The US P&C insurance industry has experienced challenges in recent years due, in large part, to increases in the frequency and severity of natural catastrophes, as well as a tightening reinsurance market, according to Financier Worldwide Magazine.

Natural and man-made disasters resulted in global economic losses of USD 280 billion in 2022, the sixth highest on Swiss Re sigma records, and the 16th highest since 1970 after normalising for GDP growth effects.

Of the economic losses, $270 bn was attributable to natural catastrophes. In addition to a devastating earthquake in Haiti that, sadly, claimed more than 2 000 lives, there were more than 50 severe flood events across the world, as well as tropical cyclones, episodes of extreme cold and heat, and severe convective storms (SCS).

As private market capacity has declined, the number of Floridians being insured by Florida’s state-run insurer of last resort, Citizens Property Insurance Company, has nearly tripled in less than two years.

According to Global Commercial P&C Insurance Market Review, Florida’s property insurance market has been negatively impacted by contractors who exploited the state’s former one-way attorney fee statute by artificially inflating the cost of insurance claims in collaboration with questionable billboard attorneys. These additional challenges have created unsustainable underwriting losses and have caused the reinsurance market to harden.

The combination of losses sustained because of both man-made and natural disasters and an ever-tightening reinsurance market have resulted in multiple high-profile insurer insolvencies and hundreds of thousands of Florida insurance policies being cancelled or nonrenewed.

Greenberg Traurig explore the natural and man-made catastrophic risks inherent in Florida which have contributed to creating very challenging property insurance markets in the world. We also discuss measures that Florida’s leaders have undertaken to address these issues and help support the struggling market (see Natural Catastrophe insurers losses Outlook).

Insurance reforms in Florida

AM Best is of the view that the insurance reforms passed in Florida’s most-recent legislative special session will lead to much-needed relief to the state’s homeowners market. However, in the near term, capacity will remain limited with high reinsurance costs.

A new Florida law and proposals have the potential to reduce the cost of homeowners insurance in the state, according to the Insurance Information Institute (Triple-I).

“Reforms put in place in the closing weeks of 2022 and proposed in the first quarter of 2023 suggest Florida is now quite serious about fixing the fraud and legal system abuse that have contributed to the state’s insurance crisis,” stated Addressing Florida’s Property/Casualty Insurance Crisis, a Triple-I Issues Brief which built on one Triple-I released about Florida’s homeowners insurance market in August 2022.

It will take years for the impacts of fraud and legal system abuse to be wrung out of the system and for policyholders to experience premium benefits.

Job 1 is to “stop the bleeding” as insurers fail, leave the state, or stop writing critical personal lines coverages like auto and homeowners.

Insurance reforms in Florida will lead to relief of homeowners insurance market. The new laws include the elimination of assignment of benefits and the one-way attorneys’ fees rule for property claims and reduces the amount of the time to 18 months in which a supplemental claim can be filed.

Should the measures eliminating assignment of benefits and one-way attorneys’ fees for property claims prove effective, they could materially lower insurers’ defense and cost containment expenses.

Additionally, the reduction in the amount of the time to file a supplement claim could alleviate concerns in the insurance-liked securities market about capital becoming trapped for long periods.

Man-made disasters

The Florida legislature has attempted, several times, to address Florida’s property insurance issues. In 2019, the legislature passed SB 7065 addressing abuses related to assignment of benefits under property insurance contracts.

Later in 2021, the legislature passed SB 76, which implemented new notice requirements related to litigation, addressed attorney’s fees in a limited manner, and reduced claims filing deadlines. The measures were helpful but did not fully address the issues caused by fraud and abuse.

To address the growing problems affecting the Florida insurance marketplace, Ron DeSantis, governor of Florida, called a special session of the Florida legislature in May 2022, during which the legislature passed Senate Bill 2D, which included additional provisions aimed at litigation reform.

Senate Bill 2D also aimed to provide relief to Florida insurers from the hardening reinsurance market by creating the Reinsurance to Assist Policyholders Program, which authorised a $2bn dollar reimbursement layer of reinsurance for hurricane losses directly below the mandatory layer of the Florida Hurricane Catastrophe Fund.

Subsequently, on 28 September 2022, Hurricane Ian made landfall on Florida’s Lee Island Coast. The storm produced winds of over 150 miles per hour and caused massive flooding across the state.

It is estimated that Hurricane Ian inflicted over $50bn in damage on the state, striking yet another blow to the Florida property insurance market.

Soon thereafter, the legislature met in December for its second special session of 2022 and passed Senate Bill 2A, which many industry experts regarded as the most significant property insurance reform bill in recent history.

