Overview

Swiss Re forecast global real GDP growth (inflation adjusted) of 2.5% in 2026 and 2.6% in 2027, with US outperformance relative to other advanced economies narrowing as the labour market cools and policy uncertainty lingers.

Analysts expect global GDP growth to slow to 2.3% in 2025, down from 2.8% in 2024.

Global growth is slowing at a time of large macroeconomic regime shifts. Extreme policy uncertainty is set to persist, the main driver being US goods tariffs.

Trade wars and protectionism leave no winners, but over the longer term will relocate trade and production globally.

Firms and consumers face greater risks, including more volatile exchange rates and asset prices, heightened further by new developments in the Middle East conflict, Beinsure noted.

Key highlights

- Swiss Re forecasts global real GDP growth of 2.5% in 2026 and 2.6% in 2027, with US outperformance fading as the labour market softens and policy uncertainty sticks. Beinsure analysts note that global GDP growth slows to 2.3% in 2025, down from 2.8% in 2024.

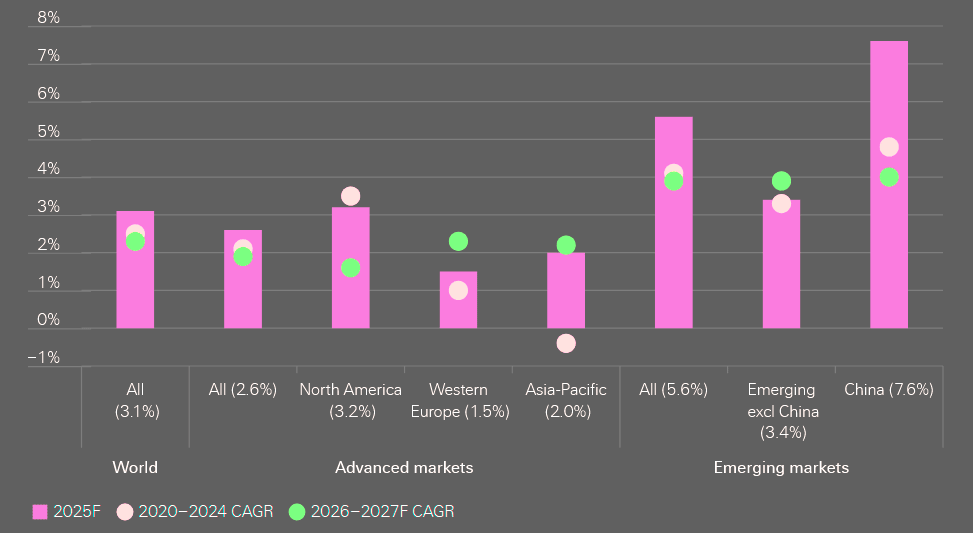

- Global insurance premium growth, life plus non-life, is expected to average 2.3% in real terms in 2026–2027, below the 2.5% CAGR of the past five years. After a strong 2024, momentum clearly cools.

- Swiss Re expects global non-life premiums to rise 1.7% in real terms next year and about 2.5% in 2027. Trade-exposed lines such as marine, trade credit, and construction feel the slowdown first.

- Global life premium growth should average about 2.3% over the next two years, supported by demand above pre-pandemic levels and structurally higher long-dated bond yields.

- Peak-year global insured losses could exceed $300 bn, driven mainly by primary perils like hurricanes and earthquakes. Swiss Re says these peak years should be expected, not treated as outliers.

According to BlackRock Investment Outlook, the Great Moderation, a period of steady growth and inflation, is over. Instead, we are braving a new world of heightened macrovolatility – and higher risk premia for both bonds and equities.

Global GDP growth outlook

| Year | Global GDP growth | Key drivers |

| 2024 | 2.8% | Post-pandemic momentum, easing financial conditions |

| 2025 | 2.3% | Tariff uncertainty, weaker trade, softer demand |

| 2026 | 2.5% | Looser fiscal stance, slower labour markets |

| 2027 | 2.6% | Stabilisation, US growth converges with peers |

Black Rock are bracing for volatility in this new regime – our first theme. Central banks are rushing to raise rates to contain inflation that’s rooted in production constraints.

