Overview

Wider natural catastrophe exposure continues to pressure financial results across the property and casualty insurance industry. Catastrophe reinsurance also limits direct losses. Beinsure analyzed the Fitch’s report and highlighted the key points.

Premium revenue growth tied to recent substantial price increases and more diligent underwriting to manage risk concentrations and aggregations point to improvement in 2024 underlying segment results.

Key Highlights

- Insured Losses Within Ratings Sensitivities. Despite high catastrophe losses, most rated insurers remain within capital and rating tolerance levels due to strong balance sheets, diversified risk, and the ability to raise premiums.

- Wide Loss Estimates from Wildfires. Insured losses from ongoing wildfires are estimated between $10 bn and $30 bn, with economic losses as high as $275 bn, reflecting the gap between insured and total damages.

- Concentration of Catastrophe Events. Hurricanes Helene and Milton contributed up to $45 bn in insured losses in 2024. Convective storms added $50 bn more over two years, with growing exposure in newly developed suburban areas.

- Rising Pressure on Weaker Insurers. Firms with limited capital and exposure beyond reinsurance protection are more likely to face rating actions, especially in wildfire-prone regions like California.

- Litigation and Inflation Driving Liability Risk. Social inflation, large jury awards, and high economic inflation are pushing up liability claims and premiums, putting reserve adequacy at risk—especially for commercial auto and long-tail lines.

Insurers may continue to struggle to generate underwriting gains depending on catastrophe loss experience, and results will vary considerably.

In 2024, global natural perils resulted in total direct economic costs of $417 bn. Of this, $154 bn was covered by private insurers and public insurance entities.

From 2017 to 2024, insurers faced an average annual loss of $146 bn from natural catastrophes, indicating a “new normal” near $150 bn annually, according to Gallagher Re’s Natural Catastrophe and Climate Report.

The direct economic cost of natural catastrophes in 2024 was estimated at $417 bin. This was 15% above the decadal (2014-2023) average of $361 bn and 16% above the most recent 20-year average ($359 bn).

When excluding earthquakes and other non-weather perils, the year’s total was $402 bn; or 20% higher than the decadal average ($335 bn) and 32% higher than the previous 20-year average ($305 bn).

Instead, industry losses were largely attributable to record severe convective storm losses totaling $59.7 bn, including 25 events that generated $1 bn or higher of losses.

The lack of a major singular loss event leads to a higher proportion of losses retained by primary insurers versus reinsurers, resulting in significant segment losses for a number of regional and mutual insurers.

Catastrophe Exposure and Market Vulnerability

Wildfires remain a concern, yet hurricanes present greater potential impact. A direct strike on Miami, for example, could cause over $100 bn in losses. A major earthquake in Los Angeles or San Francisco carries wide risk uncertainty.

Rates for property catastrophe coverage remain high due to frequent and severe weather. Larger underwriters benefit from diversified portfolios and broad reinsurance protection.

Florida presents higher risk due to the presence of small specialty insurers that rely on reinsurance and state-backed entities such as Citizens and the Florida Hurricane Catastrophe Fund. Losses exceeding reinsurance capacity could threaten these smaller companies.

Prominent natural catastrophes

Hurricanes are more variable in strength. Warmer sea surface temperatures in the Caribbean and Gulf of Mexico contribute to this shift.

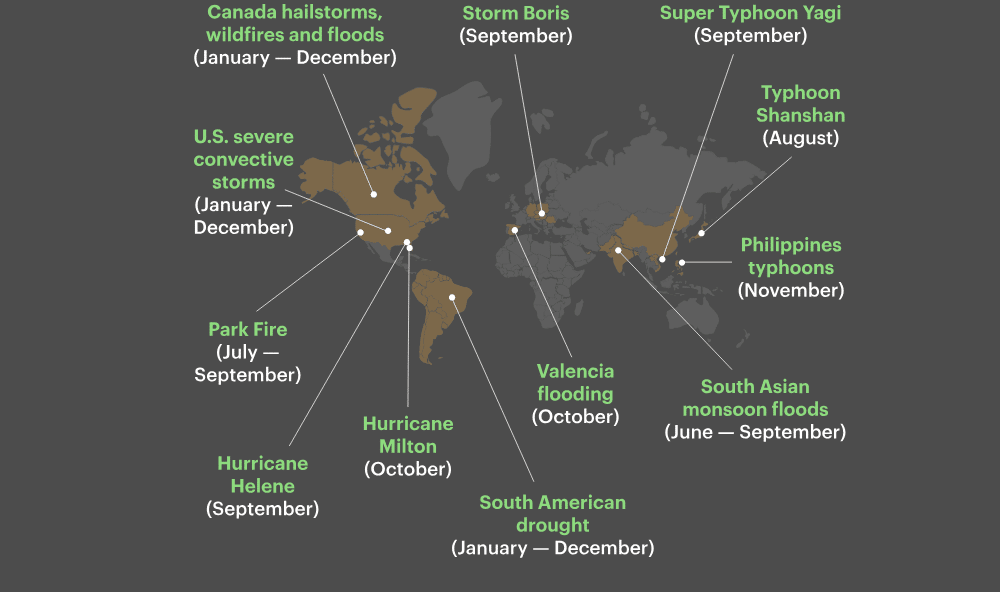

Recent storms have also affected lower-risk regions. Hurricane Helene reached Georgia with significant force, while Hurricane Debbie led to high insured losses in Quebec, where flood coverage exists unlike in the U.S.

