Overview

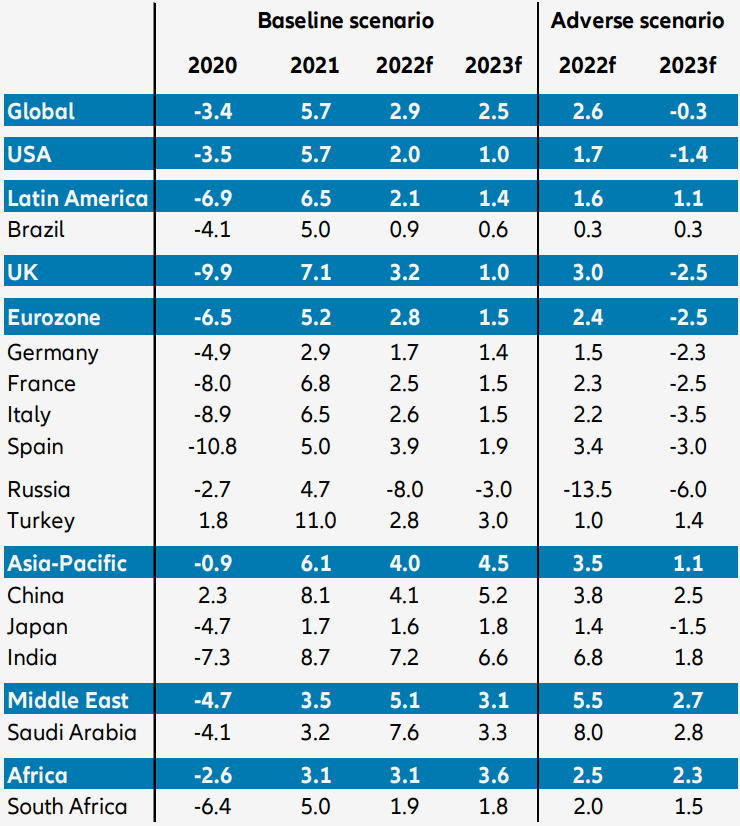

Allianz expect global GDP growth at +2.9% this year and +2.5% in 2023, down by -0.4pp and -0.3pp compared to our last forecast.

The revision is due to the larger direct and indirect impacts from the war in Ukraine and the longer-than-expected lockdowns in China, which will reduce output by -1.2pp and -0.6pp in 2022 and 2023, respectively.

Global growth is entering a soft patch this year as uncertainty due to geopolitical risks remains high

According to Allianz Research, global trade has most probably contracted in Q2 (-1.3% q/q). The Chinese reopening will support some catch-up effects for trade, and therefore global GDP growth, going into the summer, but we expect a rather timid recovery.

Soft patch for global growth

We now forecast global trade to grow by +3.5% in 2022 and +3.6% in 2023 in volume terms, much below consensus. In value terms, the strength of the dollar coupled with high inflation in 2022 will push nominal growth to +10.4% before it slows to +4.2% in 2023.

While a soft landing remains our baseline scenario for 2022, downside risks of a recession are building up fast

This time the concern is not only about the magnitude of the recession, but also the distribution effects. As record-high inflation (8.1% in 2022 at the global level) degrades real disposable incomes, households and corporates are likely to scale back consumption and investments, respectively.

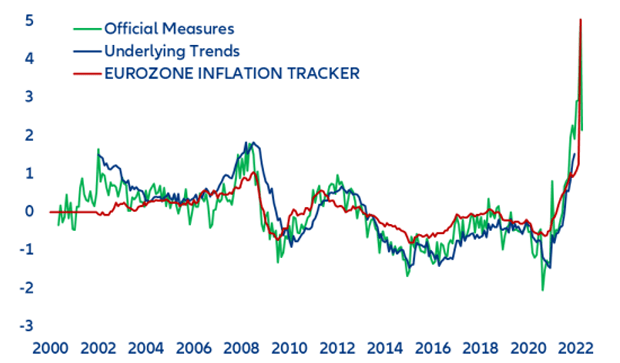

Eurozone: Headline Inflation (z-score)

