Overview

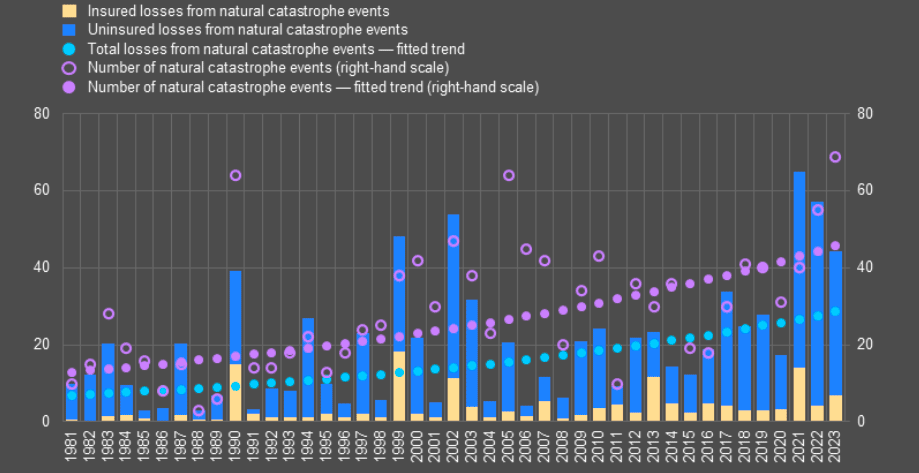

- Economic losses from and number of natural catastrophes in the EU

- Proposed EU-Level Framework: Re/insurance Scheme

- Evolution of the natural catastrophe insurance protection gap in Europe

- Evolution of reinsurance and natural catastrophe insurance coverage

- Lessons from national insurance schemes

- Stylised decomposition of the catastrophe risk insurance premium

Economic losses from natural catastrophes in the EU are rising due to increased economic exposure and the growing severity of climate-related disasters. Between 1981 and 2023, NatCat events caused €900 bn in direct losses, with one-fifth of the total occurring in the past three years alone. However, only about 25% of these losses were insured, and this share continues to decline, according to European Central Bank and EIOPA’s report about European system for natural catastrophe risk management and insurance.

Europe, the fastest-warming continent, faces escalating climate risks that threaten insurance affordability and availability.

As the frequency and severity of climate-related events grow, (re)insurance premiums are expected to increase, making coverage less accessible, particularly for low-income households.

The unpredictability of such events may also lead insurers to withdraw from high-risk areas. Low awareness of risks and reliance on government disaster aid further suppress insurance adoption among individuals and businesses (see Natural Catastrophes Drivers. 6 Main Lessons for Insurance Industry).

Between 1981 and 2024, natural catastrophe-related extreme events caused around €900 bn in direct economic losses in the EU, with more than a fifth of the losses occurring in the last three years (2021: €65 bn; 2022: €57 bn; NatCat in 2023: €45 bn)

The floods of 2024 in central and eastern Europe, as well as in Spain, highlighted the challenges extreme weather poses to the EU and its Member States. These events emphasized the importance of emergency preparedness, risk mitigation, and adaptation to prevent and minimize economic losses.

They also underscored the need for effective national insurance schemes to reduce the financial burden of natural disasters and address the growing insurance protection gap, which places increasing strain on public finances.

An EU-level approach could provide a solution to these challenges by building on existing national and EU structures. A public-private reinsurance mechanism could pool risks across regions and perils, increasing diversification and stabilizing the market (see Global Insured & Economic Losses from Natural Catastrophes Outlook). This would support broader insurance coverage for natural catastrophes while encouraging national-level solutions.

Economic losses from and number of natural catastrophes in the EU

A complementary EU fund for public disaster financing could improve risk management and support reconstruction efforts, with payouts tied to risk mitigation and climate adaptation measures pre-agreed under national plans. Together, these measures aim to reduce economic losses, promote insurance adoption, and strengthen Europe’s resilience to climate risks.

Proposed EU-Level Framework: Re/insurance Scheme

A two-pillar approach is recommended to address these challenges, leveraging existing national and EU mechanisms:

1. EU Public-Private Reinsurance Scheme

- Objective: Expand insurance coverage for natural catastrophe risks, particularly in areas with low insurance penetration.

