Overview

WTW has analyzed natural disasters, key lessons, and emerging trends. The assessment will focus on physical and vulnerability factors that contributed to the most significant catastrophes in 2024. Beinsure has highlighted the key insights from the WTW’s Natural Catastrophe Review.

The spotlight on climate change intensified in 2024 as the global mean temperature exceeded 1.5°C above pre-industrial levels for the first time.

The year saw an array of weather-related catastrophes, many of which were influenced by the effects of a warming planet. Global insured losses exceeded $140 bn, marking the fifth consecutive year above $100 bn.

Meanwhile, the insurance protection gap remained substantial, with total economic damages exceeding $350 bn, highlighting the inadequacy in resilience to climate-related risks in insurance.

Offering a smarter way to risk, this report goes beyond the numbers to provide new perspectives to help with natural catastrophe risk management and resilience across multiple sectors.

Credible data and risk models can help you make informed choices about trade-offs: making investments to become more resilient, buying more insurance protection, or accepting the risk. Beware of becoming overly committed to one approach.

Peter Carter, Head of Climate Practice, WTW

“Simply having lots of data or a single modelling approach may not give the robust risk perspectives you need. Seeking

expert input and a more nuanced modelling approach, where you challenge your core modelling approach (“defender”) with a different approach (“challenger”) will provide alternative perspectives. Then you will navigate an increasingly volatile natural hazard environment much more effectively,” Peter Carter said.

Key Highlights

- $140bn Insured Losses – Global insured losses from natural catastrophes in 2024 surpassed $140bn, marking the fifth consecutive year above $100bn.

- $350bn Economic Damages – Total economic losses from natural disasters exceeded $350bn, highlighting a persistent protection gap.

- 8 Category 4+ Hurricanes – Since 2017, eight Category 4+ hurricanes have made landfall in the U.S. Gulf Coast, compared to just eight in the previous 57 years.

- 500,000 Heat-Related Deaths – Extreme heat events contributed to approximately 500,000 heat-related deaths globally in 2024.

- $50bn U.S. Storm Losses – Severe convective storms in the U.S. generated over $50bn in insured damages for the second consecutive year.

- $5.6bn Canadian Insured Losses – Canada experienced its costliest year for natural disasters, with insured losses reaching $5.6bn.

- €31bn Flood Loss Projection – Under a 2°C warming scenario, annual flood-related economic damages in Europe could rise to €31bn by 2050.

Pre-season forecasts of North Atlantic hurricane activity in the 2024 season were particularly high. All major forecasters agreed that the season would be extremely active with a much higher number of storms than average.

Ultimately, despite the useful indicativeness of seasonal hurricane activity forecasts, there appears to be a general tendency toward overconfidence.

The most credible forecasts are therefore those with the widest uncertainty ranges. Getting out of Model Land and improving the forecasts will require a concerted push for greater model diversity, followed by a longer-term approach to quantitative evaluation.

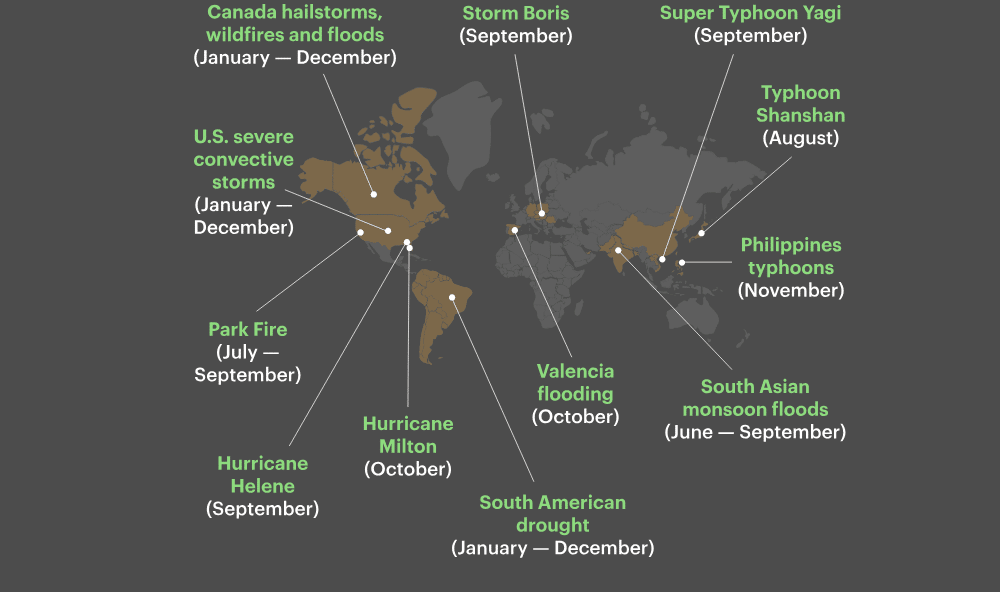

Prominent natural catastrophes discussed in this Natural Catastrophe Review

However, the Paris Agreement’s target refers to long-term average temperatures, meaning a single year exceeding this threshold does not constitute a permanent breach. Nonetheless, the latest temperature data highlight the rapid rate at which the Earth is warming. All of the past 10 years now rank in the top 10 warmest on record.

