Overview

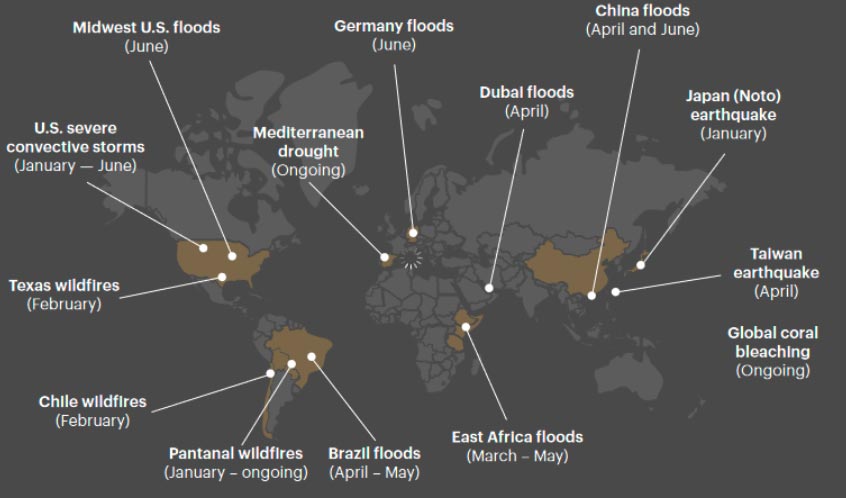

Natural disasters amplified by climate change continue to take a bitter toll on the global economy and caused more than $350 bn in economic losses, with insurance covering just over $100 bn. Catastrophic events in 2024 already include severe convective storms in the U.S., major earthquakes striking Japan and Taiwan, exceptionally intense rainstorms in the Middle East, the largest wildfire ever in Texas’ northern Panhandle and severe flooding in southern Germany.

According to WTW’s Natural Catastrophe Review, more than ever, it’s critical to price the cost of natural catastrophe risks accurately and prepare accordingly. But all too often, the naive use of risk models leads people to miscalculate exposure to extreme catastrophic events.

Just three years ago, severe floods devastated several European countries, causing $54 bn in economic damages and leading to at least 243 deaths.

For many businesses, the floods far exceeded their risk scenario planning considerations, with financial impacts much worse than expected.

After any major disaster, it’s common for people to complain that their models underestimated the true costs. But it’s worth remembering we put models to work on a very difficult task: to predict the physical and financial impacts of natural hazards on a world constantly being reshaped by climate change, exposure growth and inflation.

Global natural peril review

Despite summer not being in full swing, 2024 has already been a notably active year for severe convective storms in the United States.

With 1,264 tornado reports, this year has the second-highest number of tornadoes in the past 15 years.

Additionally, there have been 4,108 hailstorms, making it the fifth most active year for hail, and 8,978 damaging windstorms, the second most on record. However, 2024 still trails behind 2011, which remains the worst year for these perils across the U.S.

The total storm counts for the entire country are not a perfect measure of economic or insured losses. In both 2011 and 2023, high numbers of wind and hailstorms resulted in the worst years for direct damages in recent memory.

2020, despite having typical numbers of tornadoes and windstorms and a lower-than-average number of hailstorms, still experienced high economic and insured losses.

Since most damaging storms occur in summer, the early start to this year’s severe weather season suggests another potentially costly year with high damages from convective storms.

Prominent natural catastrophes

Major Storms in 2024

This year’s most severe storms have involved tornado “outbreaks,” where multiple tornadoes originate from the same large-scale weather pattern over one or more days. From April 26 to 28, severe weather in the Southern and High Plains generated over 140 tornadoes, including a violent EF4 tornado that destroyed a Dollar Tree distribution warehouse in Marietta, Oklahoma.

Another large outbreak from May 6 to 10 resulted in more than 160 tornadoes hitting Oklahoma, Kansas, Tennessee, Alabama, Georgia, and Michigan. This system was so destructive that several National Weather Service offices issued tornado “emergencies,” indicating a severe threat to human life.

Finally, from May 19 to 27, the Midwest experienced an extended period of tornadic activity, culminating in a large, violent EF4 tornado that devastated Greenfield, Iowa, killing at least five people.

Lessons from Noto (Japan) and Hualien (Taiwan) Earthquakes

In early 2024, major earthquakes hit Japan and Taiwan. WTW’s engineering experts analyzed building failures, emphasizing the need for seismic risk assessments, retrofitting, and improved construction codes.

Overview of the 2024 Earthquakes

In the first half of 2024, Japan (Mw7.5) and Taiwan (Mw7.4) experienced significant earthquakes. Enhanced resilience and preparedness reduced casualties and damage compared to previous events.