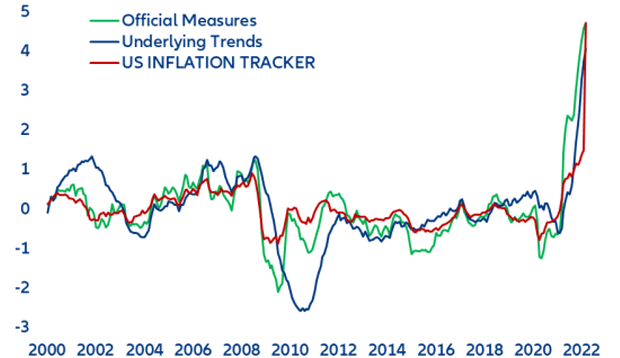

US: Headline Inflation (z-score)

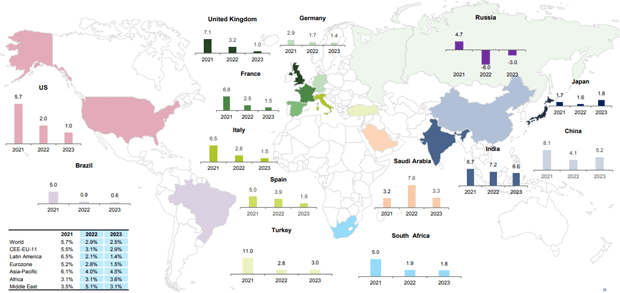

While consumer sentiment is plunging, business confidence is still holding up. However, lower planned capex suggests that corporates are becoming more cautious. As inflation stays high for longer (4.7% in 2023 globally; above 3% in the US, Eurozone, UK), the risks of a wage-price loop are increasing.

Global Inflation rates

A complete and disorderly suspension of oil and gas imports from Russia to the EU by year-end could bring about our “adverse” scenario (40% probability), in which the major economies are pushed into a recession. In this scenario, policymakers would fail to save the day à la 2020 as central banks’ initial fixation on fighting inflation constrains fiscal policy options. Meanwhile, the expected policy u-turn in H1 2023, including aggressive rate cuts, would come too late.

The suspension of oil and gas imports from Russia to the EU is expected to cost -1.6pp of EU GDP growth as we estimate the energy shortfall after substitution and self-rationing at about 4% of final energy consumption against 10%

Overall, taking into account the additional impact from tightening monetary and financial conditions, we expect global GDP growth would contract by -2.8pp in 2023 to -0.3% in the adverse scenario (after slowing by -0.3pp to +2.6% in 2022). This implies a recession of -1.4% in the US and -2.5% in the Eurozone and the UK – roughly 1.5-standard deviations from two-year trend growth in terms of output loss. China’s growth would slow to +2.5% in 2023.