The bill strengthened Florida’s property insurance market by eliminating one-way attorney fees for property insurance claims, which was the driving force incentivising unscrupulous contractors and their attorneys to file frivolous lawsuits in defence of largely inflated or fraudulent property insurance claims.

Other key aspects of Senate Bill 2A included:

- enhancing the authority of the Florida Office of Insurance Regulation to conduct market conduct examinations of property insurers following a hurricane to hold insurance companies accountable and prevent abuse of the property appraisal process;

- reducing timelines for insurers to process payments and get funds back into the hands of policyholders as they rebuild their lives;

- building on reforms passed earlier in 2022 by committing additional funds to provide temporary reinsurance support and help stabilise the marketplace.

Additionally, the legislature passed Senate Bill 4A, which provided property tax relief for homes rendered uninhabitable due to recent storms.

The bill provided $750m for the communities impacted by Hurricanes Ian and Nicole, including $350m to support the entire portion of local government match for Federal Emergency Management Agency (FEMA) Public Assistance, freeing up local funds to undertake additional hurricane recovery and mitigation projects and $150m to the Florida Department of Environmental Protection to support local beach renourishment projects and a new Hurricane Restoration Reimbursement Grant Program.

Natural catastrophe risk

While we do not see a new norm of higher loss growth rates, regular occurrence of multi-billion insured loss outcomes from secondary peril events is new.

In 2021, two separate secondary perils events – winter storm Uri in the US and devastating floods in central-western Europe in July – each caused losses in excess of $10 bn.

Traditionally secondary perils have been less well monitored than primary. Recent efforts to change this should be further progressed.

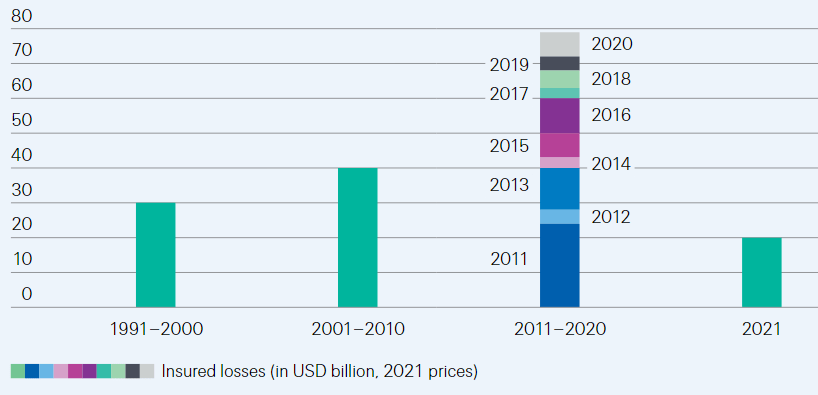

Flood affects more people around the world than any other peril. Losses from flood have been on an upward trend globally and at a significantly faster pace than global GDP. Through 2011 to 2020, at near USD 80 billion, cumulative insured losses from flood events around the world were almost double that of the previous decade. The flood experience of 2022, with insured losses at USD 20 billion, indicates no let up of the upward trend.

Florida officials have also sought to better prepare the state to withstand the effects of increased natural disasters. In recent years, Florida lawmakers have implemented historic investments to ensure communities are prepared for rising sea levels and flooding.

For example, during the 2022 legislative session, lawmakers passed House Bill 7071, ‘Home Hardening and Other Tax Breaks for Floridians’.

The law includes the ‘Home Hardening’ initiative, which provides sales tax relief to homeowners to harden their homes from storms.

The bill also includes an abatement of all property taxes for owners of surfside condominiums, pro-rated refunds of property taxes on residential properties rendered uninhabitable by a catastrophic event for at least 30 days, a sales tax reduction on new mobile homes and several sales tax holidays.

In the same session, lawmakers passed House Bill 7053, ‘Coordination of Flooding and Sea-Level Rise Resilience Efforts’.

The law establishes the Statewide Office of Resilience within the Governor’s Office, with a governor appointed chief resiliency officer. It also sets a minimum of $100m in funding to be identified annually in a comprehensive and ranked list of resilience projects.

Mindful of last summer’s tragic incident involving the collapse of the Champlain Towers, legislators passed Senate Bill 4D, ‘Building Safety’.

Senate Bill 4D originally only made changes to the building code relating to roof replacement requirements.

However, the scope was expanded to include policy changes related to condos and condo associations. The bill amends the Florida Building Code to provide that when 25% or more of a roofing system or roof section is being repaired, replaced or recovered, only the portion of the roofing system or roof section undergoing such work must be constructed in accordance with the current Florida Building Code in effect at that time.

