Overview

During past year, the world saw another year of impactful natural catastrophe events that once again emphasized the need to better account for the growing risks that these hazards bring, according to Gallagher Re Natural Catastrophe Report.

The increase in severity and in some cases frequency of events – particularly when focusing on secondary perils – presents reinsurers with a multifaceted and complicated challenge when it comes to risk protection and mitigation.

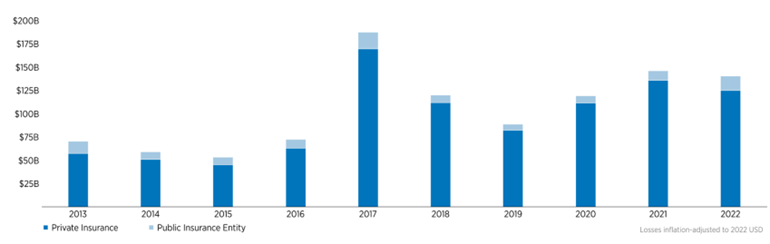

2025 became the fifth year since 2018 to cross the $100bn threshold. Total insured losses were estimated at $140bn, of which $125bn was covered by private insurers and $15bn by public insurance entities (US National Flood Insurance Program).

Analytics summarize the major catastrophe events that occurred in each region around the globe in 2022-2025, detailing the financial loss, fatalities, and other major considerations for our clients and beyond. A summary of major global events can be found in the appendix. All data estimates are from Gallagher Re, unless stated otherwise.

This report also aims to help readers give greater thought to how topics such as climate change, inflation and social inflation, and the macroeconomic environment are driving new and emerging types of risk. The risk profile faced by the private sector, governmental entities and beyond continues to evolve as new challenges arise.

Global natural catastrophe overview

2022 was a year marked by costly, consequential and historic natural catastrophe events around the world. The estimated economic cost of natural hazards was listed at $360bn. Private and public insurance entities covered $140bn, meaning 61% of global disaster losses were not covered by insurance, demonstrating the protection gap.

Natural hazard mitigation and adaptation needs amplify as annual cat losses show continued growth

It was also another year where climate change, exposure growth and social inflation were the clear primary driving forces of loss.

The fingerprints of climate change were visible on virtually every major weather and climate event in 2024, once again highlighting the urgency to implement proper planning and investment strategies that will limit the risk to life and property.

How we collectively bring together financial institutions (insurance, asset managers, real estate, banking), governmental entities, academia, and emergency management to identify risk and implement actionable plans to improve our resilience, mitigation, and adaptation readiness will have hugely positive impacts on trying to slow the rate of annual catastrophe loss growth.

US Dominates Loss Costs

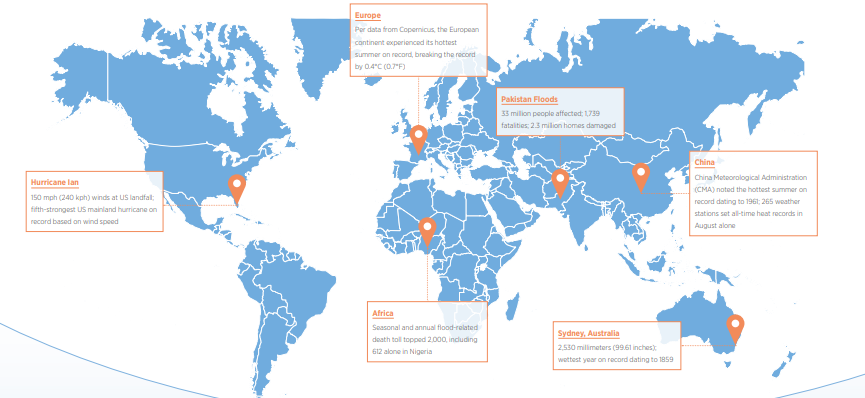

The US endured several large-scale and impactful events, led by Hurricane Ian. The storm was poised to result in at least $55bn loss for public and private insurance entities, and an overall economic loss of $112bn in the US alone. This marked one of the costliest natural disaster events ever recorded globally.

The country also endured a prolific drought that was expected to result in $9bn in indemnity payouts via the United States Department of Agriculture (USDA) Risk Management Agency (RMA) crop insurance program.