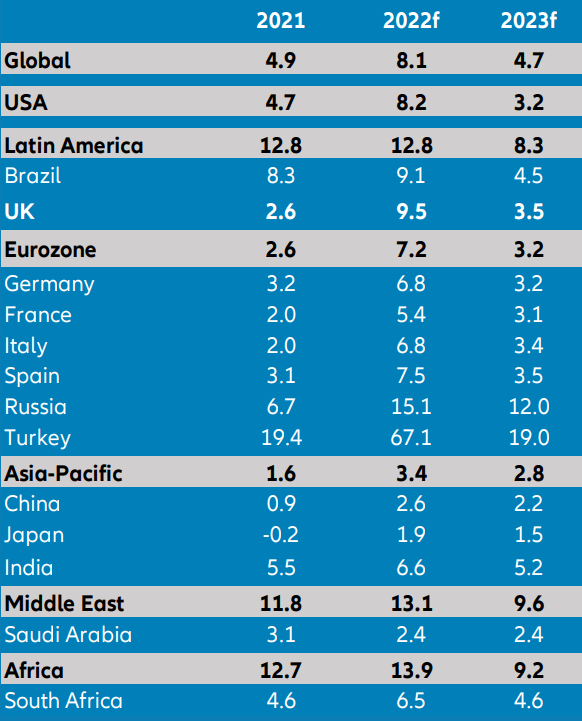

Global GDP growth forecasts

Policy space to contain downside risks is diminishing quickly. Central banks in advanced economies have become more determined to aggressively tackle inflation as supply-side price pressures remain strong. We expect the Fed to increase interest rates to at least 3.5% by end-2022 and the ECB to 0.75%.

However, tightening financing conditions to dampen aggregate demand can easily trigger a recession, especially in countries where the recovery from the Covid-19 crisis is still not complete.

Fiscal policy can help to limit adverse distributional effects but will not be enough to stave off the growth slowdown and could perpetuate high inflation.

In our adverse scenario, we expect inflation-focused monetary tightening to cause a sizable contraction of demand, resulting in a global recession in early 2023, amplified by depressed asset prices. In this situation, we expect global GDP growth to contract by -2.6pp in 2023 to -0.1% (after slowing by -0.3pp to +2.6% this year.

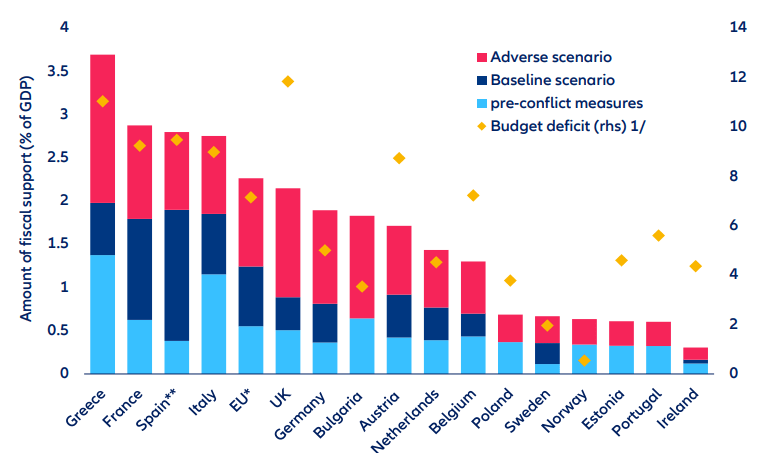

Eurozone: Estimated fiscal support and comparison with Covid-19 crisis measures

What does this mean for corporates?

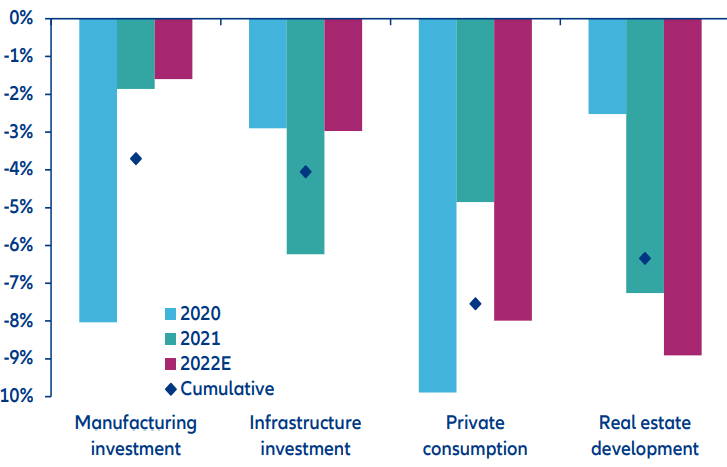

High cost pressures are dampening some investment prospects, but some catch-up effects might be likely in H2 as input shortages reduce significantly and supply normalizes while demand slows down further.

Structural headwinds such as higher energy prices (with oil averaging 105 USD/bbl in the remainder of 2022 and remaining over 90 USD/bbl well into next year) coupled with rising interest rates and wage acceleration would continue to put pressures on corporate margins going forward.