Senate Bill 4D, which addresses roof repairs as it relates to property insurance, was amended to include condo safety recommendations which largely mirror stronger structural and building safety measures outlined by the Surfside Working Group’s Florida Building Professionals Recommendations.

Global insured losses from flooding

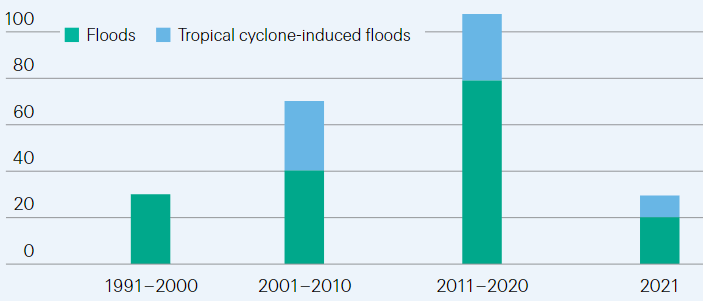

Insured flood losses are on the rise, with most of the global flood insurance losses recorded in the last two decades. Accumulating economic wealth, growing populations, poor defence infrastructures and climate-change effects are driving the increase. Even so, in the last decade flood events counted for just 10% of insured losses from all natural catastrophes. This is a reflection of low flood insurance penetration in both emerging and advanced economies.

Global insured flood losses, including estimated flood damage due to tropical cyclones

Floods can be secondary effects of tropical cyclones that spark storm surges and/or heavy rains, leading to large-scale inland flooding. With limited information available, we estimate that over the last 20 years, flooding as a secondary effect of tropical cyclones added around 30% to the global insured losses from pluvial and fluvial flood events.

Looking to the future

Florida is regarded as one of the most difficult property insurance markets in the world, which is largely attributed to the prevalence of natural disasters such as catastrophic hurricanes and flooding.

In fact, a main factor driving up property insurance and reinsurance rates in Florida is fraud. Most observers can agree the market is at a critical inflection point, and action must be taken to address these challenges.

Efforts by Mr DeSantis, the legislature, and the Florida Office of Insurance Regulation to address the fraud by eliminating one-way attorney fees and reforming the manner in which property insurance claims are adjudicated may help to address the problem and bring much-needed relief to Florida insurance consumers, but there will likely always be people looking to game the system.

The legislature is expected to focus on property insurance heavily in the 2023 regular legislative session. In that regard, Florida lawmakers have an opportunity to transform a struggling insurance marketplace which supports one of the most desirable and vibrant property markets in the world. Those of us who live and breathe in this market will be watching closely to see if the legislature will continue to build on the efforts taken in December 2022.

Natural catastrophe & disaster FAQs

What is a natural catastrophic event?

A natural catastrophe is an unexpected event, caused by nature, such as an earthquake or flood, in which there is a lot of suffering, damage, or death.

What is an example of a natural catastrophe?

Various phenomena like earthquakes, landslides, volcanic eruptions, floods, hurricanes, tornadoes, blizzards, tsunamis, cyclones, wildfires, and pandemics are all natural hazards that kill thousands of people and destroy billions of dollars of habitat and property each year.

What is the most catastrophic natural disaster?

From 1980 to July 2022, the tsunami caused by an earthquake in the Indian Ocean in December 2004 was the deadliest natural disaster in the world. The exact death toll is impossible to calculate, but it is estimated that over 200,000 lives were lost as a result of the tsunami.

Is catastrophe a natural disaster?

A natural disaster is a naturally occurring weather event that impacts a large geographical area with many people. Typically, property and infrastructure damage is on a large scale. A catastrophe occurs when inadequate forecasts are produced, evacuation of residents is not carried out and communication is lacking.

What are 3 examples of catastrophic events?

Catastrophic weather events include hurricanes, tornadoes, blizzards, and droughts, among others. As these massively destructive and costly events become more frequent, scientific evidence points to climate change as a leading cause.

What disaster is the most difficult to prevent?

Earthquakes are one of the most unpredictable and damaging disasters. The scientific community has yet to find a way to predict when an earthquake will occur with enough time to evacuate areas. Systems exist, but they can only give a few minutes warning to residents that a disaster is on its way.

…………………………..

AUTHORS: Fred E. Karlinsky – Shareholder, Co-Chair Insurance Regulatory & Transactions Practice at Greenberg Traurig, Timothy F. Stanfield – Shareholder with the Florida Government Law & Policy Practice at Greenberg Traurig, Christian Brito – Associate at Greenberg Traurig

Fact checked by Oleg Parashchak