Overview

For Bermuda-based (re)insurers, underwriting results are expected to deteriorate in 2025 as premium rates are pressured and loss costs increase, although strong returns should continue as capital remains robust, according to Fitch Ratings. Beinsure analyzed the Fitch’s report and highlighted the key points.

Bermuda (re)insurers will continue to produce favorable returns in 2025 as underwriting discipline is maintained, although the market pricing cycle is past its peak.

The combined ratio will approximate 90% for full-year 2024, which is an increase from 86.5% in 2023.

5 Key Highlights

- Underwriting Pressure: Combined ratio to reach 90% in 2024, driven by higher catastrophe losses and softening premium rates.

- Cycle Peak Passed: January 2025 renewals confirm that reinsurance pricing has stabilized, with conditions expected to soften further by midyear.

- Strong Capital Base: Shareholders’ equity rose 18% in 2024 due to underwriting gains and market returns, supporting continued resilience.

- Cat Bond Growth: Catastrophe bond issuance hit $17.7 bn in 2024, reflecting strong investor appetite and favorable returns.

- Neutral Outlook: Despite lower margins, Fitch maintains a ‘neutral’ sector outlook, supported by stable capital and risk-adjusted returns.

Catastrophe losses will represent 7-8 percentage points on the 2024 combined ratio, up from 3.2 points in 2023 (see TOP 20 Reinsurance Companies in Bermuda 2025).

Reinsurance Market Cycle is Past its Peak

The January 2025 reinsurance renewal demonstrated that the reinsurance market cycle is past its peak, with stable to softening pricing as increased supply was more than adequate to meet higher demand.

Fitch expects market conditions to soften further at the 2025 midyear renewals, although risk-adjusted returns will remain favorable as underwriting discipline is maintained.

Shareholders’ equity grew 18% at 2024 from 2023 due to underwriting gains, solid investment income, and equity and bond market gains, partially offset by an increased return of capital to shareholders.

Global reinsurers’ profitability will remain strong in 2025 despite lower risk-adjusted prices for most business lines when reinsurance contracts were renewed on 1 January

ROAE will be favorable in 2024 at near 18%, although down from the superb 25.4% in 2023.

The Bermuda Re/Insurance Market Losses

The Bermuda market will have a meaningful share of insured losses from the recent California wildfires for both primary business and reinsurance.

However, we do not expect ratings to be affected given plentiful capital levels.

The potential impact on reinsurance renewal pricing from the fires will depend on the ultimate level of loss and the remoteness of such an event relative to catastrophe loss expectations.

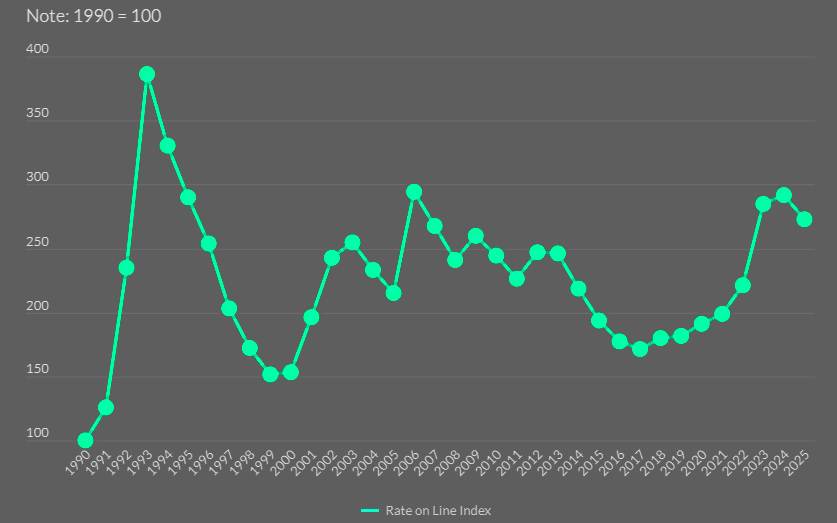

Guy Carpenter & Company’s Global Property Catastrophe Reinsurance Rate on Line Index declined 6.6% at the January 2025 renewals.

This is the first annual decline in the index since 2017, following a 71% increase from January 2017 to 2024. As a result, the index remains favorable, just below the level reached after the pricing reset in January 2023.

Global Property Casualty Rate on Line Index

Alternative Reinsurance Capital and Capacity

Barring significant losses, the ILS market is anticipated to be resilient over the near term. However, emerging risks, such as cyber, may grow but will lack meaningful participation until confidence in modeling these threats improves.

ILS capital support remained very strong in 2024.

Increased alternative reinsurance capacity reflected the exceptionally favorable rate environment for property catastrophe risks in 2024, following the significant price correction in the prior year and the corresponding attractive expected returns available in the market.

Catastrophe bond returns were particularly strong in 2024, with investors benefiting from attractive yields on recently issued transactions and the generally higher positioning of the catastrophe bonds in cedent catastrophe reinsurance towers.

Limited recent loss activity for catastrophe bonds with per occurrence triggers reflects the generally remote attachment points used in the market.

However, ILS capacity supporting aggregate reinsurance has come under pressure from heightened severe storm activity in the U.S. and, more recently, wildfires in California.

The lower prices reflect an abundance of capital, with the reinsurance cycle now past its peak, but market conditions remain supportive of strong risk-adjusted returns.

Fitch expects combined ratios to hover around 90% in 2025 and the sector return on equity to fall slightly to 17% from 19% in 2024. The sector outlook remains ‘neutral’.

Cat Bond Issuance

Catastrophe bond issuance hit a new annual record of $17.7 bn in 2024, marking the second straight year of growth.

The increase of over $1 bn from 2023 came from strong activity in the first half and a surge in the final quarter, offsetting a quiet Q3-Q4.

According to Appleby’s Bermuda office, activity in early 2025 already shows no sign of slowing. Most cat bond tranches issued in late 2024 upsized during marketing.

Many priced down from midpoint guidance, in some cases by as much as 20%. This indicates strong investor appetite and favourable execution for sponsors.

The market is flooded, but there are better investors ready to buy. Issuers are cutting prices, and investors keep accepting them. It’s a steady cycle of supply and demand.

While a few deals missed execution in early 2024, Adderley said pricing remains rational. Cat bond funds have grown into major ILS players, and they track every deal.

In addition to cat bond growth, analyst anticipates more activity in new life reinsurer formations and sidecars. He expects several new structures and entities to launch in early 2025.

FAQ

Yes. Despite underwriting pressures, profitability remains solid due to strong investment income and disciplined risk selection.

Underwriting results are expected to weaken slightly. The 2024 combined ratio will rise to about 90%, up from 86.5% in 2023.

No. The cycle has passed its peak. January 2025 renewals show stable to softening pricing driven by increased capital supply.

Bermuda-based companies are exposed to California wildfire losses, but Fitch does not expect ratings to be affected due to strong capital levels.

Catastrophe bond issuance reached a record $17.7 bn in 2024. Investor demand remains high, and pricing continues to decline due to excess capital.

ROE will decline slightly to 17% in 2025 from 19% in 2024 but remains strong by historical standards.

Not significantly in the near term. Modeling uncertainty continues to limit meaningful capital allocation to cyber exposures.

………………..

AUTHORS: Brian C. Schneider, CPA, CPCU, ARe – Senior Director at Fitch Ratings (Chicago), Laura Kaster, CFA – Senior Director, Risk for North and South American Financial Institutions, Credit Commentary & Research at Fitch Ratings, Brad Adderley – Bermuda Managing Partner at Appleby