However, building and infrastructure failures still occurred. In Japan, liquefaction-prone areas saw most failures, while in Taiwan, soft-story collapses were prevalent. These issues underscore the need for ongoing seismic risk assessments, retrofitting vulnerable buildings, and updating construction codes.

Mw7.5 Noto Earthquake, Japan

On New Year’s Day 2024, a Mw7.5 earthquake struck Japan’s Noto Peninsula at a depth of 10 km, causing severe shaking, liquefaction, and landslides. The shallow epicenter produced peak ground accelerations (PGAs) of up to 1.2g, comparable to those during the 2011 Tohoku earthquake.

Over 102,000 structures in Ishikawa Prefecture were damaged, including the complete or partial collapse of 23,700 buildings.

The earthquake resulted in 245 deaths and over 1,300 injuries, primarily from collapsed buildings. Economic losses were estimated at up to 2.6 trillion yen ($17.6 bn), while insured losses were estimated at up to 870 bn yen ($5.5 bn).

Despite frequent seismic activity, Japan’s strict building codes, continuously updated after major seismic events, reduce earthquake casualties. These codes, established after the 1923 Yokohama earthquake, mandate stringent seismic design and retrofitting.

The 1995 Kobe and 2011 Tohoku earthquakes prompted further improvements, enhancing seismic resilience. In response to the 1995 Kobe earthquake, Japan implemented an early warning system and conducts regular earthquake drills to improve public preparedness and response.

Modern Japanese buildings, utilizing reinforced concrete, steel, seismic dampers, and base isolation, generally withstood the earthquake well, showing minimal structural damage.

Collapses mainly occurred in older structures, those with irregular designs, or those with inadequate seismic detailing, particularly in liquefaction zones. Some newly constructed wooden buildings also failed, indicating a need for further revisions to the Building Standard Law.

Hualien Earthquake, Taiwan

On April 3, 2024, a powerful Mw7.4 earthquake struck eastern Taiwan, located 18 km southwest of Hualien at a depth of 34.8 km. This relatively shallow earthquake caused intense shaking, with a peak ground acceleration of 0.55 g near the epicenter.

The Land Management Agency reported 848 damaged structures, including 42 marked as “code red.”

The disaster resulted in 18 deaths and over 1,100 injuries. Economic losses were estimated at $28 bn, with insured losses likely between $0.5 bn and $1 bn.

This was Taiwan’s strongest earthquake in nearly 25 years, following the 1999 Mw7.7 Chi-Chi event in central Taiwan, which caused severe damage or collapse to over 100,000 buildings and resulted in over 2,400 fatalities and 11,000 injuries.

The reduction in collapsed buildings and fatalities since the 1999 Chi-Chi event highlights improvements in seismic resilience over the past three decades.

After the 1999 earthquake, Taiwan introduced stringent construction standards and curbed poor construction practices. Recognizing that building codes alone were insufficient, Taiwan also implemented programs to assess and retrofit structures.

$4 bn was allocated from 2009 to 2022 to upgrade the seismic capacity of 10,000 schools.

Additionally, private buildings underwent screenings and mandatory seismic assessments, with the government providing retrofit guidance and subsidies for high-risk buildings.

Despite these efforts, some buildings remain at high risk of seismic damage. The Hualien earthquake highlighted the vulnerability of soft-story buildings—multi-story structures with open spaces lacking structural walls, common in buildings with carports or commercial spaces on the first floor.

Soft-story buildings are an issue not only in Taiwan but also in other seismically active regions such as California.

For example, the 1989 Loma Prieta earthquake in Northern California caused many failures of soft-story multi-residential buildings with carports on the ground floor.

This common vulnerability across continents highlights the importance of a comprehensive risk evaluation performed by teams of experienced engineers, who not only can assess the risk but also can provide viable retrofit strategies for a vast array of structures.

Flood risks and climate challenges impacts for aviation

The recent floods in Dubai caused significant challenges for local airlines and airports. Well-calibrated insurance and risk management strategies, including the use of parametric insurance, can improve resilience.

Floods have always been part of life on earth, but recent flash flooding events in eastern Australia, Brazil, Dubai and Texas have been significant, sudden, and caused major disruption for airports and airlines.

Changes in the world’s climate are making these previously unusual events into something we all need to be prepared for. Insurance and risk management have a positive role to play in supporting aviation organizations as they strive for resilience.

