Overview

In the 14th annual Global Insurance Survey, a new macroeconomic risk category has emerged among insurers. According to Goldman Sachs Asset Management, tariffs and trade disputes now rank fifth among the top 10 risks to investment portfolios. Beinsure analyzed the GSAM’s report and highlighted the key points.

405 Chief Investment Officers (CIOs) and Chief Financial Officers (CFOs), representing over $14 trln in balance sheet assets combined, provide their insights regarding the macroeconomic environment, return expectations, industry capitalization and asset allocation.

Nearly one-third of 405 chief investment officers and chief financial officers surveyed cited it as a major concern. Last year, it did not appear on the list.

The recent GSAM survey highlights shifting macroeconomic concerns among insurance executives, emphasizing the impact of tariffs and trade disputes.

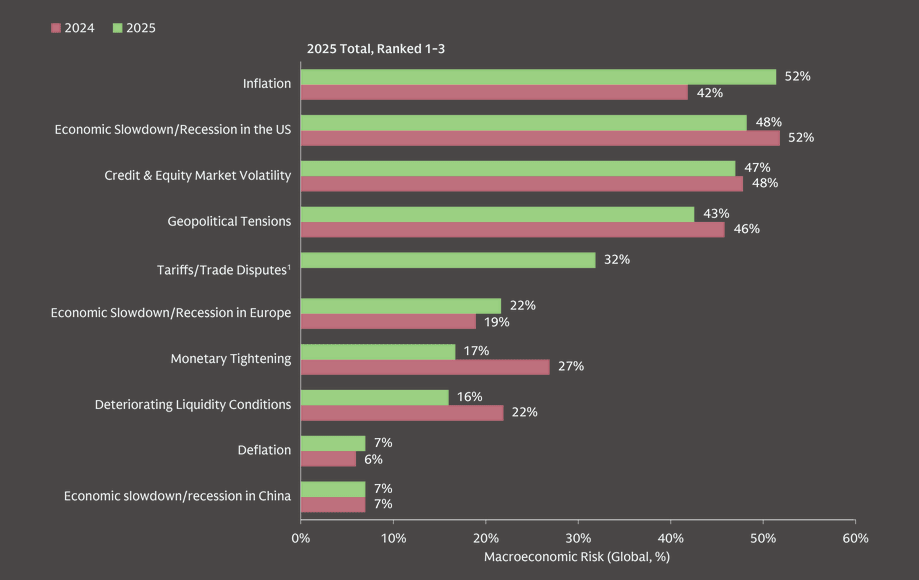

32% of surveyed insurance executives identified these issues as a significant macroeconomic risk, ranking 5th after inflation, recession, market volatility, and geopolitical tensions.

This marks a significant change, as tariffs did not feature on the list the previous year.

Key Insights from the Global Insurance Survey

- Rising Concerns Over Tariffs: The return of President Donald Trump and his administration’s approach to tariffs has sparked new concerns. The announcement of targeted tariffs, set to take effect on April 2, has heightened uncertainty.