A key contributor to the record-high temperatures in both 2023 and 2024 was El Niño, which peaked in December 2023 but continued to influence global temperatures during 2024.

By May 2024, neutral El Niño-Southern Oscillation conditions had developed, with sea surface temperatures gradually returning to near-average levels in the Central and Eastern Pacific.

Gulf of Mexico sea surface temperature anomalies relative to the 1991 – 2020 average

The Intergovernmental Panel on Climate Change projects that a warming climate will increase the frequency of Category 4+ storms. As a result, risk managers are closely watching this trend, adjusting catastrophe models and refining strategies to better align with the evolving risk landscape.

The 2024 season exemplified a recent trend of strong storms impacting the U.S. Gulf Coast. Since 2017, eight Category 4+ hurricanes — Harvey, Irma, Maria, Michael, Laura, Ida, Ian and now Milton — have made Gulf landfalls.

By contrast, the previous eight Category 4+ landfalls spanned 57 years (1960 – 2016).

Research from the WTW Research Network, led by Dr. James Done at the U.S. National Center for Atmospheric Research, reveals that 2024’s heat records reflect a broader trend: Extreme heat events in cities have quadrupled in frequency over the past 40 years, with heat waves now lasting twice as long in some regions.

These extreme heat events highlight the growing effects of climate change on health, infrastructure and ecosystems, with extreme heat now responsible for approximately 500,000 heat-related deaths annually worldwide.

Extreme Weather Events in 2024

In the second half of 2024, hurricanes Helene and Milton caused widespread damage, leading to more than $40 bn in insured losses.

In the western North Pacific, Super Typhoon Yagi ranked among the 10 costliest storms ever recorded, with economic losses surpassing $15 bn across Southeast Asia and South China.

Severe convective storms in the U.S. continued their trend of high losses, exceeding $50 bn in insured damages for the second consecutive year . Canada faced its most expensive year for natural catastrophes, with hailstorms, floods, and wildfires pushing insured losses to $5.6 bn.

List of 2024 North Atlantic hurricanes (Category 1+)

| Hurricane | Dates Active | Maximum Category | Direct Landfalls |

| Beryl | June 28 – July 9 | 5 | Grenada, Saint Vincent and the Grenadines, Yucatán Peninsula, Texas |

| Debby | Aug. 3 – 9 | 1 | Florida, South Carolina |

| Ernesto | Aug. 12 – 20 | 2 | Bermuda |

| Francine | Sept. 9 – 12 | 2 | Louisiana |

| Helene | Sept. 24 – 27 | 4 | Florida |

| Isaac | Sept. 26 – 30 | 2 | None |

| Kirk | Sept. 29 – Oct. 7 | 4 | None |

| Leslie | Oct. 2 – 12 | 2 | None |

| Milton | Oct. 5 – 10 | 5 | Florida |

| Oscar | Oct. 19 – 22 | 1 | Bahamas, Cuba |

| Rafael | Nov. 4 – 10 | 3 | Cuba |

Flooding caused major disruptions worldwide. Europe experienced one of its worst years for flood-related damages. In Spain, floods in Valencia resulted in $3.7 bn in insurance claims, marking the country’s most expensive natural catastrophe.

Storm Boris brought extreme rainfall to Central and Eastern Europe, generating $2.2 bn in claims. In South Asia, heavy monsoon rains affected millions and disrupted agriculture, energy, and manufacturing.

Earlier in the year, severe floods hit the United Arab Emirates, Brazil, China, and Germany.

While some regions struggled with excess water, parts of South America suffered from severe drought. The crisis disrupted agriculture, energy, and transportation, underscoring the widespread impact of climate-related risks.

Record-Breaking Global Temperatures

For the first time, the annual global mean temperature in 2024 surpassed 1.5°C above pre-industrial levels, averaging 1.55°C above the 1850–1900 baseline.

The World Meteorological Organization confirmed this record, marking a critical threshold identified in the 2015 Paris Agreement to prevent the worst effects of climate change.

This follows 2023, which set its own record at 1.48°C above pre-industrial levels.

Annual global surface temperature anomaly relative to a pre-industrial baseline (1850 – 1900)

The Expanding Role of Climate Change

The rising financial toll of natural catastrophes reflects both the increasing number and value of assets at risk. However, climate change is also playing a growing role, with multiple events in 2024 linked to human-induced warming.

Rapid attribution has become a key tool in assessing these connections. Scientists, including those at the World Weather Attribution project, now quickly determine how climate change has influenced the likelihood or intensity of specific disasters.

In 2024, rapid attribution studies provided new insights into climate-related weather patterns. Researchers found that exceptionally warm sea surface temperatures in the Gulf of Mexico were 200 to 500 times more likely along Hurricane Helene’s path and 400 to 800 times more likely along Hurricane Milton’s path due to human-caused warming.

In Central and Eastern Europe, Storm Boris produced 10% more intense rainfall and was twice as likely to occur because of climate change. The severe drought in South America was found to be 30 times more likely as a result of human-induced warming.

