Overview

As property and casualty insurers in the United States struggle to maintain profitability, executives will need to direct a coordinated response across pricing, underwriting, claims, and other functions.

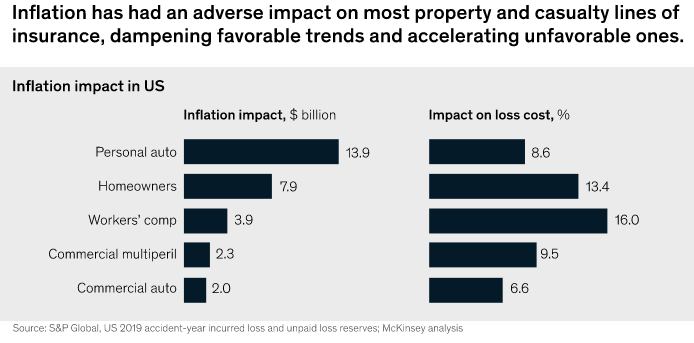

The insurance industry faced challenges to profitability even before the pandemic, and the sudden unexpected spike in inflation has only added to them. McKinsey estimates show that rising prices contributed to an approximately $30 billion increase in loss costs—the amount an insurer must pay to cover claims—in 2021, over and above historical loss trends (see How High Inflation & Base Rates Can Impact to (Re)Insurers?).

Price increases have been exceptionally high for the goods and services that drive personal insurance claims.

For example, prices for motor vehicle parts and equipment rose 22.8 percent between June 2021 and June 2022, while the cost of used cars and trucks rose 14 percent. Supply chain disruptions and other causes of inflation in the automotive industry led to an estimated $9 billion in loss costs for auto physical damage in 2021.

Loss costs for lines with long settlement periods, such as workers’ compensation, went up by an incremental $4 billion, and high prices for core commodities drove up loss costs in multiperil insurance lines, both personal and commercial, by an incremental $8 billion and $2 billion, respectively.

Under these circumstances, short- and long-term strategies for insurers revolve around savvy pricing, expense management discipline, and claims operational excellence. We can’t predict the exact path of inflation and interest rates, but we see several key variables to watch and three possible scenarios that carriers should consider preparing for.

Key indicators as claims costs continue to rise

As insurers plan their response to inflationary pressures, they should monitor four important measures: general inflation, claims cost inflation, wage inflation, and interest rates (see How Artificial Intelligence Can Help Insurers Reduce the Inflation Impact?).

General inflation

The US Federal Reserve’s interest rate policy will depend on the agency’s expectations for how inflation will play out. Any signs of long-term expectations becoming “unanchored” and trending above 2% could cause concern and lead to aggressive policy intervention, as noted during the March meeting of the Federal Open Market Committee.

For insurers, high general inflation creates an environment that favors assertive premium and pricing strategies.

This requires discipline in managing account pricing: smart insurers build in favorable premium trends, improve pricing and filing responsiveness and agility, and reduce calendar period exposure through product enhancement and innovation.

Claims cost inflation

The most important factor for P&C carriers to watch is claims cost inflation above and beyond general inflation. The factors driving claims cost inflation differ across lines of business (see How Inflation Challenging Insurer Profitability?). Supply chain disruptions have had strong effects on specific goods, such as vehicles and vehicle parts; global market upheavals have been particularly pronounced in the commodities and energy sectors.

To manage such costs effectively, insurers will need to focus on increasing claims productivity and automation and improving or repairing managed-care network utilization and negotiated pricing while also balancing cycle time improvements with claims accuracy.

Wage inflation

During the early days of the pandemic, the labor market participation rate declined to a low of 60.2 percent in April 2020 (see about Negative Effects of Inflation on the Insurance). Two years later, participation was at 62.2 percent, still well below the prepandemic level of 63.4 percent in February 2020. As the labor market continues to tighten, insurers must stay alert for increasing wage pressure on overall expense ratios. This will mean maintaining expense management discipline and transparency, as well as investing in increased productivity and digital self-service.

Interest rates

As the Fed adjusts its targets for the federal funds rate, Treasury rates and other returns across the insurer’s portfolio will rise. This may offset some of the margin pressure caused by increased claims and wage inflation and will allow leading insurers with advanced pricing capabilities to invest in gaining market share.