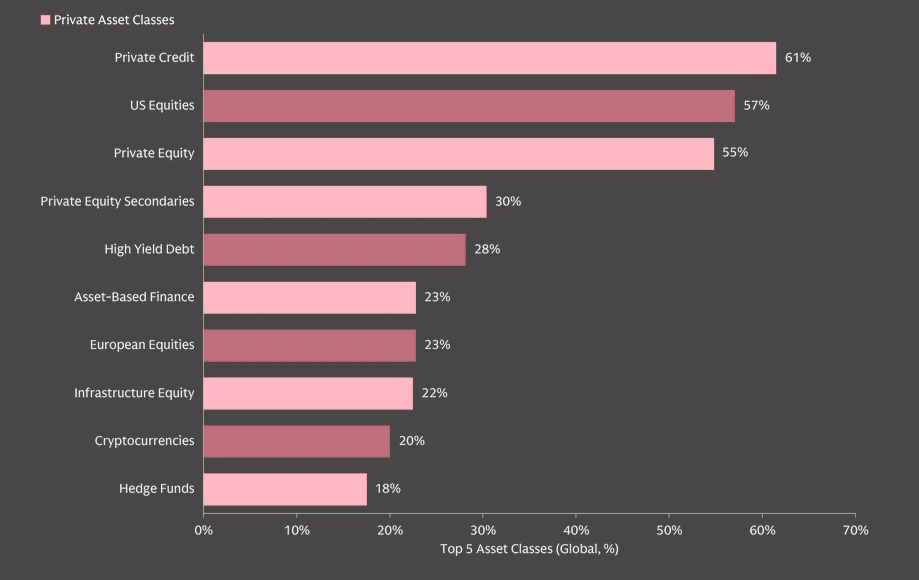

- Private Investment Market Shift: To navigate volatile economic conditions, insurers are increasingly moving into private investments. About 62% of surveyed executives plan to increase their allocation to private assets within the next year. Private credit stands out as a preferred asset class, with 61% anticipating high returns from it.

- Inflation and Recession Fears Persist: Inflation remains the top concern, cited by 52% of respondents, up from 42% last year. Recession fears remain substantial, with 48% indicating a risk of economic slowdown, a slight decrease from the previous year.

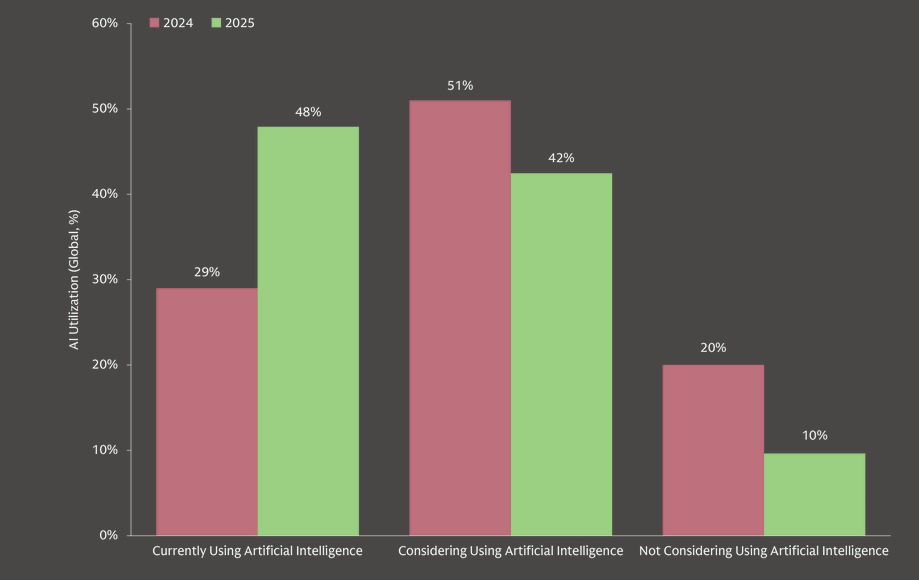

- Technological Transformation: The insurance sector is evolving with a strong focus on innovation and efficiency. Nearly half (48%) are already utilizing artificial intelligence, while another 42% are considering its implementation within the next year.

- Market Volatility and Geopolitical Risks: Despite a slight decrease from the previous year, market volatility and geopolitical tensions remain prominent concerns for insurance executives, cited by 47% and 43%, respectively.

Demographics of Respondents

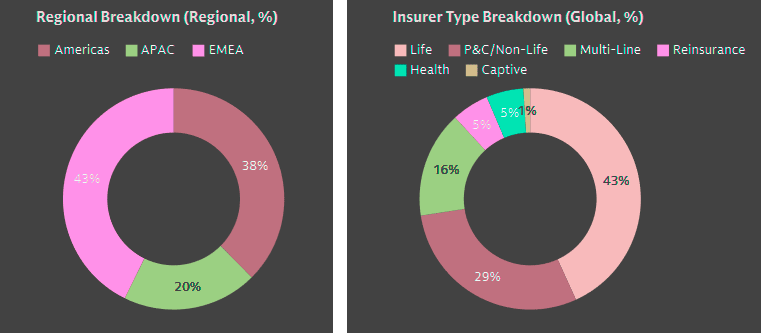

- Geographic Distribution: 38% from the Americas, 43% from Europe, the Middle East, and Africa (EMEA), and 20% from Asia-Pacific.

