Overview

Many small and medium-size are underinsured, especially smaller and newer businesses. And commercial customers who have been loyal to one provider are more willing to switch than ever.

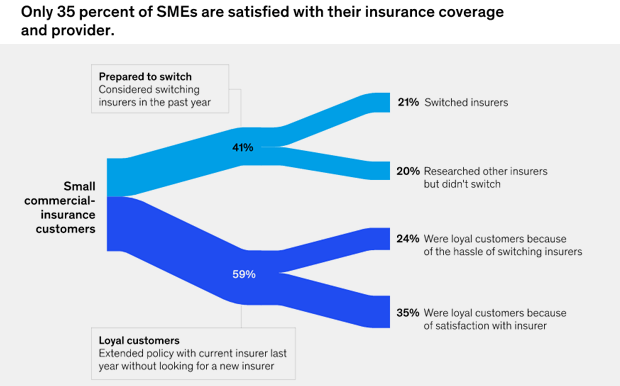

In McKinsey survey of SMEs, only about 1/3 of respondents said they were completely satisfied with their current insurance coverage. Fortunately, there is a great deal of flexibility when it comes to providing the simplified products and processes that SMEs are calling for.

Many existing products, for example, are far too complex to meet the needs of smaller firms. Automation, standardization, and simple segment-specific tailoring would not only boost customer satisfaction but also visibly improve efficiency.

With the right strategy, the appropriate skills, and a suitable business model, insurers can offer SMEs an attractive portfolio that better meets their needs.

The SME segment represents billions in untapped premiums

SMEs are the bedrock of most global economies, but the consequences of the COVID-19 crisis are creating waves in the sector and, in many cases, closing doors. In some countries, SMEs remain afloat thanks to generous financial assistance.

It is unclear, however, how many of those companies will file for insolvency in the coming months and years, or how many business concepts will never come to fruition because of the strain of COVID-19 on potential entrepreneurs.

Whatever the outcome, this changing SME landscape provides impetus and gives insurers new opportunities to expand their portfolios and tailor them to SMEs.

Take the SMEs market have long been a core segment for composite insurers; they accounted for 60 to 65% of all commercial and industrial premiums.

The future holds even more potential: commercial insurance has enjoyed an average annual growth rate of 2.9%. And while just 7% of medium-size enterprises reported gaps in their insurance coverage, 1/3 of the smallest firms identified outstanding insurance needs.

According to McKinsey estimates, the untapped market potential (in terms of annual premiums) of underinsured small enterprises and microenterprises in Germany alone could be up to €2 billion. That’s the equivalent of one-tenth of that market’s total premiums today.

Insurers’ SME options are broad and varied

So how can insurers capture these billions in potential? There are several key options that are effective in Germany and could prove instructive for insurers serving similar global markets across Europe, North America, and Asia.

Differentiate for small but sophisticated customers

SMEs represent an extremely heterogeneous target group for insurers: they vary in size and standing, business area, and insurance needs and preferences. These factors make segmentation the key to conquering this sector.

Company size and standing

As in many developed nations, the SME market in Germany is broad and diverse: the segment includes one-person operations as well as major medium-size firms with revenues in the tens of millions.

Catering to this range of needs is challenging but worth every effort because SMEs account for 45% private-sector revenue.

Moreover, a company’s standing and maturity matter. Newer businesses are often underinsured, but they are also subject to fewer risks. As they grow in size and complexity, that initial lower need for insurance products changes.

Business area

Different types of businesses carry different types—and severities—of risk. Industry cycles also play a role, a fact that became even more evident during the COVID-19 pandemic. Economic-recovery simulations carried out by McKinsey have shown considerable divergence in how long individual sectors will need to return to pre-COVID-19 form.

Fintechs, for example, will rally very quickly, while the travel and hospitality sector will take far longer to recover from the consequences of the crisis. Insurers can incorporate these different recovery processes into their strategic decision making.

Customer expectations and preferences

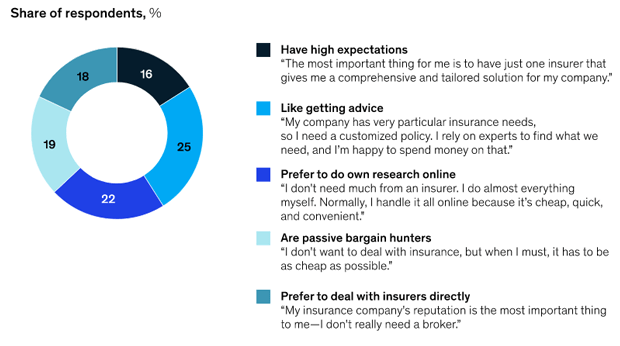

Depending on industry, size, and financial situation, SMEs have extremely different insurance requirements. Based on data survey of 1,400 SMEs, McKinsey has identified five customer segments with distinct expectation profiles and preferences.

Traditionalists who like getting advice make up the largest group at 25%, though their counterparts—those who prefer to do everything online on their own—come in a close second.

Insurers can build profitable customer relationships with each of these archetypes through the appropriate products, services, and channels.

SME policyholders fall into 5 customer segments

Develop long-term customer loyalty

The majority of SMEs are loyal customers—but not for much longer. The survey revealed that 41% of customers have already researched alternatives, and around half have switched to a different insurance carrier. Most of those switches, however, are related to auto insurance—a product that is traditionally beset by high turnover.

It is not unusual for a company’s risk landscape and business situation to evolve over time—though sometimes this evolution happens abruptly and radically, such as during the COVID-19 crisis. These progressions warrant changes in insurance coverage. For insurers, it is vital to detect this need as early as possible.