At least three Severe Convective Storm (SCS) outbreaks resulted in a multibillion-dollar insured loss, with 2023 marking the 15th consecutive year with aggregate insured SCS losses topping $10bn and the 8th year since 2010 that such losses have topped $20bn.

A prolific late December winter storm and extreme cold snap led to significant societal disruption via power outages and impacted crops across a huge swath of the lower 48 states. This put a further spotlight on losses associated with secondary perils.

Historic and Consequential Global Events

The costliest event and one of the most consequential from a humanitarian perspective outside the US was the prolific seasonal monsoon flooding in Pakistan. A report from the World Bank cited a $15bn direct physical damage economic loss, while the country’s National Disaster Management Authority cited 1,739 fatalities, 2.3 million homes damaged and 33 million people affected across 90 districts.

According to Natural Catastrophe Insight: Economic & Insured Losses, historic flooding also impacted several regions of Africa, notably in Nigeria where the country’s insurance industry faced its most expensive natural catastrophe on record.

The effects of a third consecutive La Niña occurrence were quite pronounced in Australia: the Insurance Council of Australia stated weather-related events had resulted in nearly $5bn in payouts alone, primarily from a historic flood event in late February and March.

Other notable events included a series of record summer heat waves in Europe that led to excess mortality totals into the tens of thousands; a powerful March offshore earthquake in Japan; record-setting SCS activity in France; extensive drought conditions across South America, Europe and parts of Asia; typhoon landfalls in Japan and the Philippines; Hurricane Fiona landfalls in Puerto Rico and Canada; multiple strong European windstorm vents to wrap the 2021–2022 season; and an intense May derecho in Canada.

Role of Climate Change

The implications of climate change on daily weather and climate events continues to become better understood. However, it remains a lengthy journey in defining how confident we are in our comprehension of what climate change will look like in its influence on individual events.

New research from the academic realm has further identified how climate change is affecting the behavior of individual events, but it is not a linear interpretation. There are distinct differences on a per-peril and per-region basis.

The following graphic attempts to simplify the current confidence levels in scientific research regarding how climate change is influencing individual perils. Temperature- and precipitation-focused perils are most confidently understood, but SCSs remain at the bottom of academia’s current understanding (see Insured Natural Catastrophe Losses).

Following a year in 2022 where virtually every continent on Earth was exposed to some type of record-breaking weather or climate activity, it grows more important by the day to account for the physical and nonphysical risks posed by climate change. Such risks are no longer hypothetical. They are already here.

It is also worth mentioning that there is a growing focus from private financial industries on how to more effectively build climate change into their climate and environmental, social, and governance (CESG) strategies. With the regulatory market around the world putting more emphasis on climate-related financial disclosures or rating agencies beginning to score companies based on their CESG performance, there is a growing need for financial firms to meet the growing demands on portfolio decarbonization and carbon accounting.

Global Natural Hazard: Notable Statistics

Global Natural Catastrophe Event Summary

2024 was a year marked by one exceptionally large catastrophic loss event and many moderately large events that aggregated to high economic and insured loss totals (Global catastrophes economic losses estimated of $270 bn).

Highlighting the enormity of the event, Hurricane Ian’s economic and insured losses represented 32% and 39%, respectively, of the globe’s entire annual total.

The following table highlights the 11 events that resulted in a multibillion-dollar insured loss.

Natural Catastrophe Event Summary

| ~50,000 | $360bn | $140bn |

| Estimated Fatalities | Economic Loss | Insured Loss |

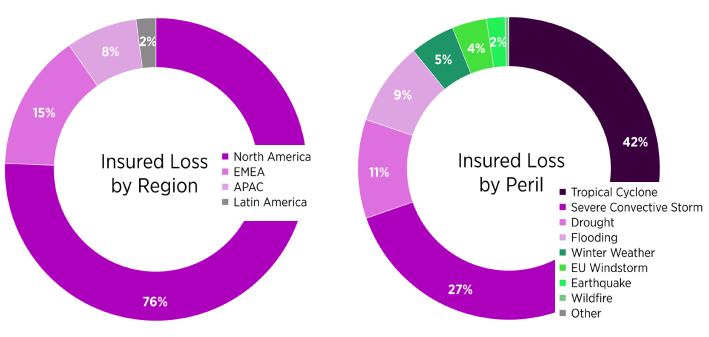

The topic of primary versus secondary perils has taken on heightened significance in recent years as these so-called secondary perils—marked by higher-frequency/lower-cost events—have shown accelerating loss growth and often aggregate to higher annual totals. Secondary perils were again the most expensive on an economic basis and exceeded those on the insured loss side.