- Insurance Sector Breakdown: 43% of respondents represent life insurance carriers, followed by 29% from property/casualty (non-life), 16% from multiline carriers, and 5% each from reinsurers and health insurers. Captives made up 1%.

“As we continue to transform insights into actionable investment opportunities, we are excited to embark on another year of strong and dedicated partnership with our clients,” Mike Siegel says.

Macroeconomic Trends for 2025

The survey reflects how geopolitical actions, economic uncertainties, and innovation trends are reshaping risk perceptions in the insurance industry.

Our survey was conducted against a backdrop of macroeconomic uncertainty and a changing geopolitical landscape. This year’s title, The Great Pivot, accurately describes the shift towards illiquidity and acknowledges the continued momentum towards private asset classes.

As the landscape evolves, insurers are diversifying investments and embracing new technologies to mitigate risks and enhance operational efficiency (see Insurance Risk Dashboard. 10 Key Risks of the European Insurance Sector).

Navigating the Cycle

Insurers are concerned with the potential impact inflation may have on their portfolios, with 52% citing it as the greatest macroeconomic risk to their investments, an increase from 42% in 2024.

Entering its 14th year, the Goldman Sachs Asset Management Insurance Survey has once again achieved a record number of respondents. The survey indicates a heightened appetite for Private Credit, driven by its attractive risk-adjusted returns and diversification benefits.

Mike Siegel, Global Head of Insurance Asset Management and Liquidity Solutions

Other significant concerns include economic slowdown in the US, volatility in the credit and equity market, and geopolitical tensions, according to Global Economic and Insurance Market Outlook 2025-2026.

Rank the issues that pose the greatest macroeconomic risk in order of risk to your investment portfolio

Powering into Private Markets

Insurers continue to turn their attention towards alternatives: 62% of participants plan to increase their allocation to private assets within the next year.

Among these, Private Credit stands out, with 61% of respondents ranking it among the top five asset classes expected to provide the highest returns over the next 12 months.

This growing confidence is further underscored by the fact that 55% of insurers believe the credit quality is stable and 32% are prepared to take on more credit risk.

More than half of insurers globally view Private Equity as a potentially high-returning asset class for 2025. Additionally, 54% of insurers are considering investments through open-ended private market vehicles for their general account.

Alternative investing interest remains strong among insurers, with more than half planning to increase their allocation towards private assets in the next 12 months.

This trend is driven by the potential for higher returns, diversification benefits, and access to unique opportunities.

Which asset classes do you expect to have the highest total return in the next 12 months?

Ensured Innovation

The insurance industry is undergoing a period of significant transformation driven by innovation and a push for greater efficiency.

In a period of heightened merger and acquisition activity, 68% of all respondents believe the search for operational synergies and economies of scale as the primary drivers of this trend.

This movement towards efficiency is further amplified by the increasing adoption of Artificial Intelligence, as indicated by our survey.

Notably, 9 out of 10 respondents are currently using or are considering utilizing AI, with a striking 81% citing its primary benefit as reducing operational costs.

This proactive adoption of AI demonstrates a forward-thinking movement within the industry. The convergence of M&A activity, AI adoption, and climate-conscious investment strategies signifies a dynamic insurance sector, constantly striving for progress and innovation.

Is your company utilizing AI?

The survey findings indicate the insurance industry’s rapid adoption of Artificial Intelligence (AI). Notably, 90% of respondents are currently using, or are considering using AI, with a striking 81% citing its primary benefit as reducing operational costs.

We expect Private Credit to continue to offer compelling risk-adjusted returns in 2025. As the market expands, more financing opportunities will arise, providing attractive returns for insurance companies while diversifying their direct lending portfolios.

Stephanie Rader, Global Co-Head of Alternatives Capital Formation

This has led insurers to increase their allocations in this asset class, leveraging the benefits of different vehicle structures depending on their preferences (see about Future Impact of AI on Investment Market Strategy).

The report also highlighted that innovation and efficiency are transforming the industry, with 48% of insurers already using artificial intelligence and another 42% considering adoption within the next year.