In-depth monitoring of potential triggers for switching not only helps prevent turnover but also delivers valuable information on how to address customers’ newly emerging needs.

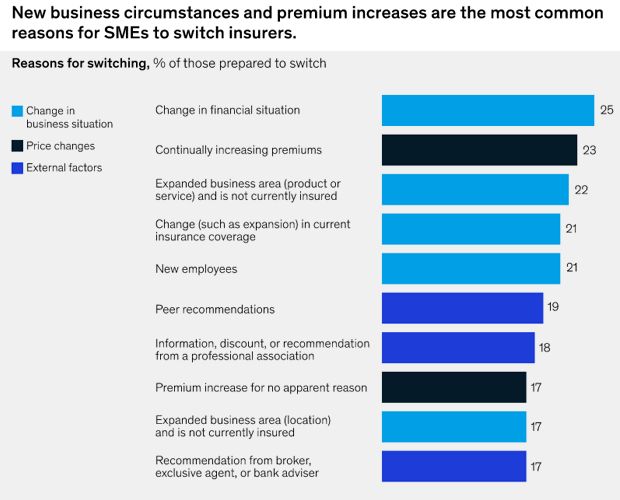

The underlying reasons for switching throughout the segment largely fall into three categories, according to the survey: business situation, premium increases, and external factors.

While switching because of increased premiums is to be expected, many SMEs are also switching because they are looking to expand into new business areas and hire more employees.

These triggers are relevant because they change a company’s risk profile; as a result, insurers must update old ways of working and search for alternative providers and solutions to match these new risk landscapes.

Having the latest data is essential to developing long-term loyalty among SME customers. Insurers and their sales teams should work to continuously improve the customer experience by communicating regularly with policyholders, promptly identifying changes in their business situations, and responding with fitting solutions. Satisfied customers both foster stable portfolios and are effective multipliers when it comes to generating new business through word-of-mouth referrals and online reviews.

7 proven business tactics

To seize the opportunities presented by the SME segment, some pioneering insurers are relying on a raft of success factors covering all possible dimensions of this market—from specific strategies to designing outstanding customer experiences.

- Align the target segment and objectives to company strategy. There are many available SME market opportunities—and the right choice will depend on an insurer’s strengths. The commercial insurance segments that align with an insurer’s core strategy will be the best fit. Insurers will also want to set concrete goals aligned to their strategy, whether those are to increase the number of policies in the portfolio, to propel growth in gross premiums written, to widen profit margins, or to improve customer retention.

- Think like a customer. All SME insurers should aim to serve not only as one-time claims adjusters or sales contacts but also as trustworthy supporters throughout the entire insurance customer journey. Doing so can improve customer loyalty and thereby garner new business while enabling insurers to respond to changes in risk more quickly. For insurers, this means that investing in customer experience is an investment in their own growth.

- Tailor product portfolios to target customers. As soon as target customers have been selected according to an insurer’s strategy, the product portfolio needs to be revised to offer optimum service to policyholders. Constant monitoring of changes in customer needs is vital and should be followed by implementing the relevant product modifications.

- Build and expand technical excellence. Heavily heterogeneous SME risks call for modern price and risk models. In Germany, many insurers still base their pricing on the simplified SME claim-data model published by the German insurance trade association rather than investing specifically in their own capabilities and actuarial and analytical resources. Insurers should instead draw on market-based SME pricing models from public sources, enrich these with external data sources, and rapidly integrate with new digital sales channels (such as software for brokers and agents). The latter form the basis for real-time tariff updates and for capturing real market data in the form of price quote databases that insurers can—and should—use to further improve internal models.

- Activate and digitalize sales channels. The increasingly digital nature of brokers, pools, and aggregators makes it necessary for insurers to sell some of their SME products through third-party providers of price comparison or underwriting software. For this to work, insurers must integrate with external APIs, use market standards (such as standardized APIs), and build or maintain IT architectures that digitally support external third-party providers. At the same time, insurers must invest in digital solutions for their own channels (such as brokers, contact centers, and direct sales). If brokers and aggregators can provide quotes in real time, this should also be an option for the agent and direct sales channels. Given the broad spectrum of SME customers, insurers can also benefit from continuous investment in the development and product training of their own sales teams.

- Offer seamless customer journeys. Some SMEs already expect a fully digital service, while others are not quite there yet. Now is the time to deliver a customer journey that supports online and offline contact points, depending on the customer’s preference. This requires thoughtful design of the entire customer experience, including all sales and service channels—whether web-based, app-based, or based on phone calls—and a review of product and pricing strategy to ensure parity among channels.

- Drive innovation. Competition is bound to intensify. Aggregators and new sales tools will offer greater transparency for a traditionally opaque market. Insurers will have to counter the resulting pressure on average premiums and the claims ratio through a radical redesign of their processes and a well-supported culture of continuous improvement.

Strategic clarity, customer orientation, and operational excellence are essential to successfully tackle the heterogeneity and resulting complexity in the SME segment.

New digital processes and differentiated data about customers and risks will help map complexity in the segment to form an innovative business model. In view of the long-standing neglect of this segment and the likelihood of an increasingly dynamic postpandemic market, the opportunities for determined early movers are better than ever.

………………………..

AUTHORS: Stephan Binder – senior partner in McKinsey’s Zurich office, where Philipp Horsch is an associate partner; Johannes-Tobias Lorenz – senior partner in the Düsseldorf office; Felix Schollmeier – partner in the Munich office.