They are not acknowledging the stark trade-off: crush economic growth or live with inflation. The Federal Reserve, for one, is likely to choke off the restart of economic activity – and only change course when the damage emerges. We see this driving high macro and market volatility, with short economic cycles.

Global insurance premium growth will slow

Against this growth backdrop, we estimate that global insurance premium (non-life + life) growth will slow to an average of 2.3% in real terms in 2026 and 2027, just below the 2.5% compound annual growth rate of the last five years (see 20 largest insurance markets).

Beyond 2027, we see growth stabilising at 2.3%, supported by structural drivers like rising natural catastrophe exposures and escalating liability costs in non-life.

Premium growth will likely slow as the global economy weakens, more so in trade-exposed areas such as marine and trade credit insurance, and in sectors like construction, Beinsure noted. Life insurance sees primarily indirect consequences via financial and labour markets.

Global life insurance premiums are projected to grow at an annual rate of 3% in 2025 and 2026, more than double the average growth of the past decade.

The sigma report, Growth in the Shadow of (Geo-)Politics, attributes this rise to increasing real wages, sustained high interest rates in markets like the US, ageing populations, and the expanding middle class in emerging economies. Beinsure reviewed the report and highlighted the key points.

Global insurance premium growth outlook

| Segment | 2025 | 2026 | 2027 |

| Total insurance (life + non-life) | 2.0% | 2.3% | 2.3% |

| Non-life insurance | 1.8% | 1.7% | 2.5% |

| Life insurance | 2.3% | 2.3% | 2.3% |

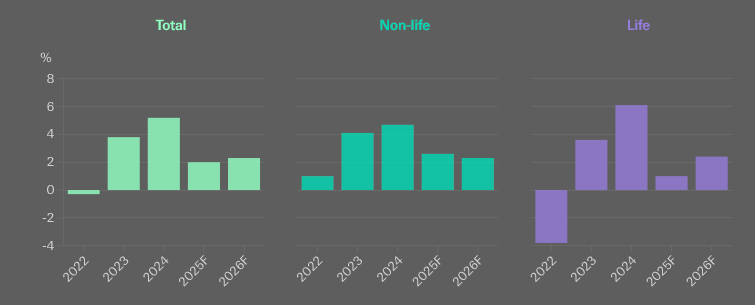

After a strong showing in 2024, premium growth in the world’s insurance industry is slowing on both the non-life and life sides, impacted by the global economy and unstable policy environment.

We estimate that total premiums (life and non-life) will grow by 2% in real terms in 2025 (vs 5.2% in 2024), with marginal pick-up to 2.3% in 2026.

Swiss Re expects global non-life insurance premiums to grow by 1.7% in real terms next year, before edging up to about 2.5% in 2027.

Earnings momentum cools, but strong investment yields should soften the slowdown. That income matters more now than it did five years ago.

Global total insurance premium real growth rates by regions

Life insurance tells a steadier story

Swiss Re sees global life premium growth averaging roughly 2.3% over the next two years as demand settles above pre-pandemic levels.

Industrial policy is rewriting the economic playbook – AI is accelerating, growth looks strong, but the credit cycle will reveal how solid it really is.

Jerome Jean Haegeli, Group Chief Economist

Long-dated bond yields remain structurally higher, and that backdrop gives insurers room to support profitability even as top-line growth evens out.

Key pressures by insurance line

| Area | Primary impact | Commentary |

| Non-life – motor | Higher claims severity | Tariffs raise repair and replacement costs |

| Non-life – construction | Cost inflation | Materials and labour volatility |

| Marine & trade credit | Slower premium growth | Trade exposure, weaker volumes |

| Life insurance | Indirect pressure | Linked to labour and financial markets |

| Long-tail casualty | Reserve strain | Inflation, litigation, slower repricing |

Real premium growth, total, non-life and life insurance

Populations are ageing, the ratio of working-age persons to total is shrinking, and household structures are changing, with more single-dwelling and no-child households. These demographic shifts are rebalancing the underlying triggers of demand for life insurance.

