Overview

Every insurer should closely monitor price developments, focusing on the drivers relevant to the respective insurance coverages, such as repair costs, construction prices or medical inflation.

Acording to The Geneva Association Report, naturally, insurers have to react to sustained cost increases by adjusting premiums. However, the balance of an increase in premiums on the one hand, and potential adverse selection effects on the other, must always be kept in mind. The same logic applies to reserving, especially in long-tail business. In this context, rising interest rates can mitigate selection issues by making it easier to finance long-term guarantees.

How insurers respond to inflation across the value chain

Product design should also be reviewed. Lump-sum benefits, maximum sums insured, caps and deducti-bles help to limit maximum loss exposure, while also reducing the extent of required premium adjustments (see How Does Inflation Challenging Insurer Profitability).

If insurers properly manage the challenges ahead and limit negative effects on profitability, there should be no sustained impact on market capacity and insurance supply

Digitisation and automation constitute crucial levers to counter the increase of operating costs. Substantial efficiency gains resulting from such endeav-ours can drive down cost ratios and will ultimately strengthen the resilience of our industry.

On the investment side, there are two divergent aspects. On the one hand, rising interest rates are positive regarding reinvestment yields. However, on the other hand, escalating fears of an economic recession and the geopolitical environment can substantially affect market values and volatility.

Product management

Most links of the insurance value chain lend themselves to strategic and operational responses. This analysis prepares the ground for the exploration of effects on insurance demand and supply, i.e. insurance penetration, and, ultimately, the role of insurance in society.

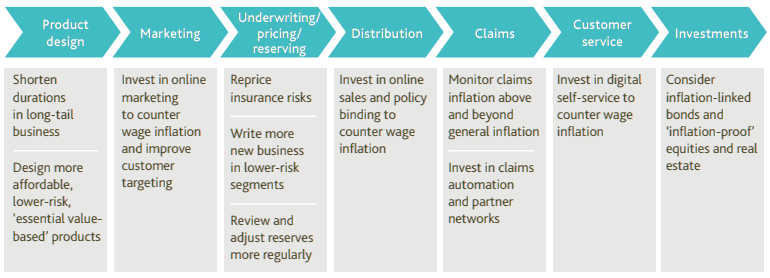

As discussed earlier, long-tail P&C business is particularly vulnerable to inflation. In this context, contract design offers ways to mitigate inflation exposure, for example by shortening the duration of liabilities or by indexing limits and deductibles.

Contract design offers ways to mitigate inflation exposure, for example by shortening the duration of liabilities or by indexing limits and deductibles

Specific measures include a shift to ‘claims-made’ policies, which only cover claims reported during the policy period regardless of the date of occurrence; sunset clauses, where the insurer will only respond to losses reported before a predeter-mined future date; and index clauses, which link premiums, limits and deductibles/retention to an inflation-related index (and would also avoid onerous repricing).

Inflation is also likely to prompt insurers to offer more lower-cost and lower-risk products with an increased focus on risk and loss prevention (e.g. through Internet of Things applications and automotive telematics) as well as usage-based propositions, which try to respond to affordability issues faced by customers, especially in a recessionary inflation environment.

Insurance Marketing

With tight labour markets and increasing wage pressure, insurers will maintain their drive to improve operational cost efficiency and overall productivity, i.e. output per employee. Digitalisation is one obvious route to achieve this objective in the marketing function.

At the same time, online digital marketing also allows for better targeting of customers, based on an enhanced understanding of their needs and the ability to offer more tailored products. In addition, digital marketing applications enable insurers to refine their pricing and make their processes faster and more customer-centric.

In times of rising general inflation, it is even more important for non-life insurers to monitor claims cost inflation above and beyond general inflation

These capabilities are likely to prove particularly beneficial in times of inflationary recessions when an increasing number of customers will more critically review the cost-benefit characteristics of their insurance policies.

Underwriting, pricing and reserving

The main underwriting response is to reprice insurance risks with elevated claims costs. The need and scope for doing so depends on the competitive environment in the relevant insurance markets, insurers’ assumptions concerning central banks’ ability to tame inflation within a reasonable period of time and the degree of public policy and regula-tory constraints and intervention.

The main underwriting response is to reprice insurance risks with elevated claims costs

However, calculated premiums do not only reflect inflation but also interest rates and expected investment income, which are rising because of monetary policy responses to inflation. In addition, insurers are likely to steer new business towards propositions with lower risk profiles and shorter durations.

At the same time, insurers could proac-tively offer increased limits to their customers in order to avoid underinsurance as a result of inflation. Last but not least, in times of inflation, insurers, especially in the P&C segment, will more frequently need to ascertain the adequacy of their technical reserves.

Insurance Distribution

As the biggest non-claims cost block in insurance, acquisition and distribution is a natural focus of corporate efficiency drives, even more so in times of wage inflation.