Simulating the impact of an increase of 200bp in corporates’ interest rates, we estimate that profitability is most at risk in construction, energy, transportation and computers & telecom, with the impact after one year ranging, depending on the sector, from -5.7pp to -2pp margin loss in the US and more than -7pp to -3pp in the Eurozone.

After two years of declines, we expect global business insolvencies to rebound by +10% in 2022 and +14% in 2023, approaching their pre-pandemic level. One in three countries will return to pre-pandemic levels in 2022 and one in two countries in 2023.

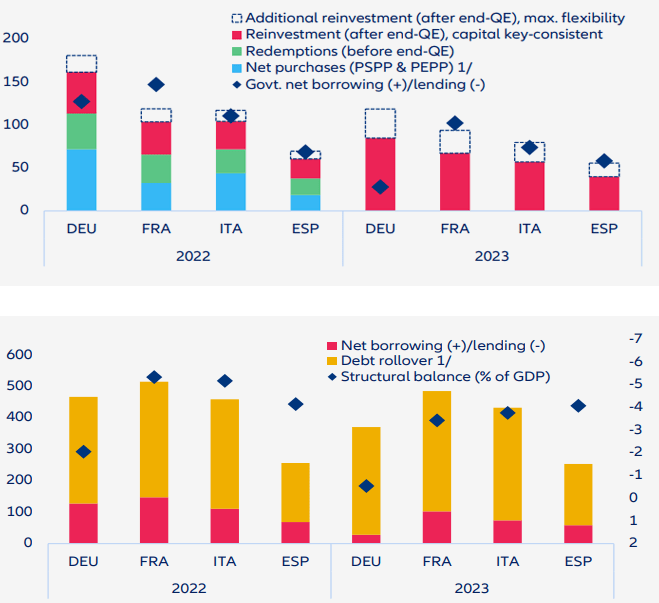

Eurozone: Estimated Eurosystem purchases of government debt and estimated refinancing needs

Capital markets are getting fickle

The hawkish shift of major central banks (withthe exception of China and Japan) has unsettled fixed income and equity markets alike. Rising rate expectations have led to a significant upward revision of long-term rates.

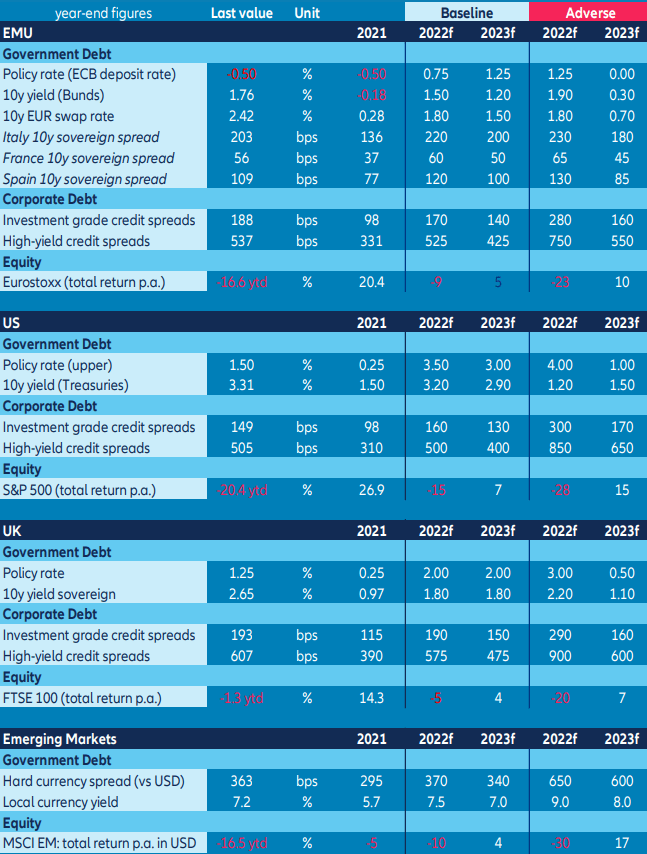

We expect the 10Y benchmark Bund yield at 1.5% by end-2022 and the 10Y US Treasury yield at 3.2%.

