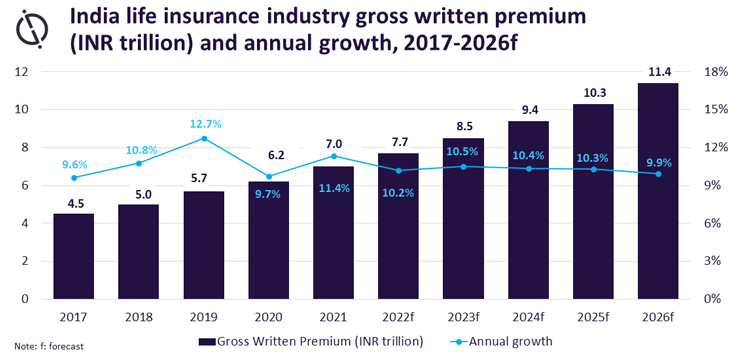

India’s life insurance market is expected to grow at a compound annual growth rate (CAGR) of 10.3% through 2026, driven by growing awareness and positive regulatory landscape.

According to analysts at GlobalData, it is forecasted to grow from $92.3 billion in 2021 to $150.6 billion in 2026, in terms of gross written premiums.

In 2023 the life insurance industry is set to grow by 10.2%; driven by the development of digital distribution channels and product innovation.

The life insurance industry in India is witnessing a significant post-pandemic growth, supported by growing awareness, increasing demand for group policies, and a favourable regulatory environment.

Private insurers are also increasingly offering group life policies as an employee benefit. Such policies, where the risk pool is diverse leading to lower premiums, are cost-effective employee retention measures.

GlobalData analysts observed that, during the last few years, Indian life insurers have witnessed strong growth in the sales of group life insurance policies.

The Life Insurance Corporation of India (LIC), the largest life insurer in the country, with 63.2% market share, recorded 12.7% growth in group life premiums in FY2021 while individual life premiums declined by 2.8%.

Another factor that has supported the growth of the industry in the country, is the government’s push to increase life insurance penetration by selling life products to low-income customers through Pradhan Mantri Jeevan Jyoti Bima Yojana.

Positive regulatory developments have supported product innovation in the life insurance industry. For example, IRDAI relaxed product approval with the expansion of the ‘Use and File’ process to include life products. Earlier, under the ‘File and Use’ policy, life products required regulatory approval before their launch.

Life insurers in India have also been focusing on strengthening digital distribution channels.

According to GlobalData, the Covid-19 pandemic has compelled insurers to develop and increase the digital distribution of their products and gain direct control of customer relationships.