Growing Concerns Over Trade Policies

Michael Siegel, global head of insurance asset management and liquidity solutions at GSAM, noted that the survey closed around six weeks ago.

He suggested that, given recent developments, the number of concerned executives would likely be even higher if the survey were conducted today.

Since January 20, President Donald Trump has proposed and adjusted tariffs on China, Canada, and Mexico. He has also advocated for broader retaliatory tariffs targeting key trading partners worldwide.

Recently, the Wall Street Journal reported that the White House plans to narrow the scope of tariffs set to take effect on April 2, shifting from industry-specific tariffs to a more targeted approach focused on major trading partners.

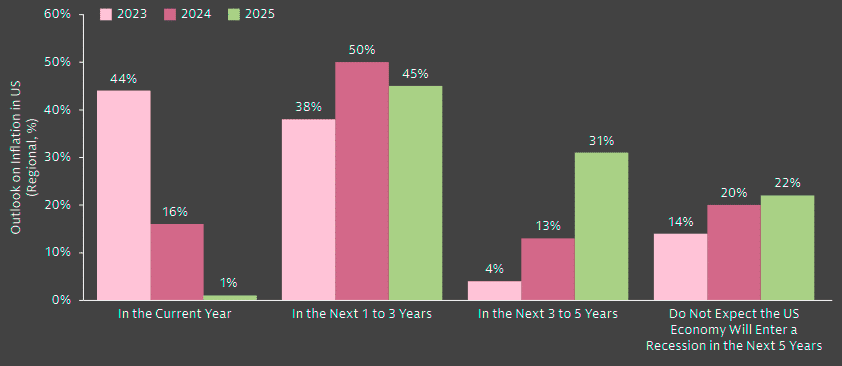

When, if at all, do you think the US economy will enter a recession?

Many insurers globally (46%) predict that the US will enter a recession within the next three years. Fears of a US recession have fallen meaningfully versus 2024 where over 67% of respondents expected a recession within the next three years.

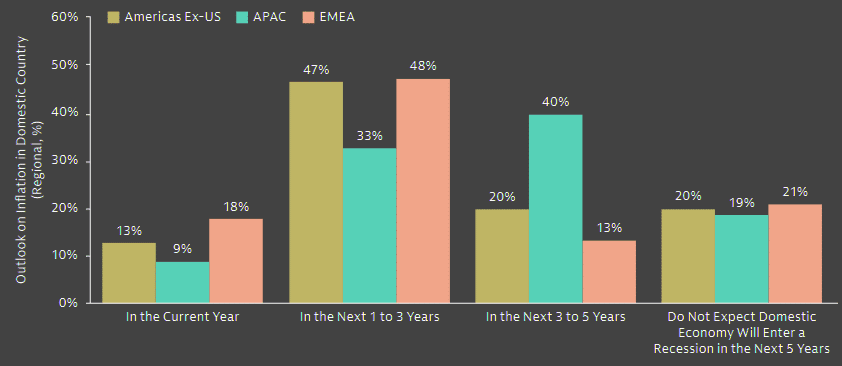

When, if at all, do you think your domestic economy will enter a recession?

Insurers have varying views when it comes to recession concerns in their respective regions. The majority of EMEA insurers (66%) expect their domestic economy to enter a recession within the next three years, with 18% of insurers expecting it to occur in the current year.

Similarly in the Americas, 60% of insurers expect a recession in next three years in their domestic countries. In APAC however, most insurers (59%) do not expect a recession within the next three years.

Shifting Investment Strategies

The survey also revealed that insurers are increasingly moving into the private investment market. Around 62% of participants plan to boost their allocation to private assets within the next year.

Private credit remains a standout, with 61% of respondents ranking it among the top five asset classes expected to yield the highest returns over the next 12 months (see Business Models and Investment Strategies of US Insurers).

Insurers globally are already benefiting from the transformative ability of Artificial Intelligence to improve risk underwriting and operational efficiencies. As the industry continues to expand and market consolidation accelerates, insurers will continue to think about their business and capital organization strategically in 2025.