These findings reinforce the need for both mitigation and adaptation strategies. Investments in protective infrastructure, such as flood defenses, and adequate insurance coverage are essential to narrowing the protection gap and enhancing financial resilience.

Rising Interconnected and Compounding Risks

Climate change is also amplifying interconnected risks across industries. The 2024 South American drought, influenced by both El Niño and climate change, affected energy, transportation, agriculture, and businesses simultaneously. Manufacturing and food processing firms, which depend on electricity, water, and transportation, faced operational disruptions, compounding economic losses.

Aging infrastructure, combined with extreme rainfall, has also increased the risk of dam failures. In 2024, heavy rainfall triggered multiple dam failures worldwide, leading to floods that displaced populations and disrupted local economies.

These examples highlight how climate-related disasters create cascading effects, requiring cross-sectoral approaches to resilience and risk management.

This In 2024, a mid-season lull in North Atlantic hurricanes raised questions about forecast accuracy. WTW Research Network partner Dr. Erica Thomson examines the reliability and limitations of pre-season hurricane forecasts.

Insured losses and the challenges ahead

As of November 2024, PERILS estimated the insured loss from Boris to be around €2 bn, with 95% coming from Austria, the Czech Republic and Poland.

Other notable flood losses in Europe in 2024 include: Germany (July 2024): Insured losses estimated at €1.7 bn Valencia, Spain (October 2024): Estimated insured losses of €3.5 bn.

Combined, these events will add to a bruising few years for European insurers, who also experienced significant claims from Storm Bernd flooding in 2021 (€13.5 bn) and hailstorms in 2023 (€7 bn).

While European insurers remain well capitalized to pay extreme weather claims, the recent flood events are part of a broader pattern of costly natural disasters in recent years, especially from so-called secondary perils, the cumulative effect of which is adding pressure to the global availability and affordability of (re)insurance.

The effects of climate change

The event brought the heaviest rainfall ever recorded in Central Europe, with scientists estimating that climate change made the precipitation 10% more intense and twice as likely. Researchers also found that the storm affected an area 18% larger than it would have in a cooler climate.

Storm Boris demonstrated the benefits of investing in flood defenses and early warning systems; however, more investment is still needed to reduce the risks of future flooding.

The European Union’s Joint Research Centre estimates that 160,000 Europeans are currently exposed to flooding each year, resulting in average annual economic damages of €7.6 bn. But under a 2°C warming scenario, these figures are expected to rise to 365,000 people and €31 bn annually in 2050.

Proactive risk management

The flooding seen across Europe this year, which also includes Valencia and Germany, will add to concerns among risk managers about the availability of affordable property insurance in a warming world. As a result, businesses are increasingly adopting a proactive, forward-looking approach to flood risk management to better protect their

assets, infrastructure and supply chains.

This requires knowledge of current asset or portfolio flood risks and an awareness of how the risk profile could change in

the future under different climate scenarios.

However, this can be challenging due to data limitations, modeling uncertainties and the sensitivity of floods to site-specific conditions.

Risk managers can address these challenges by using reliable information sources, such as frequently updated national flood maps and bespoke flood models. To ensure a robust risk assessment, careful consideration should be given to factors such as the spatial resolution of maps and models as well as the representation of flood defenses.

Comprehensive risk assessments, combined with mitigation measures — such as protecting key equipment and developing comprehensive emergency plans — can reduce potential losses, demonstrate well-managed risks to insurers, and help secure more favorable premiums and coverage.

Probabilistic forecasts (which is effectively what these are, even those that state a single number) cannot be assessed solely on how well they perform in a single year. We need to look at previous years as well to get an overall picture of reliability.

Interestingly, across the past 24 years, the differences between forecast and observations are usually in the same direction for most modeling groups. If the ensemble was unbiased, then the residuals would be randomly spread around the zero line, but instead they often all fall on the same side of it

FAQ

Hurricanes Helene and Milton caused over $40bn in insured losses, while Super Typhoon Yagi led to $15bn in economic losses across Southeast Asia and South China.

The year saw record-high global temperatures, with warming trends intensifying extreme weather events like hurricanes, floods, and heat waves.

El Niño contributed to record-high temperatures, peaking in December 2023 and influencing global weather patterns through mid-2024.

Despite insured losses exceeding $140bn, total economic damages were more than $350bn, highlighting a substantial gap in coverage.

Europe faced one of its worst flood years, with Spain’s Valencia floods resulting in $3.7bn in claims. Storm Boris caused $2.2bn in damages across Central and Eastern Europe.

Energy, transportation, agriculture, and manufacturing faced disruptions due to droughts, hurricanes, and extreme heat.

Investing in flood defenses, adopting proactive risk management strategies, and utilizing updated catastrophe models can enhance resilience and reduce financial exposure.

……………….

QUOTES: Dr. Erica Thomson – WTW Research Network partner – Senior Policy Fellow in Ethics of Modelling and Simulation at the LSE’s Data Science Institute, funded by a UKRI Future Leaders Fellowship, Peter Carter – Head of Climate Practice, WTW.

Edited by Nataly Kramer