- Mechanism: Pool private risks across the EU and diversify by peril and region to enhance stability and scalability. The scheme would encourage and support national-level solutions while operating as a voluntary mechanism.

- Funding: Risk-based premiums from (re)insurers or national schemes. However, care must be taken to avoid excessive market segmentation from risk-based pricing.

- Outcome: This scheme would stabilize the insurance market, achieve economies of scale, and provide broad coverage for high-risk areas, functioning similarly to an EU public-private partnership.

2. EU Fund for Public Disaster Financing

- Objective: Enhance disaster risk management and support reconstruction efforts after major natural disasters.

- Mechanism: Member State contributions would fund the initiative, adjusted for national risk profiles. Fund payouts would be contingent on the implementation of agreed-upon risk mitigation and climate adaptation measures.

- Outcome: The fund would incentivize robust national adaptation plans and ensure prudent use of resources for reconstruction.

The complementarity of the two pillars would ensure the efficient use of private and public sector funds for natural disaster payouts, while also encouraging ex ante risk mitigation.

First, this approach would improve cost efficiency by covering risks ex ante across households, businesses and governments. The two pillars would enhance risk pooling and provide incentives for risks to be borne at the lowest possible level.

Second, the approach recognises the primary role of the private insurance sector in covering most of the damages caused by a disaster, thus reducing the need for public financing for damage caused to households and businesses. Third, and importantly, it is compatible with national initiatives for improving insurance coverage, through schemes or funding solutions.

At the same time, the approach acknowledges that governments retain certain responsibilities, including the reconstruction of public infrastructure. While in principle each pillar could be implemented independently as a stand-alone instrument, the

pillars would reinforce each other and be more effective if implemented jointly.

Ideally, the two pillars should work in unison to provide incentives for ex ante risk mitigation and additional financial support for the highest loss layer natural catastrophes, for the ultimate benefit of households, businesses, and governments.

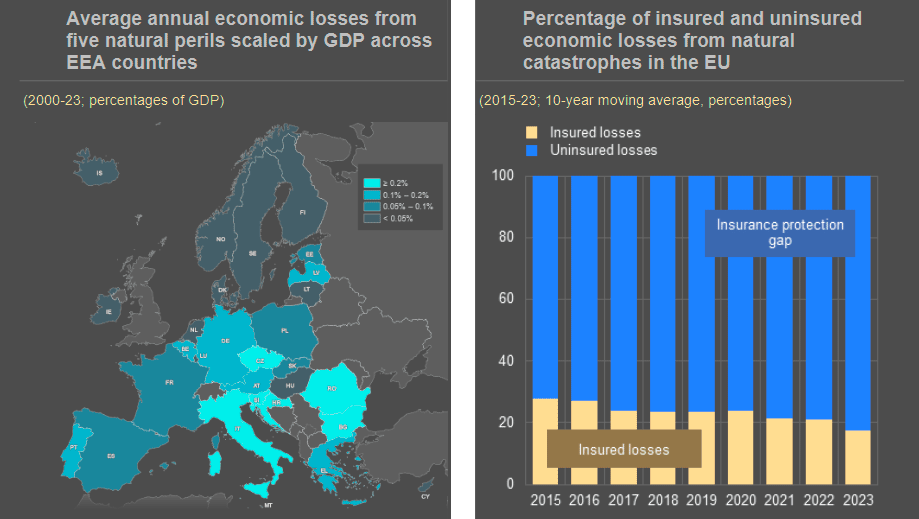

Evolution of the natural catastrophe insurance protection gap in Europe

Geographical distribution of economic losses from five natural perils and the evolution of the natural catastrophe insurance protection gap in Europe.

Natural catastrophe insurance uptake among low-income households in the EU is declining, increasing the burden on governments to provide financial assistance when disasters occur. The proportion of low-income consumers with property damage insurance for natural catastrophes has dropped from 14% to 8% since 2022. Affordability and budget constraints remain the primary reasons why 19% of European consumers either do not purchase or fail to renew insurance.

Low-income households face heightened vulnerability to financial and environmental stress. They are more likely to live in areas prone to natural catastrophes due to the affordability of land and housing.

Limited resources often prevent them from relocating to safer areas or investing in disaster-resistant housing. Rising insurance costs also exacerbate housing affordability issues, as households must allocate a larger share of their income to insurance, leaving less for essential expenses like rent.