Global insured losses exceeded $140 bn

WTW has analyzed natural disasters, key lessons, and emerging trends. The assessment will focus on physical and vulnerability factors that contributed to the most significant catastrophes in 2024.

The year saw an array of weather-related catastrophes, many of which were influenced by the effects of a warming planet. Global insured losses exceeded $140 bn, marking the fifth consecutive year above $100 bn.

Meanwhile, the insurance protection gap remained substantial, with total economic damages exceeding $350 bn, highlighting the inadequacy in resilience to climate-related risks in insurance.

Offering a smarter way to risk, this report goes beyond the numbers to provide new perspectives to help with natural catastrophe risk management and resilience across multiple sectors.

Fires burning in the Los Angeles will result in insured losses

The multiple fires burning in the Los Angeles area will result in insured losses that materially exceed highs from past wildfire events but are not likely to affect ratings of P&C (re)insurers, Fitch Ratings says.

Insured losses should remain within ratings sensitivities for affected issuers, given ample capital levels, diversified risk exposure and insurers’ ability to increase premium rates.

Estimating insured losses is difficult given that fires are not fully contained. Nonetheless, significantly wide estimates for insured losses range between $10 bn and $30 bn, and economic losses between $150 bn to $275 bn.

Expected losses for rated (re)insurers, while not affecting capital, will reduce near-term earnings, depending on exposure to claims from homeowners, auto, commercial property, and business interruption insurance.

Insurance Loss Trends and Regional Risks

In 2024, the most significant insured catastrophe losses in the U.S. came from Hurricanes Helene and Milton, with combined estimates between $30 bn and $45 bn.

Convective storms added more, with insured losses of $50 bn across two years. Storms increasingly impact central U.S. suburbs, where new housing developments are more exposed.

Fires and earthquakes continue to produce higher economic losses than insured ones. Insurance gaps contribute to this difference. Many individuals remain uninsured or underinsured relative to current property values. Earthquake insurance remains limited, with California’s take-up rate at just 10%.

Insurers most susceptible to negative rating actions

Companies most susceptible to negative rating actions are those where wildfire losses exceed earnings and reinsurance limits, weakening capital relative to rating sensitivities.

Insurance losses could pressure weaker capitalized companies, increase reinsurance costs, and further strain a system that has seen insurers retreat from the market.

Several insurance companies have stopped writing new business in the state after reevaluating wildfire risk, pricing, and reinsurance market conditions.

Wildfire risk, while a growing source of insured losses in California, was previously viewed as a secondary peril to more costly hurricane and earthquake insured losses.

Notably, the wildfire seasons of 2017 and 2018 included the Tubbs and Camp Fires with insured losses of $11.1 bn and $12.5 bn respectively, per Aon.

Insurers operating in California contribute to the FAIR Plan based on market share, spreading the risk of high-loss events.

Large catastrophic losses can strain the financial resources of the FAIR Plan, potentially leading to assessments or surcharges on participating insurers to cover deficits.

Significant losses can lead to increased premiums or reduced coverage availability in the private market as insurers adjust to offset their increased liabilities from FAIR Plan contributions.

Financial Stability, Legal Pressures, and Reserve Adequacy

The industry can manage individual large events but is at greater risk if several events occur in close succession. This occurred in 2001–2002, which included the 9/11 attacks, hurricanes, reserve shortfalls, and an equity downturn.

A severe equity market drop remains a threat to capital surplus, as seen in 2001, 2008, and 2022.

Social inflation also increases casualty losses. Mass tort cases and large jury awards have become more common, especially as post-pandemic court activity rises.

These trends mirror earlier waves of litigation in the 1970s and 2000s. Legal costs continue to rise, pushing insurance premiums upward.

High inflation and weak economic growth risk undermining loss reserve adequacy. Commercial auto and liability lines are most exposed.

Insurers’ ability to project loss severity accurately under inflation and litigation pressure is critical. Inaccurate pricing and reserve development may lead to reserve increases and reduced profitability.

The fingerprints of climate risk do undeniably exist on many individual events. One must understand that climate risk is not solely an issue for physical damage potential, however, and the non-physical implications are substantial.

This may affect sectors such as real estate, agriculture, industry and manufacturing; as well as impacting health and retirement, and the long-term strategies of investors (see Top 10 Risks for the Global Insurance Industry).

The reduction of greenhouse gas emissions is essential to this process, and this will be vital in stabilizing or reducing the impact of future extreme weather events.

FAQ

Most insurers remain within tolerance limits due to strong capital, diversified portfolios, and pricing flexibility, so ratings should remain stable for most.

Fires are ongoing and not fully contained, leading to wide loss estimates and uncertainty in final insurance and economic impacts.

Homeowners, auto, commercial property, and business interruption insurance are key segments impacted by wildfire and storm-related claims.

Companies are reevaluating risk and pricing, especially in wildfire-prone states like California, where reinsurance costs and exposure levels are rising.

It spreads catastrophic risk across insurers based on market share. Major losses can strain its resources, leading to surcharges or higher premiums across the market.

Climate risk affects sectors like real estate, agriculture, and health. It also impacts investment strategies and long-term insurer planning.

High inflation, slow economic growth, and litigation trends challenge insurers’ reserve adequacy, particularly in long-tail liability lines like commercial auto.

…………………

AUTHORS: Gerry Glombicki, CPA, CISSP, CCSP, CISA, ARM – Senior Director, North American Insurance at Fitch Ratings (Chicago), Laura Kaster, CFA – Senior Director, Risk for North and South American Financial Institutions, Credit Commentary & Research at Fitch Ratings

Edited by Nataly Kramer