Fitch Ratings expects the withdrawal of hull war-risk marine insurance in the Persian Gulf to carry negative credit implications for U.S. property and casualty insurers with heavy reliance on Gulf shipping routes.

The impact for diversified global (re)insurers appears neutral because their exposure to the region remains limited.

According to Beinsure analysts, rating outcomes over the next twelve months will depend on two factors. Loss development. And how long shipping disruption lasts. Earnings volatility and capital strength will likely separate stronger insurers from weaker ones.

Specialist marine underwriters with double-digit exposure to Gulf premiums face the greatest pressure. Reduced shipping volumes could offset gains from sharply higher war-risk rates.

That dynamic raises uncertainty around earnings, reserve adequacy, and capital levels.

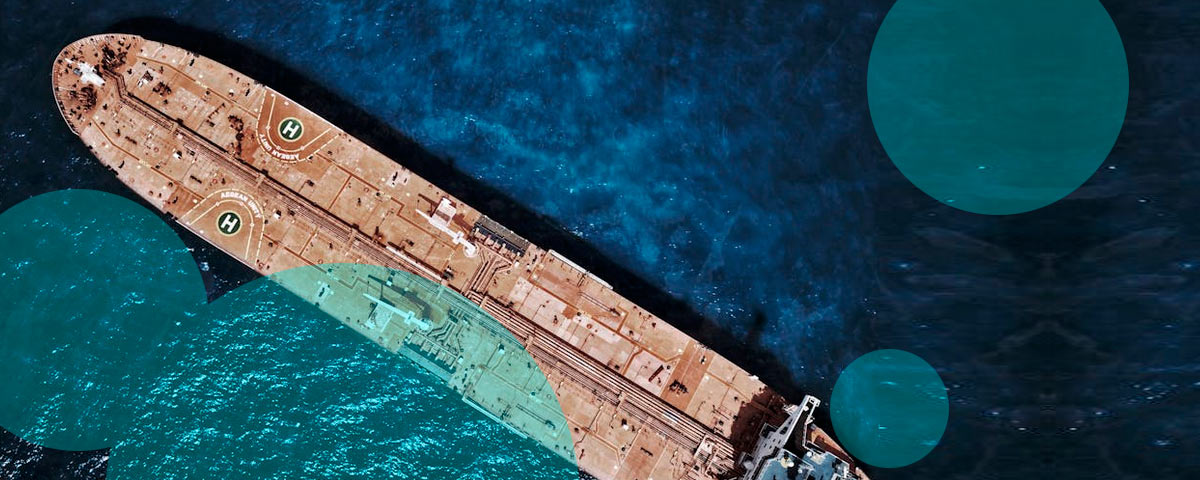

The global marine insurance market still carries large exposure to vessel losses in the region.

Skytek estimates around $22.5 bn in vessel value currently sits at risk in the Persian Gulf, including oil tankers and cruise ships vulnerable to strike damage or seizure.

Industry losses could climb above $5 bn if multiple large vessels suffer total losses. Even so, diversified multiline (re)insurers with marine war exposure below roughly 5% of premium volume should face little rating pressure because their capital buffers remain strong.

Fitch says global insurers face manageable earnings pressure from Iran conflict unless escalation damages energy infrastructure or prolongs market volatility.

Immediate risk centers on ships transiting the Strait of Hormuz. The passage carries about 20% of global oil supply, large volumes of liquefied natural gas, and roughly 30% of globally traded nitrogen fertilizer.

Shipping traffic dropped sharply after the conflict began. Lower vessel movement reduces short-term claim frequency. Exposure concentration rises at the same time because vessels remain clustered within the region.

If disruption extends beyond six months, trapped ships create compounding risk for insurers. Standard marine policies treat seized vessels as total losses when they remain unrecovered after twelve months.

War-risk premiums climbed sharply during the crisis. Coverage availability also tightened after several insurers cancelled hull war-risk policies and stopped writing new business in the Persian Gulf.

Still, abundant reinsurance capacity entering 2026 may limit the ultimate spike in marine war pricing. Premium rates will likely remain elevated through the end of the year. That environment supports underwriting margins for carriers maintaining selective Gulf exposure.

Reduced shipping volumes limit the benefit. Uncertainty around government intervention also complicates pricing decisions.

The U.S. International Development Finance Corporation announced up to $20 bn in reinsurance support covering hull, machinery war risk, and cargo exposures in the Gulf.

The program operates on a rolling basis linked to vessel transits. According to Fitch, the facility could reduce extreme tail-loss scenarios for participating insurers.

Government-backed reinsurance introduces a second effect. Subsidized capacity may displace private underwriting once the immediate crisis passes. Marine specialists could face longer-term pressure on volumes and pricing if public support remains active after shipping risks decline.