Dubai’s deluge in April was particularly eye-catching because it occurred in a region that is famously arid. The United Arab Emirates has minimal annual rainfall, typically 78 mm per year (compared with the U.K.’s 1,220 mm), and extreme rainfall events are rare in the region.

When they do occur, they are often intense, and what is concerning is that records related to the intensity of rainfall in the region that were broken in 2022 have been broken again less than two years later.

An estimated 1,244 flights were canceled over the initial two days of the incident, which likely resulted in subsequent delays and cancellations throughout global networks.

Business interruption insurance typically requires physical damage for a payout, and since there was little to no physical damage to aircraft, many incurred costs are unlikely to be recoverable from insurers.

Adapting to climate risks with parametric insurance

Parametric insurance or index-based programs can support aviation organizations facing rain-related cancellations in arid regions and other diverse, changing landscapes.

These programs address income loss or increased costs from adverse weather using robust data to tailor coverage based on geography, risk exposure, risk appetite and budget.

They cover various weather events, including tropical cyclones, floods (river, coastal and flash flooding), wildfires, drought, hail and temperature extremes. Claims are triggered if a reference index moves above (or below) an agreed threshold, with payouts calculated on a pre-agreed scale.

The benefits of parametric insurance for aviation organizations are significant. It provides protection against economic loss without requiring direct damage to insured assets, thereby covering non-damage business interruption.

Payouts can be scaled and tailored to provide coverage for specific scenarios and event intensities. The clearly defined parameters eliminate the need for onsite loss adjustment, allowing claims to be paid within days or weeks rather than months.

With unrestricted use of claim proceeds, organizations can use payments as needed, whether to replace damaged assets; supplement revenue; cover additional expenditures; invest in risk management; service debt; or provide financial support for customers, employees or communities.

The recent floods in Dubai and further afield highlight the importance of strong relationships with insurance partners to ensure that risk management and financing meet the evolving needs of aviation organizations.

Accurate risk assessment models that incorporate changing climate conditions and urban development patterns are crucial. While historical data are useful, preparing for future changes, and being ready for change, is essential for building resilience.

Texas Panhandle wildfires

In February 2024, wildfires in the Texas Panhandle burned 510,000 hectares and destroyed over 500 structures. Downed power lines ignited the fires, highlighting risks from aging infrastructure, poor land management, declining population, and climate change.

The Smokehouse Creek Fire, the largest wildfire on record in Texas and the second largest in the U.S., burned 426,600 hectares.

Ignited on February 26, 2024, in Hutchinson County, this wildfire quickly spread across Hemphill and Roberts counties, including the town of Canadian. It cut power to 11,000 people and caused the deaths of three people and 15,000 cattle.

Insured losses are expected to exceed $350 mn, while the Investigative Committee on the Panhandle Wildfires estimates total economic loss to the Panhandle may ultimately exceed $1 bn.

The Texas Panhandle’s steady population decline due to cultural and economic shifts has made it harder for authorities to manage and respond to recent wildfires. According to the Texas Emergency Management Council, fewer residents in the region mean fewer volunteer firefighters and less local government tax revenue to support their volunteer fire departments.

Recent fires add to insurance protection gap challenges

Texas homeowners’ insurance premiums are significantly higher than the national average and have been rising due to increased weather-related claims and climate change concerns.

Governor Greg Abbott noted that many homes in rural Panhandle counties affected by recent fires had no insurance.

Likewise, most fencing and cattle losses were uninsured unless landowners had special endorsements, with preliminary estimates indicating $123 mn in agriculture and related economic losses from the Smokehouse Creek Fire.

With climate change expected to increase the frequency and severity of extreme weather events in Texas, the risk to uninsured homeowners will grow.

This highlights the urgent need to improve insurance affordability and close the protection gap, particularly for vulnerable rural and lower-income populations.

The Investigative Committee on the Panhandle wildfires recommended that the legislature evaluate ways to limit insurance premium increases for property and business owners affected by the fires and to make insurance coverage for fencing and cattle more widely available and affordable.

El Niño and climate change fuel Brazil floods

Catastrophic flooding in Brazil during April and May highlighted the combined impact of El Niño and climate change. The extreme rainfall, now twice as likely due to global warming, caused severe flooding in Rio Grande do Sul (RGDS).

Record-breaking rainfall in RGDS amounted to three months’ worth in just two weeks, affecting an area the size of the U.K. Some parts of RGDS saw nearly 1,000 mm of rain in two weeks, with Porto Alegre recording 327 mms in less than a week at the end of April. Flooding persisted through most of May, with depths reaching 5 meters in some areas.