Jared Klyman – Global Head of Insurance Strategy at Goldman Sachs

This can be achieved by revisiting their strategic asset allocation to maximise risk- and constraint-adjusted returns and by leveraging new technologies across their business activities.

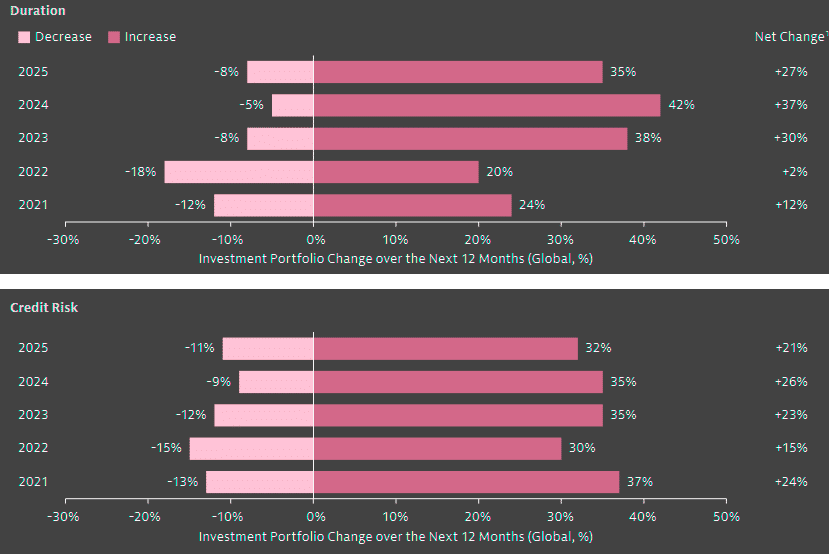

Over the next 12 months, are you planning to increase, maintain, or decrease duration and credit risk in your investment portfolio?

This year, 35% of respondents note that they intend to increase duration, while only 8% plan to decrease.

This shift suggests a continued demand in securing higher yields on fixed income securities, reflecting a cautious optimism about the interest rate environment.

This is a decrease from 2024, where 42% of insurers were looking to extend duration in their portfolios. Notably, 32% of insurers plan to increase credit risk in their portfolios this year, while only 11% intend to decrease.

Inflation and Recession Remain Top Concerns

Inflation remains the top macroeconomic risk, with 52% of executives naming it as a primary threat, up from 42% last year.

Concerns about a U.S. recession ranked second at 48%, down from 52% in the previous survey. Credit and equity market volatility followed at 47%, slightly down from 48% last year.

Geopolitical tensions ranked fourth at 43%, also down from 46% in 2024.

We expect policy uncertainty – especially trade – to pose significant headwinds to global growth this year. Our 2025 US growth outlook stands at a below-consensus 1.7% on a Q4/Q4 basis and we see inflation re-accelerating to 3% on the back of higher tariff rates.

Jan Hatzius, Chief Economist and Head of Global Investment Research

Fed policy normalization looks further off than previously expected, and we currently only see two 25bp cuts in June and December this year.

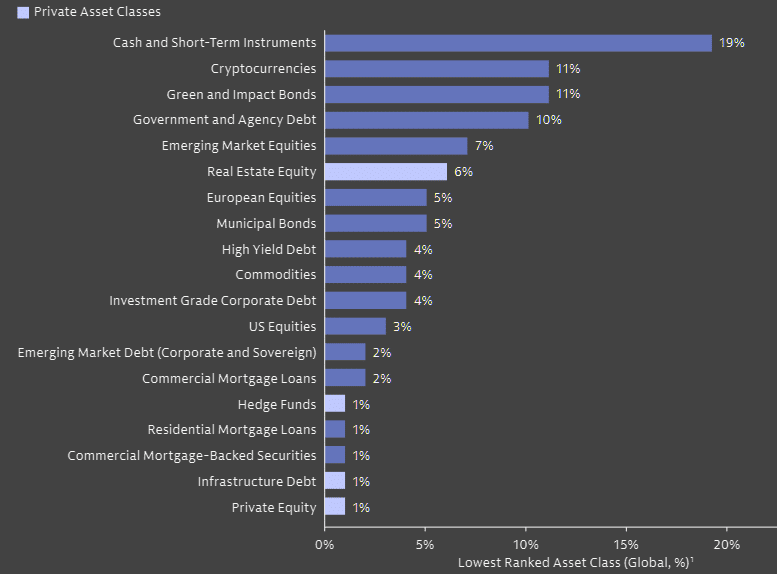

Please rank the 5 asset classes that you expect to deliver the lowest total returns in the next 12 months