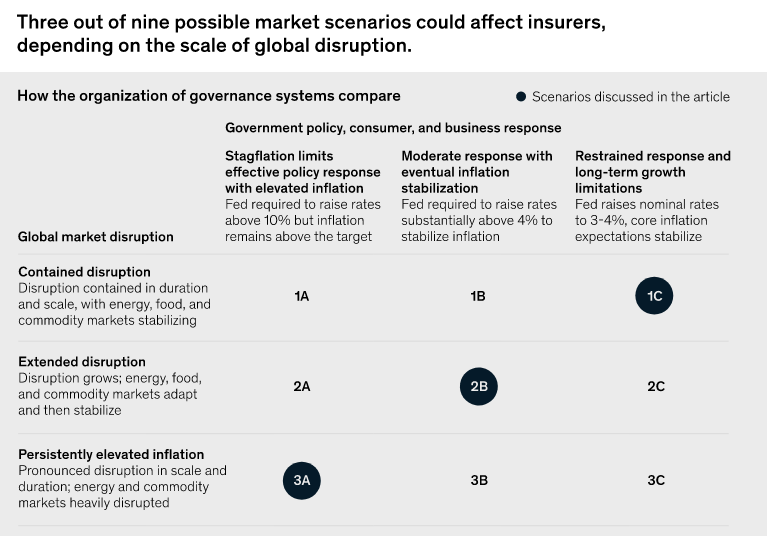

Three primary scenarios will present opportunities and threats

Based on global market situations and responses from governments, businesses, and consumers, we identified nine possible scenarios and identified three that appear most relevant for insurers in the months and years to come.

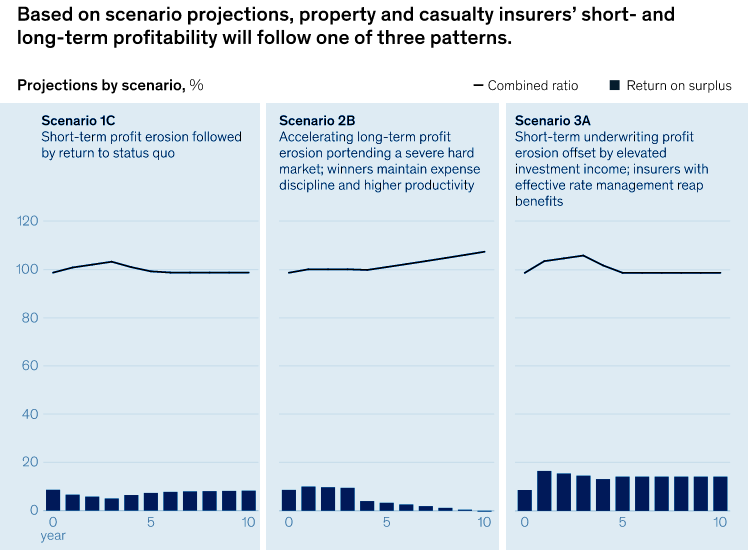

Based on these scenarios, insurers’ profitability will follow one of three patterns.

- Scenario A: Stabilization. In the most optimistic view, energy, food, and commodity markets would stabilize, and in response, the Fed would most likely stay on its current path, raising policy rates to 3 to 4 percent. Inflation expectations would remain stable, and actual inflation would recede going into 2023. For insurers, this is likely to represent a near-term erosion in combined ratios (losses and expenses in relation to total collected premiums) and overall profitability, but with an ultimate return to long-term norms. This scenario favors carriers with large and diversified portfolios, healthy surpluses, and operational excellence, particularly in expense and claims management.

- Scenario B: Continued disruption. If conflicts in Eastern Europe intensify and COVID-19 continues to affect the global economy, there is a real risk that global markets will continue to be disrupted, with energy and commodity prices continuing to experience volatility and general inflation. In response, the Fed might find itself forced to hike policy rates substantially above 4 percent to keep long-term inflation expectations anchored. This might have adverse effects on the overall economy, particularly real estate construction. For insurers, this scenario would translate into more persistent profitability challenges—a worse scenario than one with consistently higher inflation. Claims costs would continue to rise because of disruptions in global commodity markets, but moderate general inflation could prevent insurers from increasing premiums for customers. The result could be a severe contraction in underwriting capacity and a hard market with more stringent underwriting standards. Insurers that come out ahead will be those with superior underwriting and pricing discipline and a focus on profitable pockets of the market.

- Scenario C: Persistently elevated inflation. Finally, while less likely, major disruptions of global markets could drive global energy and commodity prices to longer-term elevated inflation. In such a situation, the Fed might see a need to raise interest rates even higher but might not be able to control inflation. Should expectations become unanchored and the economy continue to struggle under global market disruptions and restrictive policy, the US could enter a new period of stagflation—that is, with inflation remaining elevated despite high interest rates and slow economic growth. For insurers, this scenario would cause significant short-term disruption in combined ratios and underwriting profit. However, as sometimes happens in foreign markets with persistently high inflation, the long-term outlook might permit premiums and investment returns to rise at the same pace as expenses and loss costs. This market will favor P&C carriers that can bring operational excellence to the entire value chain, especially those with better pricing strategies and underwriting discipline.

Insurers can handle any scenario if senior executives drive a well-coordinated approach to countering inflation across all functions of the value chain.

Leaders may want to consider preparing a “resilience playbook” that allows them to deploy tactics as conditions warrant. This means creating visibility into the value at risk, time to deploy, and investment required for each lever being considered. It also means setting measurable thresholds for taking such actions and having the organizational alignment and resources ready to handle risk. The playbook can be scripted by addressing issues such as where customers will see value in the new environment, how to pursue repricing, and how to set priorities and organize activities.

