Overview

The 2024 Atlantic hurricane season ended on November 30, marking a year of above-average storm activity and substantial insured losses in the U.S. The National Oceanic and Atmospheric Administration (NOAA) recorded 18 named storms with winds of 39 mph or higher, according to BestWire report.

11 became hurricanes, and five were classified as major hurricanes with wind speeds of at least 111 mph. Five of these storms made landfall in the continental U.S. For comparison, a typical season includes 14 named storms, seven hurricanes, and three major hurricanes.

Seven hurricanes formed in the Atlantic after September 25, the highest number on record for that period, according to NOAA. Total economic losses for the 2024 hurricane season were approximately $110 bn across North America, with insured losses estimated at about $49 bn, according to Munich Re.

MS Amlin, a global re/insurer at Lloyd’s, projects that the 2024 Atlantic hurricane season will be notably above average and potentially one of the most active on record.

Climate scientists at MS Amlin analyzed forecasts from 24 research entities, including private companies, universities, and government agencies.

Their consensus anticipates an average of 23 named storms, 11 hurricanes, and 5 major hurricanes. In comparison, the 2023 season recorded 20 named storms, 7 hurricanes, and 3 major hurricanes.

The Accumulated Cyclone Energy (ACE) index, which quantifies overall hurricane activity by considering the number, intensity, and duration of named storms, is predicted to reach 204, significantly higher than the long-term average of 123.

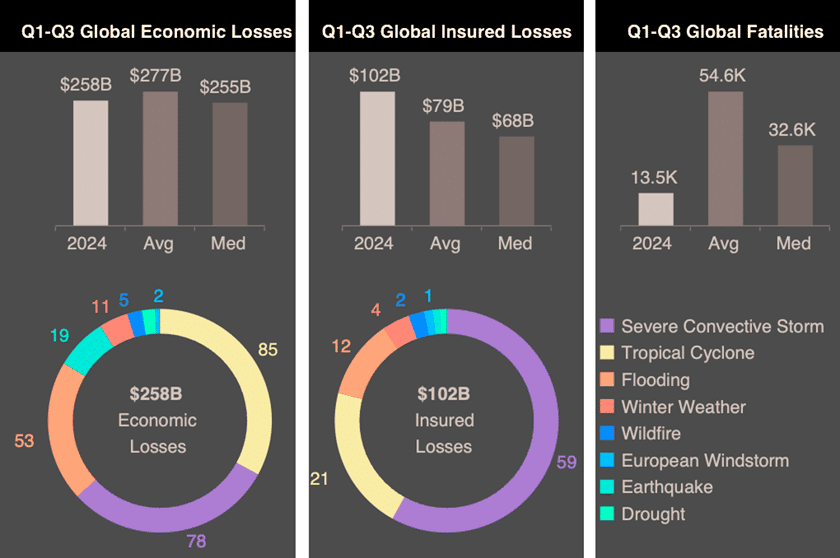

According to 2024 Global Catastrophe Report, Q3 2024 saw a number of significant disaster events, which drove total economic losses from natural catastrophes above at least $258 bn. This was lower than the 21st-century Q1-Q3 average of $276 bn and significantly lower than losses in the same period of last year ($351 bn).

Major Storms and Insured Losses

Florida insurers faced over $5.3 bn in claims due to Hurricane Helene in late September and Hurricane Milton in early October, according to Florida Office of Insurance Regulation data. Helene also caused significant damage in other southeastern U.S. states (see U.S. Insured Losses from Hurricanes).

Mark Friedlander, a spokesperson for the Insurance Information Institute, stated that U.S. property insurers managed the season’s impacts effectively.

Hurricanes Beryl, Debby, and Francine primarily resulted in flood-related losses with minimal wind damage. Helene brought more substantial damage but produced only moderate insured wind losses.

Milton was the most significant wind event of the season, but insured losses were much lower than initial catastrophe modeler projections.

Aon projected global reinsurer capital at nearly $700 bn as of June 30, with growth expected into 2025, barring significant catastrophic events.

Elevated North Atlantic hurricane activity, which was initially anticipated, only intensified in the latter half of the season with Hurricanes Helene and Milton.

Some insurers have combined losses from the back-to-back storms. Progressive Corp. reported $360.1 mn in combined losses, expenses, and unfavorable development from the two hurricanes in October.

Allstate Corp. estimated $286 mn in losses for the first month of Q4 2024, mainly due to Hurricane Milton and unfavorable reserve adjustments from Helene.