- Primary perils (Economic/Insured): $149bn (41%)/$67bn (48%)

- Secondary perils (Economic/Insured): $211bn (59%)/$73bn (52%)

The last 10 years of global insured losses index to today’s dollars

The US accounted for 53% of global economic losses and 74% of insured losses. The country boasts the most robust insurance market in the world and it is typically the predominant annual driver in insured losses given its regular frequency of high-dollar catastrophe events.

Additional year-end natural catastrophe statistics include:

- Top three costliest perils (economic): tropical cyclone($130bn); drought ($77bn); flood ($65bn)

- Top three costliest perils (insured): tropical cyclone($59bn); SCS ($39bn); drought ($15bn)

- Billion-dollar natural catastrophe events (economic): 43 (all)/42 (weather only)

- Billion-dollar natural catastrophe events (insured): 20 (all)/19 (weather only)

The main drivers of large weather events were multi-faceted. The most important influencing factor on the year’s weather events came from a prolonged La Niña cycle that brought more intense flooding and drought conditions to many parts of the world.

A regional and peril breakout of global insured losses

As the year ended, La Niña conditions remained active, and it was forecast to extend into a third consecutive annual cycle through the 2023 before transitioning to ENSO-neutral and possibly to El Niño later in 2023.

Natural catastrophe summaries by region

US/Americas

The largest insured loss from a single event came from September’s landfall of Hurricane Ian. The estimated $55bn in wind- and water-/flood-related losses that were prolific across the state of Florida.

Ian ranked as the second-costliest natural hazard event on record regardless of peril from an insurance perspective. The only other hurricane to make landfall during the 2024 Atlantic hurricane season was Hurricane Fiona.

That storm led to catastrophic flooding in Puerto Rico before tracking northward and striking the Canadian Maritimes as a strong extratropical cyclone. Overall, the Atlantic hurricane season was near-average, with 14 named storms, eight hurricanes and two major hurricanes (Category 3+).

SCS events were again considerable in the US and Canada. There were at least seven SCS outbreaks (six in the US and one in Canada) resulted in at least $1bn in insured losses. A significant portion of the losses were due to large hail and damaging winds (including multiple North American derechos).

Data from NOAA showed that the US preliminarily recorded roughly 1,200 tornadoes in 2022—a near-normal tally—though a March record of 236 tornadoes occurred. Exceptional drought conditions continued to affect large swaths of North and South America. Total combined economic losses were estimated in excess of $43bn, mostly in the US and Brazil. Extreme winter weather engulfed the US and Canada in late December.

EMEA

Several major weather catastrophes affected the European continent, though the most deadly arose from a series of intense heat waves in June, July and August that led to tens of thousands of fatalities.

The three months marked the hottest summer ever recorded for Europe and exacerbated major drought conditions that led to widespread agricultural impacts.

The year originally saw a series of windstorms in February (Dudley/Ylenia, Eunice/Zeynep, Franklin/Antonia) that resulted in $4.3bn in insured losses.

The full 2023 calendar year saw European windstorm loss exceed $5bn for insurers. During the summer months, significant and highly damaging hailstorms resulted in more than $5bn in insured losses from more than one million filed claims in France alone.

Record-breaking flooding swept across several regions of Africa and resulted in at least 2,000 fatalities. Historic flood-related insurance losses were generated in Nigeria and South Africa. On the opposite extreme, the worst drought in decades left more than 30 million people facing food insecurity challenges in the Horn of Africa.

APAC

Historic flooding in Pakistan led to $15bn in direct physical damage, with additional losses to GDP estimated at another $15bn and a societal disruption to 33 million people.

Extremely limited insurance takeup meant most damage was uninsured. Flooding also led to billions (USD) in damage across parts of India, China, South Korea and Thailand.