While traditional intermediaries, such as agents and brokers, still dominate distribution for most insurance classes around the world, an increasing amount of insurance is gradually being offered through mobile and internet channels, too, as part of omni-channel strategies.

This trend is expected to further accelerate in the face of inflation as both insurers and insureds are under increasing pressure to capture cost efficiencies.

Insurance Claims

Insurance claims costs are not only driven by general (consumer-price) inflation but also reflect specific legal, societal and scientific developments, which give rise to what is widely referred to as social inflation.

Phenomenon might be affected by increased general inflation, for example by raising individuals’ propensity to sue and affecting public attitudes to corporations and economic inequality.

Such changes could impact jury awards and settlements. Therefore, in times of rising general inflation, it is even more important for non-life insurers to monitor claims cost inflation above and beyond general inflation.

To counter claims cost inflation, insurers will place even more emphasis on boosting claims cost efficiency, for example by accelerating claims automation and straight-through processing as well as expanding (or building)partner and supplier networks in order to negotiate fixed prices for a longer period of time. Claims professionals will also sharpen their focus on claims with the longest cycle times, i.e. a high exposure to price inflation.

Insurance Customer service

In customer service as well, insurers will boost expense management discipline. At the same time, they are likely to invest in increased productivity and digital self-service, especially as customers grow more familiar with and expectant of digital tools for interaction and service transaction completion (see 2023 New Customer & Technology Trends in the Changing Insurance).

Asset management

In general, effective insurer responses to inflation would have to occur preventively, rather than ex-post. Once inflation has picked up, the value of inflation-linked securities and the level of interest rates reflect capital markets’ inflation expec-tations, which drive up the cost of any hedging strategy.

Also, inflation-linked bonds are typically characterised by limited supply and liquidity. Their effectiveness therefore depends on the timing and terms of purchase.

Effective insurer responses to inflation would have to occur preventively, rather than ex-post

Also, there is consensus that, for any long-term strategic asset allocation, hedges among traditional asset classes against unexpected inflation are imperfect or even ineffective.

However, there is some scope for inflation protection on the back of tactical asset allocation, for example by tilting the investment portfolio away from bonds towards commodities, equities and real estate in response to an inflation shock. For insurers, however, such benefits remain elusive in light of very high solvency capital requirements for those asset classes.

The value of insurance in times of inflation

Inflation is no stranger to the insurance industry. In some areas, it has been causing headaches for years. Take medical inflation, for example, where healthcare costs regularly rise faster than the general price level, albeit for a ’good’ reason: medical progress not only leads to better and more individualised treatment methods, but usually also to more costly ones.

Even though innovations are by their very nature difficult to forecast reliably, the industry has been good at dealing with this kind of inflation in the past.

Arne Holzhausen – Global Head Insurance, Wealth and Trend Research at Allianz

It is more difficult to deal with so-called ‘social inflation’, which is usually used to describe the phenomenon that compensation payments of all kinds have been set much more generously in recent years (especially in the U.S.). This affects a number of insurance lines, e.g. motor third-party liability and espe-cially directors’ & officers’ liability, where premiums have to be (sharply) increased and limits reduced.

The current situation, however, where prices are rising across the board, is a new challenge for the insurance industry – at least for the vast majority of insurance managers, who know the inflationary 1970s only by hearsay.

The rapid rise in prices is not even the biggest challenge; the surprise factor weighs more heavily.

For insurance customers, the fact that they have been able to buy expensive insurance cover relatively cheaply – compared with the skyrocketing prices of car and home repairs – is a positive development.

The value of their insurance coverage has increased. Of course, insurers will try to restore their profitability in subsequent years; premium increases are inevitable, because in the long run, only a profitable insurance business can also offer lasting and reliable risk protection.

From the customer’s point of view, one advantage remains: because inflation came as such a surprise, the adjustments will be made later.

Given the scale of the cost-of-living crisis, it is even quite likely that insurers will proceed with a sense of proportion and spread adjustments over several years, not least out of self-interest: excessive price increases could lead to sensitive volume losses if customers, households and companies alike can no longer cope with the price increases.

The salient feature of the insurance concept thus also proves its worth in times of inflation.

In the collective, financial burdens cannot only be shared but also smoothed out over time. The insurance industry cannot undo inflation for its customers, but it can act as a kind of buffer, creating valuable time for adjustment.

The need to fight inflation resolutely is thus not in question. On the contrary, a return to ‘normal’ and above all (relatively) stable inflation rates is essential. The insurance industry can cushion a shock to a certain extent, but not a lasting aberration with its immense economic and social costs.

…………………..

AUTHORS: Kai-Uwe Schanz – Head of Research & Foresight and Director Socio-economic Resilience The Geneva Association, Pieralberto Treccani – Research Support Manager The Geneva Association, Arne Holzhausen – Global Head Insurance, Wealth and Trend Research at Allianz