As Group Chief Economist for Swiss Re, Jérôme is responsible for the economic and insurance market research. He is also the managing editor for the sigma series, Swiss Re’s flagship research series.

Jérôme leads the global research teams located in Zurich, New York, Bangalore, Beijing and Hong Kong and provides macro and insurance industry research and associated consulting services for the Group. He steers the scenario analysis, provides the macro and insurance industry analysis and forecasts, while contributing to a sound global financial market architecture and making the world more resilient.

Jérôme served as Co-Chair of the World Bank’s Global Infrastructure Facility (GIF) Advisory Council. He is particularly active in external committees at the Institute of International Finance and the WEF and participates in roundtable discussions with policymakers; this to strengthen the positive dual role of the insurance sector as a long-term investor and risk absorber. Jérôme is a Board member of Global Asia Insurance Partnership (GAIP) in Singapore and the International Capital Market Association (ICMA). He also serves as Director of the Board at the China Asia-Pacific Reinsurance Research Center (CAPRRC).

Previously at Swiss Re, Jérôme was Head of Investment Strategy at its proprietary Group Asset Management for nearly ten years. Prior to joining Swiss Re, he was Swiss National Bank’s Delegate at the Executive Board of the International Monetary Fund in Washington DC and Senior Economist at the Swiss National Bank, UBS Warburg and Bank Julius Baer.

Jérôme holds a PhD in Economics from the University of Basel, an MSc in Economics from the London School of Economics and was a Visiting Fellow at Harvard University’s Economic Department.

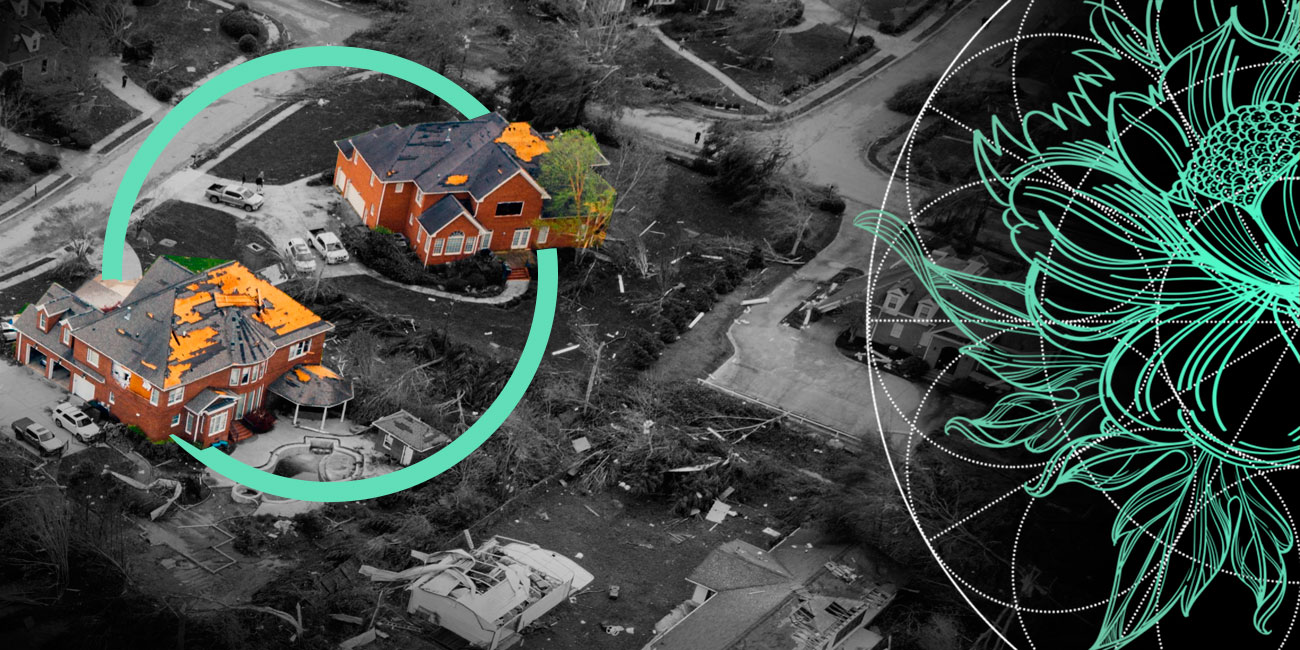

Global insured losses from natural catastrophes reach $80 bn in the first half of 2025. This is almost double the 10-year average and more than half of the $150 bn

Global premium growth is slowing in both life and non-life insurance. After strong growth of 5.2% in 2024, premiums are forecast to grow just 2% in 2025, improving slightly to 2.3% in 2026

The insurance industry faces several ongoing challenges linked to long-term economic, social, and environmental trends. These structural risks require active management to ensure protection

In the US, two major hurricanes and frequent severe thunderstorms accounted for at least two-thirds of the year’s global insured losses, which currently exceed $135 bn

2024 is on track to become the hottest year recorded. A warming climate has intensified natural catastrophes, especially in Europe, which faced severe flooding

Natural catastrophes will once again break several insured loss records in 2023. A high number of low-to-medium-severity events will aggregate to insured losses

The global non-life insurance industry is adjusting rapidly to the new higher interest rate era ushered in by the most intense monetary policy tightening since the 1980s

Aviation insurance refers to indemnification of a client against losses arising from the result of damages, maintenance, or use of aircraft, and hangars at the airport