Equity markets have corrected by more than -20% already since the beginning of the year and still have room to drop further. Market movements have been extreme but volatility remains contained compared to past stress episodes.

We expect equities to remain under pressure for the remainder of the year on the back of continued pressures on corporate margins. Credit spreads have exhibited a pattern similar to that of equities but have remained relatively resilient.

For emerging markets, risks keep building up due to the double whammy of more aggressive Fed tightening and slowing external demand, which will continue to intensify net capital outflows.

We see limited upside potential for commodity exporters in the short-term. In addition, geopolitical risks have raised concerns about investments in China.

Capital market forecasts

The specter of sovereign debt distress is emerging in Europe

A widening of sovereign spreads due to rising rates raises the refinancing cost of vulnerable Eurozone countries, such as Italy, that are struggling with widening deficits and low potential growth.

So far, high inflation and NGEU funds from the EU have helped stabilize the debt level. However, as real rates increase and growth keeps slowing, fiscal space will diminish rapidly.

With a general election scheduled in Italy for H1 2023, we see an elevated risk for a period of political instability ahead.

While a sensible national reform program, including a responsible fiscal consolidation plan, remains key to instill confidence in Italian debt, mitigating EU reform steps will likely be necessary, too.

More demands on fiscal policy amid rising social discontent might call for an extension of national budget firepower via a centralized EU fiscal capacity to fund essential spending (e.g. climate transition and defense).

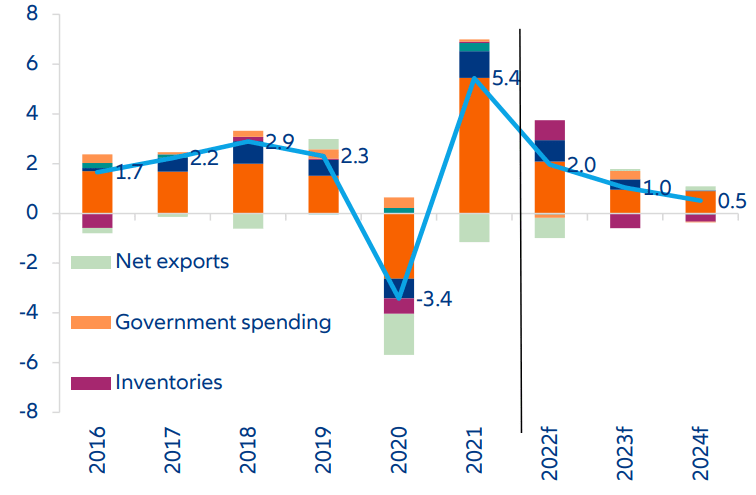

US GDP growth and components (%)

Political risk is back

Important elections taking place over the coming 18 months will likely see key economies increasingly prioritize domestic issues, at least temporarily.

In H2 2022, all eyes will be on leadership contests in the world’s two largest economies. Hence, expect the US and China to turn their focus above all to domestic affairs, away from Taiwan and Ukraine.

In the US, midterm elections will reach their climax on 08 November, when the first nationwide vote since the 2020 presidential election is scheduled. As President Biden’s approval ratings have been falling from one record low to another, Democrats are unlikely to retain their (slim) majority in Congress. Last minute attempts to pull back on less popular goals and to extend more support to a slowing economy should not be ruled out.

China: Distance from pre-pandemic trend (%)

Meanwhile, in China, the coming months will be punctuated by crucial political events: the CCP’s 20th National Congress and a plenum in March 2023 that will officialize the party and state leaders for the coming five years.

Policymakers will likely aim for stable and managed economic and sanitary situations in the run-up to these events, meaning further policy support to short-term growth amidst the zeroCovid policy.