Evolution of reinsurance and natural catastrophe insurance coverage

Addressing these challenges requires solutions that incorporate vulnerability and consumer protection measures. Policymakers and insurers need to consider the unique risks faced by low-income households and develop strategies to ensure affordable access to insurance while mitigating the broader financial impact on these communities.

Aside from insurance premiums and income constraints, the insurance protection gap is driven by further supply and demand factors.

On the demand side, the limited take-up of insurance (generally, though also specifically for natural catastrophe insurance) among households and businesses can also be attributed to high expectations of government intervention in times of disaster (moral hazard), lack of clarity on the scope of coverage in insurance contracts, previous negative experience with insurance payouts and limited risk awareness.

On the supply side, climate change makes risk-based pricing more challenging as risks become more unpredictable. Moreover, the spatial correlation of risks, affecting whole sectors, communities and large geographical areas, can affect various lines of insurance business.

Natural disaster risks are fat-tailed, with a high probability of extreme losses, requiring insurers to have sufficient funds to cover these losses.

These factors negatively affecting insurance demand and supply could be addressed by, among others, measures aimed at improving risk awareness and clarity on insurance contract coverage, or by fostering opportunities for risk prevention and adaptation.

Several factors influence both the demand and supply of natural catastrophe insurance

Several factors influence both the demand and supply of natural catastrophe insurance, leading to gaps in coverage. On the demand side, low risk awareness and underestimation of the likelihood of being affected by natural catastrophes hinder insurance uptake.

Many individuals and businesses have a limited understanding of the scope of coverage, often due to unclear terms in insurance contracts.

Additionally, high premiums or the perception of unaffordability deter consumers, while expectations of government assistance reduce the perceived need for insurance. Other barriers include a lack of trust stemming from negative past experiences with claims, the complexity of insurance products, and limited access to distribution channels.

Factors negatively affecting insurance demand and supply in the context of natural catastrophe coverage

| Category | Factors Lowering Insurance Demand | Factors Lowering Primary Insurance Supply |

| Risk Identification | Low level of risk awareness. | Uncertainty and unpredictability in risk evolution (e.g., due to lack of granular data or modeling complexity). |

| Underestimation of the likelihood of being affected by disasters. | ||

| Scope of Coverage | Incorrect knowledge or assumptions about coverage terms for natural catastrophes (e.g., unclear insurance contract terms). | Challenges in diversifying risks nationally or regionally. |

| Cost of (Re)Insurance | Premiums perceived as unaffordable or overly expensive. | Reduction in reinsurance capacity. |

| Moral Hazard | Expectation of government disaster support. | Expectation of government disaster support. |

| Other Factors | Lack of regulatory incentives for risk prevention. | Lack of regulatory incentives for risk prevention. |

| Past negative experiences with insurance claims reducing trust. | Limited competition in private (re)insurance markets. | |

| Perception of insurance as complex and time-consuming. | ||

| Lack of understanding of insurance products or access to distribution channels. |

On the supply side, insurers face challenges in diversifying risks at national or regional levels, particularly given the unpredictability of climate risks and the lack of granular data. Rising reinsurance costs and reduced reinsurance capacity further constrain the market.

Regulatory frameworks may fail to provide adequate incentives for risk prevention, while limited competition in private insurance markets restricts innovation and affordability.

These factors collectively undermine the availability and affordability of natural catastrophe insurance, exacerbating the protection gap across the EU.