Individual tactics will differ by function, but collectively, the chief product officer, chief claims officer, and CFO can build enterprise-wide resilience by taking the following recommended actions.

Chief product and underwriting officers

The company’s chief product and underwriting officers should focus on creating maximum insight into product profitability, developing rate indications frequently and with the most granularity possible to enable quick action. Leading carriers should maintain visibility into data indicators that provide early warning. High inflation worsens carriers’ existing operational weaknesses, such as vulnerability to runaway verdicts—excessive awards for damages, also known as social-inflation verdicts—premium leakage problems from undisciplined underwriting practices, and/or slow and inefficient rate management tools.

The solution is to catalog all available pricing and rate levers to seize opportunities and to identify and triage existing sources of leakage.

Successful underwriting officers will push rate targets to the lowest accountable personnel in the product or underwriting organization, vigilantly monitor the rate actions taken, and emphasize accountability and urgency to ensure value capture.

In an environment of rapidly rising prices, speed to market is critical. Delays of just a few months can cost millions of dollars of lost revenue. Achieving such speed can vary across lines of business. Carriers should file and/or steepen product class factors that track with expected inflation, generating an automatic pipeline rate.

For inoculation against extended earn-in periods and uncertainty, this may be the time to consider reducing policy calendar exposure from 12 months to six months or less, achieve further innovation in usage-based exposures, or expand retrospective-rating pricing methods (premiums that adjust based on the losses that occur during the pricing period). This may also be a good time to review portfolio exposure to long-tail lines and consider rebalancing the portfolio mix and growth appetite in favor of short-tail exposures that can be settled quickly.

The inflationary environment and the need to act quickly further reinforce the imperative for carriers to transform their underwriting capabilities.

Leading carriers are developing digital workflows, fusing underwriting “judgment” with science by leveraging data and analytics. Many carriers are facing stiff competition for top underwriting talent; by transforming the way underwriters work, carriers can not only realize benefits from better risk selection but also sharpen their employment value proposition to underwriters, who can focus on making decisions over administrative and highly transactional tasks.

In addition, high inflation effectively shrinks a carrier’s real portfolio and leaves policyholders increasingly underinsured as rising replacement costs exceed coverage limits. This is a time to offer increased limits and proactively review coverage needs with customers and agents to ensure that adequate coverage is provided, thereby supporting the best customer experience.

Chief claims officer

Insurance companies that achieve excellence in claims management will be more resilient in responding to loss pricing pressures. Chief claims officers play a critical role in managing the end-to-end claim process, including goals for customer satisfaction and cycle times.

In times of inflation, these executives should increase focus on claim types with the greatest exposure to price inflation and those with the longest cycle times.

By highlighting cycle time variability and creating a sense of urgency among the frontline staff, chief claims officers can help drive efficiency via operational excellence.

Investment in automation and straight-through processing without manual input also can contribute to driving down costs and give organizations breathing room to absorb pricing shocks.

Straight-through claims processing may give customers increased choice over whether they receive direct settlement or repair, balancing loss accuracy accordingly. Furthermore, managed-care and property repair networks represent an opportunity to negotiate longer-term fixed pricing and expanded usage across the claims operation, particularly if analytical insights have identified exposure to rising labor and raw-material costs under the networks’ influence.

Now may be a good time to accelerate innovative loss prevention capabilities through in-home Internet of Things applications, automotive telematics (such as vehicle tracking), and workplace monitoring (see New Potential and Opportunity of Telematics in Car Insurance).

Data and analytics can help ensure targeted risk-engineering inspection for large commercial properties with accident risk, while satellite imagery can be used to observe abutting brush and debris cheaply and effectively across the personal lines property portfolio, preempting fire risk. Auto telematic applications, already used effectively for pricing, can also provide coaching, disable phone use, and manage driver drowsiness.

Chief financial officer

The CFO’s key task is to emphasize discipline in expense management, ensuring visibility into productivity and allocating direct investment where the greatest improvements can be achieved.

The unique role the CFO can play is to guide the enterprise on balancing growth and profitability as inflation and mitigation levers take hold across the portfolio.

Across the value chain, insurers can further manage expenses and exposure to wage inflation by reassessing service levels and expanding adoption of self-service, especially as customers increasingly show a preference for digital tools. In parallel, the CFO, in partnership with the chief actuary, should continuously reassess appetite for reinsurance and capital allocation as the portfolio and market evolve.

In sustained severe conditions, offshoring certain labor-intensive operations to stable markets may be on the table for consideration. Market volatility will favor CFOs who are nimble, responsive, and well-prepared.

………………

AUTHORS: Kia Javanmardian – senior partner in McKinsey’s Chicago office, Sebastian Kohls – associate partner in McKinsey’s New York office, Gavin McPhail – senior expert in McKinsey’s Boston office, Fritz Nauck – senior partner in McKinsey’s Charlotte office