Lloyd’s estimated cumulative final net losses from Helene and Milton could range from $1.8 bn to $3.4 bn.

Lloyd’s Chief of Markets, Patrick Tiernan

Additionally, Florida insurers reported $131 mn in losses from the earlier, less-destructive Hurricane Debby.

North American hurricanes and Northwest Pacific cyclones caused $51 bn in total insured losses in 2024, significantly above the 10-year average, according to Munich Re.

The season’s tropical cyclones were notably severe due to elevated sea surface temperatures, which Munich Re attributed to climate change.

Natural disasters led to an estimated $258 bn in global economic losses for Q1–Q3 2024, about 7% below the long-term average of $277 bn since 2000 and slightly above the median of $254 bn

There were 47 events causing losses over $1 bn, with 32 in North America, eight in Asia, four in EMEA, and three in South America. These figures remain provisional, as individual event loss estimates often change months after occurrence.

Market Implications and Future Projections

Natural catastrophes in the U.S. accounted for nearly 80% of global insured losses in the first three quarters of 2024, a figure one-third higher than the long-term average since 2000, according to Aon.

Hurricane Helene, which made landfall on Florida’s west coast with 140 mph winds, was the costliest global event of the year’s first three quarters. Helene’s preliminary economic losses in the U.S., Mexico, and Cuba totaled $55 bn, with insured losses reaching several billion dollars.

This was more than triple the second-highest loss event of 2024, the Noto Earthquake in Japan, which caused $17.9 bn in damages.

The 2024 Atlantic hurricane season started with Beryl, the earliest-ever Category 5 storm, which made landfall in two countries before hitting Texas on July 8 as a Category 1 storm.

The Texas Wind Insurance Association projected Beryl’s losses and related expenses could reach $455 mn, nearly equivalent to the association’s catastrophe reserve trust fund balance.

Global economic and insured losses from natural catastrophes

Looking ahead, NOAA and partner researchers project a 36% increase in Atlantic hurricane season variability by mid-century. This shift could produce more active hurricane seasons, though long-term trends may also see inactive periods. As climate change influences sea surface temperatures, insurers and policymakers face growing uncertainty in forecasting storm intensity and frequency.

The insurance protection gap reached an estimated 60% in Q1–Q3, one of the lowest recorded levels, largely due to increased insured losses in the U.S. Fatalities totaled approximately 13,000, the lowest since 1986.

Insured losses from primary perils in the first nine months of 2024 were mild overall, with no single event likely to impact the broader reinsurance market.

Most losses, including those from severe convective storms, remained with insurers in Q3, maintaining exceptional returns for reinsurers.

FAQ: 2024 Atlantic Hurricane Season and Insured Losses

The 2024 season recorded 18 named storms, 11 hurricanes, and 5 major hurricanes. This was above the long-term average of 14 named storms, 7 hurricanes, and 3 major hurricanes. Seven hurricanes formed after September 25, setting a new record for that period.

Total economic losses for the season reached about $110 bn across North America, with insured losses amounting to approximately $49 bn, according to Munich Re.

Hurricanes Helene and Milton caused the most significant insured losses. Florida insurers faced over $5.3 bn in claims from these storms. Helene caused damage across several southeastern U.S. states, while Milton produced substantial wind-related losses.

Progressive Corp. reported $360.1 mn in combined losses, expenses, and unfavorable development from Helene and Milton. Allstate Corp. estimated $286 mn in Q4 losses due to Milton and reserve adjustments from Helene. Lloyd’s projected cumulative net losses from Helene and Milton to range from $1.8 bn to $3.4 bn.

Munich Re attributed the severity of the season’s tropical cyclones to elevated sea surface temperatures, which are linked to climate change. NOAA projects a 36% increase in hurricane season variability by mid-century, leading to more unpredictable storm activity.

Despite significant insured losses, most losses from Q3 natural disasters remained with insurers. The reinsurance market maintained strong returns, with global reinsurer capital projected at nearly $700 bn as of June 30. Losses from hurricanes were substantial but not enough to disrupt the broader reinsurance market.

The insurance protection gap for Q1–Q3 2024 was around 60%, one of the lowest on record. This was primarily due to increased insured losses in the U.S., which reduced the proportion of uninsured economic losses.

…………………

AUTHOR: Renée Kiriluk-Hill – Senior Associate Editor at AM Best. Edited by Nataly Kramer — Editor at Beinsure Media