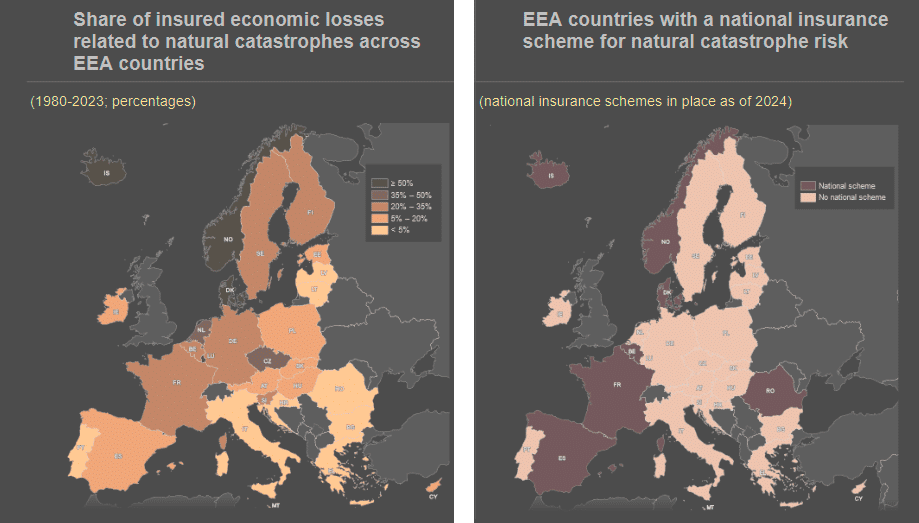

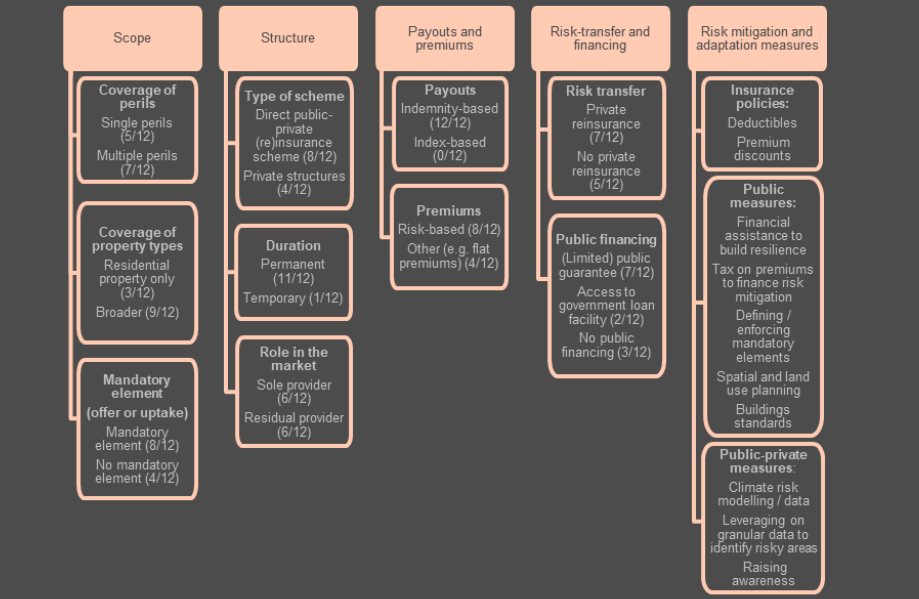

Lessons from national insurance schemes

National schemes to supplement private insurance cover for natural catastrophes, such as PPPs, help improve insurance coverage and reduce the insurance protection gap.

Looking at the European Economic Area (EEA), the share of insured losses tends to be higher in countries with such national schemes: the average share across countries with a national scheme is around 47%, while it is below 18% for those without a national scheme. Currently, eight EEA Member States have established a national scheme.

Share of insured economic losses related to natural catastrophes and national insurance schemes for natural catastrophe risk in Europe

Against this backdrop, this paper identifies national practices on which EU solutions could build to improve insurance coverage and reduce the fiscal burden for natural catastrophe losses across Europe.

Design features of national insurance schemes

The present analysis of the design features of national schemes is a first step to inform further potential initiatives at both national and EU level.

The following sub-sections therefore elaborate on the main design features of the 12 national schemes. They also draw lessons for developing an EU solution that could help overcome some of the limitations of national initiatives.

The revised intervention ladder delineates private and public funding responsibilities more distinctly

The proposed EU-level intervention seeks to reinforce and supplement private insurance, reinsurance, alternative risk transfer, and national measures, which remain essential components in the intervention hierarchy.

As outlined in the original 2023 framework, the foundational layer addresses losses from low-impact disasters, which constitute the majority of climate-related events.

For higher-loss layers, private sector reinsurance acts as a backstop for private insurers. National schemes provide additional capacity for higher-impact disasters. For the most extreme loss events involving privately insured damages, the revised ladder introduces a European public-private reinsurance scheme.

This scheme offers additional reinsurance to private (re)insurers based on risk-adjusted premiums. Although facilitated by the EU, this mechanism could potentially operate exclusively on private funding.

Even with broader insurance coverage, market-based funding alone would not suffice. Government contributions remain necessary for post-disaster reconstruction of public infrastructure. While the EU public-private reinsurance scheme covers public sector assets insured by private companies, some public assets may not be efficiently insurable through private markets.

