Overview

The reinsurance industry faces numerous challenges, including geopolitical and economic outlook uncertainty, but its most significant threat is losing relevance. 2024-2025 has been another years marked by volatility, beginning with the Noto earthquake in Japan and the loss of a Japan Airlines Airbus 350.

Other notable events include the collapse of the Baltimore Bridge in March, historic flooding in Dubai in April, and the CrowdStrike/Windows global outage in July, according to Aon’s Global Catastrophe Recap.

Such losses reinforce recurrent, yet critical, themes for the industry – the growing interconnectivity and complexity of risk, volatility of losses, and the widening gap between insured and economic losses.

The Baltimore Bridge collapse serves as an example of cross-class impact, while the CrowdStrike outage illustrates the interconnected nature of software supply chains and the risks of accumulation.

Building a sustainable reinsurance market

Against this backdrop, the reinsurance industry has, however, enjoyed exceptional results over the past 18 months.

At a time of above average natural catastrophe losses, as the first half of 2024 insured losses reached $58 bn, well above the first half decadal average of $47 bn, reinsurers achieved an average common return on equity of 17.6% in the first half of 2024.

Some of the industry’s largest reinsurers reported a ROE of more than 25.0% – well above most primary insurers.

These results show a clear performance insurance gap between reinsurers and certain insurance industry segments. Structural changes in 2023 property cat programs, such as higher retentions and reduced capacity for frequency covers, led to an uneven distribution of underwriting profit across the insurance value chain.

U.S. insurers, in particular, have raised net retention levels and absorbed most catastrophe losses over the last 18 months.

Severe convective storms, now mostly retained by insurers, made up about 75% of global insured natural catastrophe losses in the first half of 2024 and 59% in 2023.

Renewals in 2024 saw pricing ease gradually, with reductions for the best-performing risks. Pricing competition is expected to expand into 2025, offering more flexibility. However, insurers require more from reinsurers than just better pricing.

Reinsurers must actively help insurers manage frequency losses and earnings volatility to deliver real value. If reinsurers avoid this risk, insurers will follow, weakening the relevance of reinsurers in risk transfer.

Reinsurance industry faces challenges

The reinsurance industry must either seize opportunities in a changing risk landscape or withdraw, allowing more risk to be retained or moved to the public sector and capital markets.

31% ($118 bn) of economic losses $380 bn caused by natural catastrophes in 2023 were covered by insurance, highlighting the opportunity for (re)insurers to play a larger role in supporting economic resilience around the globe by growing into new markets and expanding risk appetites for existing products.

Last year, the Turkey and Syria earthquake, floods in China and Hurricane Otis all generated substantial uninsured damage, costs which often had to be covered by local governments. In the U.S., the total number of policies written by Florida’s insurer of last resort, Citizens Property Insurance Corp, has doubled over the past two years. In Europe, recent storms and floods have sparked a debate on insurance penetration and public private partnerships.

Growing protection gap in the commercial insurance sector

Equally as concerning is the growing protection gap in the commercial sector. Aon has seen a 43% rise in premiums written by captives under our management in the past three years, while a quarter of respondents to Aon’s latest Global Risk Management Survey now use a captive (up from 17% in 2021).

Cyber premiums written by captives increased 58% from 2022 to 2023 alone, while captives writing environmental liability grew by 114% in 2023, with the majority coming from the natural resources industry.

As risk continues to grow and evolve, we face the real threat of becoming less relevant to our customers. The vast majority of the Top 10 risks in Aon’s Global Risk Management Survey are either uninsurable or only partly insurable today, reflecting the increase in intangible assets and risks associated with growing interdependencies and concentrations of risks.

With its historical product and physical-damage orientated approach, the (re)insurance industry must get a better handle on intangible assets and interconnectivity to stay relevant and develop new products or markets to meet its customers’ needs going forward.

Reinsurers are well positioned for a growth mindset

Reinsurers are well positioned for a growth mindset with excess capacity in the market following strong returns since the start of 2023. Reinsurer capital stood at $695 bn at June 30, 2024, up $25 bn from year-end 2023.

With robust underwriting results, improved total investment yields and ongoing interest from ILS investors – capital is forecast to continue building into 2025. The question now, is what to do with that capital.

As an industry, we need to invest for the future. Currently, we do not invest enough in research and development to develop new products and market. Investing in the right tools, talent and product development is key to staying relevant as an industry.

We need to adopt a growth mindset, with a long-term strategic plan, and based on deeper collaboration.

Caution over emerging risks is understandable, but a collective effort, without the fear of failure, will enable product and service innovation.

Reinsurance industry is at a critical juncture

Aon believe the (re)insurance industry is at a critical juncture. Now on a more financial solid footing, reinsurers must deepen their partnerships with insurers, use their capital to create a more sustainable market and lean-in to a changing risk landscape.

“If we support commercial business and unmet consumer risks, these customers will retain less which helps the industry remain relevant”.

We look forward to working with reinsurers to support our clients’ evolving needs, and build a more sustainable, and growing, market.

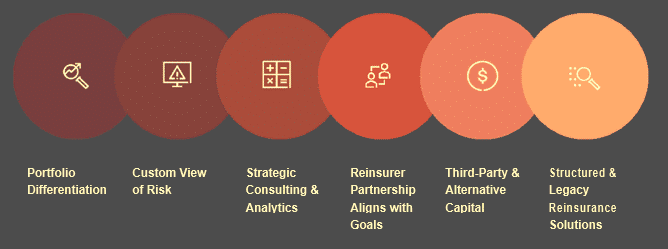

Aon continues to publish a list of top tips for insurers to achieve a successful renewal and make better decisions for profitable growth.

- Differentiate your portfolio by clearly articulating your pricing and underwriting strategies and the resulting impact on your risk profile.

- Develop a custom view of risk to better understand and mange exposure concentrations and grow profitably, improve your understanding of secondary perils and emerging risks, and optimize your placement strategy.

- Leverage strategic consulting and analytics to refine your risk appetite, adjust investment and underwriting strategies, or review business lines to drive profitable growth.

- Identify and develop relationships with your core reinsurers to build a partnership that supports and aligns with your objectives and goals.

- Consider third-party and alternative capital for optimal placement results.

- Explore structured reinsurance covers and legacy reinsurance solutions to manage volatility and free up capital to support growth opportunities.

Full Year Outlook for Reinsurance Market

Two-thirds of the way through 2024, the reinsurance sector remains on course to produce very strong results for the second consecutive year.

Capital is building quickly from already very strong risk-adjusted levels, with a further tailwind to come from mark-to-market gains on fixed-income securities, as central banks act to bring down interest rates.

These are clear signals that significantly more reinsurance capacity will be available going into the 2025 renewals, absent very large catastrophe losses between now and the year-end.

For this reason, the Atlantic hurricane season is being very closely watched, particularly as prevailing conditions have resulted in expectations of much higher than usual levels of tropical storm formation.

Based on second quarter earnings commentary, most reinsurers are targeting further growth in property business and short-tail specialty lines at forthcoming renewals.

Further increases in demand for property reinsurance will likely absorb some of the additional supply, but an easing of underwriting conditions should still be expected if primary peril losses remain benign.

Caution prevails in the casualty sector, although some reinsurers with less exposure to emerging reserving issues are sensing opportunities to grow, particularly if primary pricing continues to pick-up.

Aon believes the reinsurance market is now positioned to display greater flexibility in support of unmet client need, which in turn will boost the sector’s relevance and help to secure long-term growth.

…………….

AUTHOR: Rupert Moore – CEO of UK Reinsurance Solutions Aon