Over the longer term, the demographic changes will likely see growth for traditional life insurance products slow relative to that for retirement income, financial management and longevity solutions.

To meet the needs of ageing populations and people living longer lives, insurers will need to shift their focus from the accumulation phase of consumers’ lifespans to the decumulation phase, Beinsure stated.

Longevity products will benefit from the trend shift to defined-contribution pension models from defined benefit plans. As guaranteed-income retirement plans phase out, life insurers can move risks previously on corporate balance sheets to their own.

Demand for long-term care (LTC) solutions should also grow as populations age and people live longer lives.

Beyond insurance premiums, the macro setting keeps shifting

A political economy that leans harder on industrial policy is taking shape and it isn’t subtle.

Fiscal and monetary policy look looser as well, a mix that may buffer global growth against trade tariffs, but also leaves the door open to renewed inflation pressure. Maybe more than markets expect.

The impact of the Silver Economy on insurers will accelerate, leading to a new phase of innovation. We are seeing a generation that is larger, living longer, and arriving at retirement wealthier than we have seen before.

Paul Murray,CEO Swiss Re Life & Health Reinsurance

Those shifts land directly on insurance balance sheets. Elevated inflation eats into real incomes and household savings, shrinking demand in real terms.

Structural regime shifts affecting insurers

| Regime shift | Direction | Insurance impact |

| Industrial policy | Expanding | Alters capital allocation and risk pricing |

| Fiscal & monetary stance | Looser | Supports growth, risks inflation |

| Geoeconomic fragmentation | Rising | Smaller risk pools, higher costs |

| Policy uncertainty | Persistent | Delays investment, weakens demand |

US tariffs impact the insurance industry

Global growth is decelerating as US tariff policy reduces trade and heightens uncertainty. Consumers and firms have likely already begun cutting spending and investments in response to the uncertainty, which may not be fully visible in the economic data yet.

US tariffs impact the insurance industry through premium growth, claims and investment returns, with differing effects by geography.

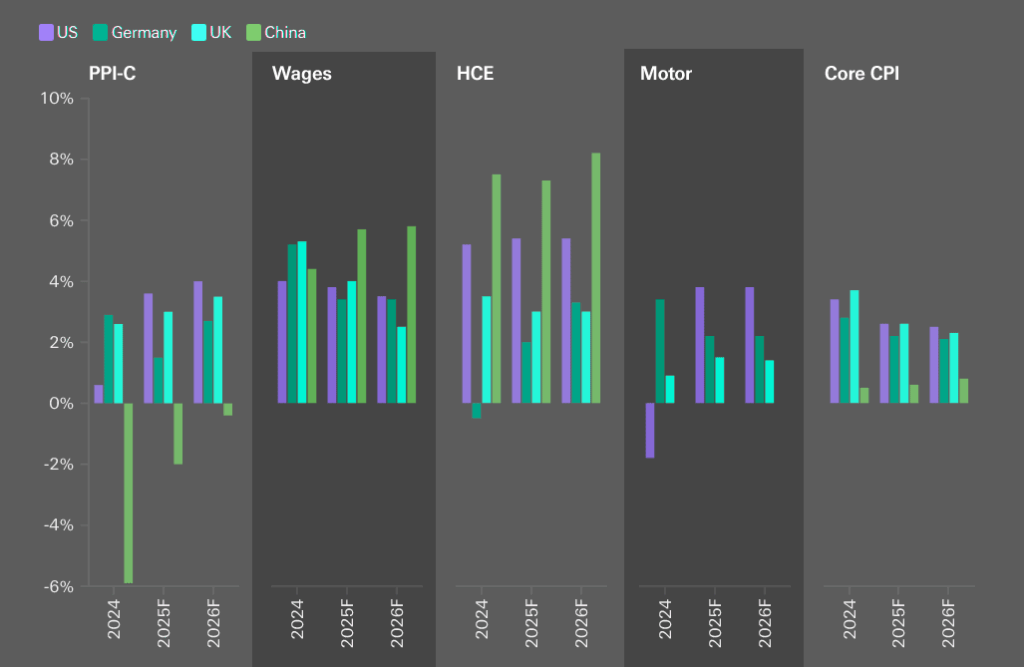

We see the greatest and most direct impact on non-life claims severity in the US, most notably in US motor and construction.