A subdued Western North Pacific typhoon season saw manageable damage impacts. The most notable were Nanmadol and Talas in Japan, Hinnamnor in South Korea, and Nalgae in the Philippines. The continent’s costliest non-weather disaster was an offshore Japan earthquake on March 16 that led to an estimated $8.5bn in economic damage.

Australia weathered the impacts of La Niña bringing incessant rainfall to the country’s east coast. One prolific event in late February and March led to an estimated $4.0bn in insured losses across parts of New South Wales and Queensland.

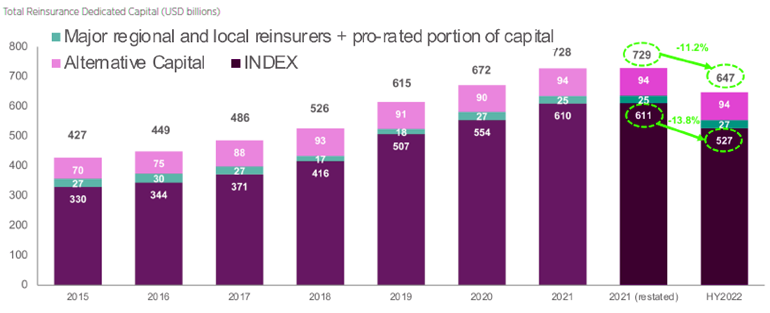

The Capital Challenge in Natural Catastrophe

While there was sufficient capacity to meet the reinsurance needs of cedants at 1.1, it is also true that the amount of reinsurance capital being deployed was diminished in 2023. Cedants were, by and large, able to secure their required limit, but it came at a price.

There was a clear desire from reinsurers to force change onto the market at the most recent renewals: pushing retentions up and restructuring programs to improve profitability for 2024 and beyond.

Total annual reinsurance capital

While Gallagher Re does not have data detailing the capital allocation to natural catastrophe coverage, our einsurance market report, published twice a year, demonstrated a clear drop in total reinsurance dedicated capital and illustrated the contribution of cat losses to the combined ratio for the subset of reinsurers which provide that disclosure.

However, the drivers of the drop in capital go beyond the runrate of losses from natural perils, and include macroeconomic factors, the impact of the reinsurance hard market, regional considerations and a greater scrutiny of models by reinsurers.

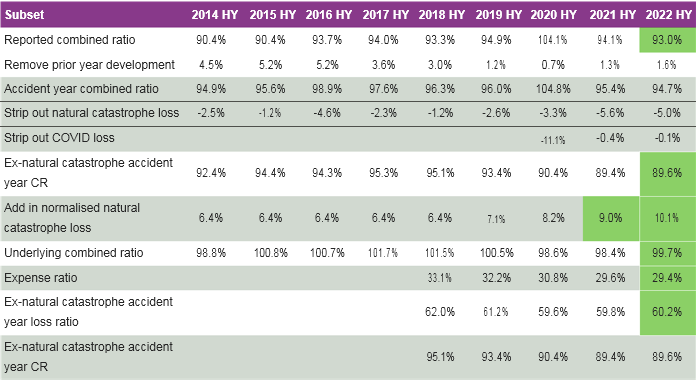

Combined Ratio for the Gallagher Re Subset

Macroeconomic Factors

Last year saw an unprecedented round of fiscal tightening in major economies, following more than a decade of low interest rates and cheap debt. Reinsurers have historically deposited much of their investment capital into investment-grade fixed-income instruments to keep volatility out of their portfolios and maintain as much liquidity as possible in case cash is needed to pay claims.

This worked well during periods of loose monetary policy, as quantitative easing and other measures kept money markets stable. But in recent months, a supply chain shock led to widespread inflation, resulting in a ramping up of interest rates.

That in turn caused a significant drop in the valuation of investment-grade bonds (particularly at the short duration end of the curve where reinsurers tend to invest), leading to a decline in available capital on a market-to-market basis.

Figures from Gallagher Re’s latest Global reinsurers’ financial results report demonstrated this, showing that for its cohort of global reinsurers, shareholders’ equity dropped by an average of 34% in the first nine months of the 2024, driven by threats of recession and the rise in interest rates, which resulted in lower market values of bonds and equities held by reinsurers.

From a solvency perspective, many reinsurers were actually better off; rising risk-free rates resulted in higher solvency ratios as the reduction in liabilities—which in Europe are discounted at risk-free rates under Solvency II—exceeded the reduction in bond portfolio values.