Cash and Short-Term Instruments is ranked by 19% of insurers as the asset class that will yield the lowest returns. This is consistent with the great pivot, reflecting the movement from public to private assets.

The lack of consensus around cryptocurrency is evident, with 11% of insurers ranking it as the asset class with the lowest total return in the next 12 months.

Asset allocators are reassessing their fixed income strategies, with Private Credit providing insurers an opportunity to invest amidst market volatility and benefit from increased lender protections.

Kevin Sterling, Global Head of Asset Finance and Investment Grade Private Credit

Asset Finance, as an asset class, provides diversification beyond corporate credit, offering attractive spread premiums and customizable duration to align with liability requirements.

Demographics and Sector Breakdown

38% surveyed were from the Americas, 43% from Europe, the Middle East, and Africa (EMEA), and 20% from Asia-Pacific. Life insurers made up the largest share at 43%, followed by property and casualty insurers at 29%.

Multiline insurance carriers accounted for 16%, with reinsurers and health insurers each representing 5%. Captives made up the remaining 1%.

As the industry continues to evolve, the increasing focus on private investments and technology adoption reflects a strategic shift to navigate economic challenges and leverage new opportunities.

FAQ

Inflation remains the top concern, with 52% of executives citing it as the greatest risk, up from 42% last year. Recession fears rank second at 48%, followed by market volatility (47%) and geopolitical tensions (43%). A new risk category—tariffs and trade disputes—entered the top five this year, cited by 32% of respondents.

To navigate economic uncertainties, insurers are increasingly moving into private investments. About 62% of surveyed executives plan to increase their allocation to private assets within the next year, with private credit standing out as a top asset class expected to yield high returns.

The insurance industry is rapidly adopting artificial intelligence to enhance operational efficiency. Nearly 48% of insurers already use AI, and another 42% are considering it within the next year. AI adoption aims primarily at reducing operational costs and improving risk underwriting.

The survey includes responses from 405 Chief Investment Officers (CIOs) and Chief Financial Officers (CFOs) managing over $14 trillion in assets. Geographically, 38% are from the Americas, 43% from Europe, the Middle East, and Africa (EMEA), and 20% from Asia-Pacific. Life insurance carriers represent 43% of respondents, followed by property/casualty (29%), multiline carriers (16%), reinsurers (5%), and health insurers (5%).

Insurers are strategically diversifying their portfolios to mitigate economic risks. Around 35% of respondents plan to increase duration in their portfolios to secure higher yields on fixed-income securities, while 32% intend to increase credit risk exposure.

The potential for higher returns and diversification benefits is pushing insurers towards private assets. Private credit, in particular, is expected to yield substantial returns over the next 12 months, with 61% of respondents ranking it among the top five high-return asset classes.

While concerns about a U.S. recession have decreased from last year, 46% of insurers globally still predict a recession within the next three years. The majority of EMEA insurers (66%) expect a domestic recession within three years, compared to 60% in the Americas and only 41% in Asia-Pacific.

……………………

QUOTES: Michael Siegel — Partner at Goldman Sachs, Global Head of Insurance Asset Management & Global Head of Liquidity Solutions, Co-Head of the Client Solutions Group in Asia Pacific at Goldman Sachs Asset Management, Jan Hatzius – Chief Economist and Head of Global Investment Research at Goldman Sachs, Stephanie Rader, Global Co-Head of Alternatives Capital Formation at Goldman Sachs, Jared Klyman – Global Head of Insurance Strategy at Goldman Sachs, Kevin Sterling – Global Head of Asset Finance and Investment Grade Private Credit at Goldman Sachs

Edited by Nataly Kramer — Editor at Beinsure Media