised into three areas.

- Firstly, there is the opportunity to meet the needs of consumers whose work and retirement experiences will look very different from the status quo. Doing so will require better customisation of products, as well as creating touchpoints that speak to personal needs, circumstances and financial aspirations.

- Secondly, considering the low-level prioritisation of insurance by many consumers, there is an opportunity to redefine retirement savings within the broader concept of general savings. In order to accomplish this, insurers will need to adopt a one-stop-shop approach to savings needs, with in-house and third-party capabilities to manage wealth and financial wellbeing throughout the life course.

- Finally, opportunities accorded by the longevity economy could be leveraged through better integration of health and elderly care. With fundamental changes in the population pyramid, where there are now more old than young, many Asia-based insurers in particular feel health and social care will become major areas of consumption. This warrants devoting more resources to developing solutions that help the aged live better by offering enhanced protection while also unlocking their purchasing power.

The perceived challenges can also be categorised into three areas.

- Firstly, the static, squeezed or insecure income of the working-age population increasingly challenges financial wellbeing in high, medium and low-income countries alike.

- Secondly, within companies, there remains a deep-seated entrenchment of traditional business models, and some may not have grasped the level of threats from (digital) competitors. For instance, the vast physical distribution channels of many insurers are still overwhelmingly focused on one-off sales of policies rather than being adapted to offer and manage more holistic financial wellbeing propositions as outlined above.

- Finally, politics and the regulatory environment are unsettled. For instance, tax incentives change with every political cycle, doing little to instil long-term savings habits or stimulate insurance purchase. Also the lack of openness in the political discourse around longevity needs and the resultant pension gap adds to the complexity of insurers’ operating environment.

Financial literacy is at the very heart of financial wellbeing. Yet people continue to underestimate their future needs given increased life spans, as well as the importance of insurance in enhancing their financial wellbeing.

Insurers have an opportunity to address this gap in the immediate term with relatively modest investments that focus especially on early age.

Broader wellbeing issues, including those that are health-related, may also have a knock-on effect on productivity, wealth accumulation, how and when people retire and their needs in old age.

…………………

AUTHORS: Adrita Bhattacharya-Craven – Director Health & Ageing The Geneva Association, Richard Jackson – President Global Aging Institute, Kai-Uwe Schanz – Deputy Managing Director and Head of Research & Foresight The Geneva Association