Economic losses are projected to surpass $4 bn. Over 580,000 residents were displaced, more than a third of RGDS’s population lost access to running water, hundreds of thousands were without power for weeks, and 170 fatalities occurred

The flooding also disrupted health services and infrastructure, leading to outbreaks of waterborne diseases like leptospirosis, adding to the challenges faced by health authorities and emergency responders.

RGDS, a major producer of rice, soy, and livestock, is crucial to Brazil’s economy. While some crops were harvested before the floods, storage facilities were likely damaged, many livestock were lost, and remaining animals face feed shortages.

The regional airport in Porto Alegre closed for several days, and local transport networks were disrupted by flooding and landslides.

Additionally, the floods disrupted supply chains throughout the region. Major auto manufacturers such as Chevrolet and Volkswagen reported production slowdowns or stoppages.

Both the phase of the El Niño-Southern Oscillation (ENSO) and climate change are thought to have contributed to the severity of the recent flooding.

The El Niño phenomenon, characterized by warmer-than-average sea surface temperatures in the central and eastern tropical Pacific Ocean, facilitates the transport of warm, moist air toward southern Brazil.

This increased moisture supply can increase the intensity and duration of rainfall events, which leads to an elevated risk of flooding.

Compared with a neutral ENSO phase, the recent El Niño phase is estimated to have increased the likelihood of this extreme rainfall event by two to five times and its intensity by 3% to 10%.

Northeast U.S. earthquake

By analyzing near-miss catastrophes such as the April 2024 Northeast U.S. earthquake, risk managers can uncover hidden risks and vulnerabilities, improving disaster preparedness and resilience.

Unanticipated events happen because recent history provides only a limited view of what can go wrong, leaving us vulnerable to risks we have not yet imagined; however, by looking more closely at near misses in the historical record, risk managers can uncover some of these hidden threats.

Using a method called downward counterfactual analysis, businesses can better anticipate and mitigate potential risks by considering what could have happened if a near-miss disaster had turned out for the worse.

In recent years, risk managers have been increasingly recognizing the benefits of downward counterfactual analysis for near misses, such as a hurricane narrowly avoiding a major city.

The April 2024 New York City earthquake

An example of a recent near-miss event is the April 2024 Northeast U.S. earthquake. The quake struck about 40 miles west of New York City, with the epicenter located near Tewksbury, New Jersey.

The event produced widespread reports of low-to-moderate shaking across the region, including in New York City, northern New Jersey and eastern Pennsylvania

Although this earthquake was not particularly notable, it highlights the often-overlooked seismic risk in the northeastern part of the country. While damaging earthquakes are rare in this region, they can occur. Historical earthquakes include a Mw6.0 event in Boston (1755), a Mw5.8 event in northern New York State (1944) and two significant events in Greater New York City: Mw5.1 in 1737 and Mw5.3 in 1884.

Given this potential risk and New York City’s status as a major population and economic center, it is important to explore downward counterfactuals of the recent earthquake.

Using a U.S. earthquake catastrophe model, we analyzed hypothetical earthquakes affecting New York state that fall within the historically observed magnitude range of Mw4.5 to Mw5.5.

Catastrophe models include stronger earthquake scenarios above Mw6 in New York state, but such events are deemed very rare, with return periods exceeding 500 years, and so are excluded from our analysis. Instead, we focus on understanding how small, plausible perturbations to the recent earthquake could have led to larger financial losses and worse outcomes.

Record-breaking Hurricane Beryl

The first hurricane of the season, Hurricane Beryl reached Category 5 at its peak intensity. It caused significant damage and loss of life while traversing the Caribbean.

Beryl set several records during its progression across the North Atlantic. It became the easternmost June hurricane and the second-southernmost major hurricane on record.

Remarkably, within two days of forming, Beryl developed into the first-ever Category 4 hurricane recorded in the North Atlantic during the month of June. On July 1, Beryl’s sustained winds reached 165 mph, making it the earliest Category 5 hurricane and the strongest North Atlantic hurricane on record for July.

Beryl surpassed the record for the earliest-forming Category 5 hurricane by over two weeks, a record previously held by Hurricane Emily in the notably active 2005 hurricane season. While that season also experienced above-average sea surface temperatures, they were not as high as those observed in July 2024.

………………….

AUTHORS: Scott St. George – Head of Weather and Climate Research, Charlotte Dubec – Head of ESG, Global Aviation & Space WTW, Daniel Bannister – Weather & Climate Risks Research Lead, Neil Gunn – Head of Flood and Water Management Research, Jessica Boyd – Modelling Research and Innovation Lead, Jessica Boyd – Modelling Research and Innovation Lead, WTW Research Network