Outside the US, tariffs are more likely to be disinflationary, reducing pressure on claims.

CPI inflation by market and sub-category, year-on-year

According to Beinsure, that squeeze shows up fastest in long-tail lines. Geoeconomic and financial fragmentation adds another layer.

Systems are breaking into blocs, slowly but visibly, and insurers must operate inside that reality.

Insurers feel it through eroding premium value, pressured reserves, and higher claims costs that don’t politely wait for repricing cycles.

Fragmentation raises costs, narrows risk pools, and limits diversification options that once felt routine. Insurance still works, but the math gets tighter, and the margin for error shrinks.

Demographic trends and life insurance implications

| Demographic trend | Change | Insurance consequence |

| Ageing populations | Accelerating | Higher demand for retirement income |

| Lower birth rates | Structural | Slower growth in traditional life |

| Longer life expectancy | Rising | Growth in longevity products |

| Shift to DC pensions | Ongoing | Risk moves from corporates to insurers |

| LTC demand | Increasing | Product expansion opportunity |

Global insured losses

Global insured losses could exceed $300 bn in a peak year, underscoring the essential role of the reinsurance sector, which holds $500 bn in capital, in absorbing large-scale shocks.

While secondary perils continue to generate significant losses, Swiss Re’s latest report emphasizes that primary perils (such as hurricanes and earthquakes) remain the largest threat, with the potential to drive peak-year losses above $300 bn.

The firm noted that such years, whether caused by a few major events or a combination of primary and secondary perils, should not be seen as rare.

Global insured loss outlook

| Metric | Estimate |

| Peak-year insured losses | $300 bn |

| Reinsurance sector capital | $500 bn |

| Largest loss drivers | Hurricanes, earthquakes |

| Secondary peril trend | $50 bn annually |

| Frequency of peak years | No longer rare |

Swiss Re cited 2017, when Hurricanes Harvey, Irma, and Maria struck, as the most recent peak year. Since then, increasing exposure due to economic expansion, population growth, and urban development has raised underlying risk levels (see how Natural Catastrophes Drive Record-High Economic and Insured Losses).

Climate change has further compounded loss potential in specific regions and weather-related perils.

Swiss Re said internal analysis of over 200 models and loss data from the past 30 years shows the scale of risk. A severe hurricane or major earthquake impacting a densely populated area with high insurance penetration could generate insured losses of $300 bn in a single year.

FAQ

Swiss Re points to large macro regime shifts, persistent policy uncertainty, and US goods tariffs. Trade friction weighs on investment and spending, even before it shows up cleanly in headline data.

Protectionism raises volatility in exchange rates, asset prices, and supply chains. According to Beinsure, insurers feel it through weaker premium growth, higher claims costs, and more fragile diversification benefits.

Total real premium growth slows to about 2% in 2025, then stabilises around 2.3% in 2026–2027. That’s still growth, just thinner than the post-pandemic rebound.

Non-life lines tied to trade and physical goods suffer most. US motor and construction face higher claims severity, while outside the US tariffs may even have a disinflationary effect on claims.

Life insurance reacts indirectly through financial markets and employment rather than immediate claims inflation. Higher bond yields support margins, even as top-line growth evens out.

Ageing populations, fewer children, and longer life expectancy shift demand away from pure accumulation products toward retirement income, longevity, and long-term care solutions.

Economic growth, urbanisation, higher insurance penetration, and climate-driven weather volatility all push losses higher. Swiss Re’s modelling shows a single major hurricane or earthquake in a dense area can now generate $300 bn in insured losses.

AUTHORS: Jerome Jean Haegeli – Group Chief Economist, Head of Swiss Re Institute, Charlotte Mueller – European Chief Economist of Swiss Re Institute

Edited by Yana Keller – Editor at Beinsure Media