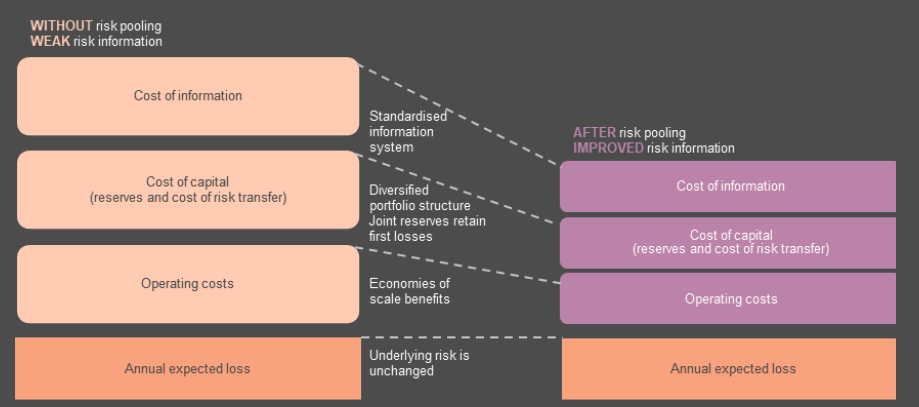

Stylised decomposition of the catastrophe risk insurance premium

The primary benefit of pooling natural catastrophe risks lies in the impact of diversification of losses on the risk-bearing capital needed to support the risk across the pool. This diversification occurs both across multiple perils and also across geographical areas.

The diversification effect arises from the fact that severe losses are unlikely to occur simultaneously across all participating entities. As a result, the capital needed to ensure that the pool can honour its obligations to the insured is lower than the sum of supporting capital that would be needed if countries considered their potential maximum losses individually.

Sovereigns with diversified funding sources and significant risk-pooling opportunities might face challenges insuring major transport infrastructure, such as roads, bridges, and railways. These assets are costly to insure privately but essential for economic recovery after natural disasters.

National and subnational governments are expected to absorb most losses from uninsured public assets. However, a European public disaster fund, financed by contributions from Member States, would provide immediate fiscal support for severe disasters.

This fund would facilitate infrastructure rebuilding by offering payouts to governments. Establishing clear access criteria and payout conditions would promote responsible budgeting, incentivize effective risk mitigation, and help contain public costs through risk pooling.

FAQ

Economic losses are increasing due to growing economic exposure and the escalating severity of climate-related disasters. Between 1981 and 2023, these events caused €900 bn in direct losses, with over 20% occurring in the past three years.

Only about 25% of natural catastrophe losses are insured, and this share is declining. Rising (re)insurance premiums are making coverage less accessible, particularly for low-income households.

Europe’s rapid warming and frequent climate events are driving up insurance premiums. Insurers may withdraw from high-risk areas, further limiting accessibility. Low awareness and reliance on government aid also reduce insurance adoption.

Countries with national schemes have higher insured loss shares (average 47%) compared to those without such schemes (below 18%). These schemes supplement private insurance, improving coverage and reducing the fiscal burden on governments.

The framework includes two pillars: 1) An EU public-private reinsurance scheme to pool risks across regions and perils, expanding insurance coverage. 2) An EU disaster fund to finance post-disaster reconstruction, tied to national risk mitigation and climate adaptation measures.

The scheme would stabilize the insurance market by diversifying risks geographically and across perils. It would also provide economies of scale, enhance coverage for high-risk areas, and encourage national-level solutions.

Barriers include low risk awareness, high premiums, reliance on government aid, unclear insurance terms, and limited competition in private insurance markets. Rising reinsurance costs and unpredictable risks due to climate change further exacerbate the issue.

……………………

AUTHORS: Nicholai Benalal – European Central Bank, Frankfurt am Main, Germany; Paolo Alberto Baudino – European Central Bank, Frankfurt am Main, Germany; Marien Ferdinandusse – European Central Bank, Frankfurt am Main, Germany; Casper Christophersen – European Insurance and Occupational Pensions Authority, Frankfurt am Main, Germany; Hradayesh Kumar – European Insurance and Occupational Pensions Authority, Frankfurt am Main, Germany

Edited by Oleg Parashchak – Finance Media