However, the potential liquidity risk (that reinsurers may be forced to liquidate underperforming bonds, crystallizing the loss in bond value, to pay claims in the event of a large loss event) may be enough to make carriers think twice about whether they can afford to underwrite more natural catastrophe risk in the short term.

Hard Market; Hard Choices

While the primary and retro markets were the early winners in the burgeoning hard market, by the middle of 2023 those rate rises had also fed through to reinsurance premiums.

However, increased rates on their own were not enough to result in a wave of capital being deployed—appetites were impacted by a variety of factors, including but not limited to:

- How reliant the reinsurer is on retro to underwrite (and therefore the availability of retro, which for 1.1.23 was extremely late to show its hand, but did ultimately come to the party)

- A lack of third-party capital reloading given some capital remained trapped from previous losses

- Investors had a broader set of higher returning investment classes to consider in the rising rates environment, and many were concerned about existing modeling adequacy, and the impact of climate change on event frequency and severity

- A drop in the number of ILS players fronting elements of reinsurance coverage when compared with previous years

- A reduction in appetite for lower attaching retentions, given the impact of secondary perils on results in the past few years

- Increasing level of scepticism regarding whether reinsurers’ tools can adequately evaluate and price risk for the current risk environment, something that’s exacerbated by the implications of climate change

Much also depends on the state of the individual cedants. In the US, smaller or more regional clients clearing less than $200mn of capacity broadly found coverage, so long as pricing was set at an appropriate level.

Considerably more challenging were the larger placements, particularly $500mn and above, where the broadest level of participation across the reinsurance market was required to clear capacity.

Third-party investors historically play little part in the likes of European treaties other than through some fronting deals, given the more complex nature of the multi-peril coverage and multiples. But there was even less capital deployed than normal here too, leading to a drain on capacity when compared with previous years, in particular around complex placements.

The fact that losses have come from secondary perils, unmodeled perils, COVID, etc., is particularly challenging for ILS managers who have historically sold investors on being exposed to headline risk—the results have not borne that thesis out, which has also contributed to the lack of capital inflows.

The secondary perils experience has also led traditional reinsurance capital to largely move away from providing coverage at the lower levels, rejecting 1:3 year–1:5 year event coverage and instead coming in around the 1:10 level. It is a much simpler exercise to effectively underwrite yourself out of secondary perils by requiring higher attachment points.

Solutions and Silver Linings

Despite the challenging conditions, renewals were largely completed—thanks to a combination of collaboration and innovation.

Cedants, that were able to, agreed to higher absolute retentions, and through their broker partners, some were also able to place meaningful absolute annual aggregate deductibles (AADs) on first layers in an attempt to maintain some level of earnings coverage.

In the US, clients also investigated the use of captives—particularly the idea of using a captive to sell ultimate net loss coverage to a company, and then employing a parametric hedge like an ILW/ bond/etc. to protect the captive and group results.

Looking ahead, there is consensus that more capital will flow into the market in 2023 and beyond. Even in the dying embers of 2022, companies were able to bring new capital to the property reinsurance market, and others were able to successfully complete equity raises.

Gallagher Re estimates that somewhere in the region of $1.5bn in new capacity was raised ahead of 1.1 for that renewal, although little of it was ultimately deployed, meaning there is some dry powder for the next round of negotiations.

Events such as the Floridian reforms announced at the end of 2024 will encourage more capital to play, most likely with those cedants considered best-in-class initially, as carriers dip their toes back in the water.

Ultimately, the industry has already proved that it is not a broken system, that even in the trickiest renewal many have seen in decades, deals got done; and that the market looks set to trade on into 2024.

………………….

AUTHORS: Steve Bowen, M.Sc. – Chief Science Officer Gallagher Re, Vaughn Jensen – Global Head of Catastrophe Analytics Gallagher Re, Tina Thomson, Ph.D. – Head of International Catastrophe Analytics, Gallagher Re, John E Alarcon, Ph.D., M.Sc. – Executive Director Gallagher Re, Prasad Gunturi, M.Sc.– Executive Vice President Catastrophe Analytics Gallagher Re, Brian Kerschner – Western Hemisphere Meteorologist Gallagher Re