Overview

The US P&C insurance industry continued to generate significant underwriting losses despite strong premium growth. Results are anticipated to improve in 2024 as pricing increases continue to take hold, but uncertainty remains regarding future catastrophe losses, effects of inflation on loss costs, and loss reserve experience.

According to Fitch Ratings research, sector outlook on US P&C insurance is Neutral, with results expected to be stable to improving, with a gradually emerging recovery in personal auto, continued stability in commercial lines underwriting and investment income growth.

The industry will be hard pressed to match the 102.8% combined ratio (CR) posted in FY

Higher natural catastrophe losses and a lack of improvement in personal auto results drove the industry underwriting CR to 104.4% in 6M2024, compared with a 100% CR at mid-year 2024.

Insured natural catastrophe losses are estimated at between $105 bn and $120 bn, according to several sources, making it the third highest natural catastrophe loss year since 2011.

Insured losses from major natural catastrophes in the second quarter of 2024 are estimated to be less than $10 bn.

WTW reports that property insurance premiums will continue to rise throughout 2024, but these increases will mostly be driven by inflation raising insurable values, as opposed to rate increases. No single event caused this upswing, but rather an accumulation of catastrophes, which included hurricanes, floods, tornados and freezes, well exceeded the $70 bn average annual loss since 2011.

P&C industry net statutory earnings

P&C industry net statutory earnings declined to $9 bn in 1H, corresponding with a 1.8% annualized return on surplus. Statutory earnings fell 73% YoY, and 63% excluding a one-time $10.8 bn investment distribution to a Berkshire Hathaway insurance subsidiary.

Industry policyholders’ surplus increased by 5.4%, again exceeding $1 trillion, despite the sharp drop in earnings as the equity market recovery contributed to large unrealized investment gains.

P&C Industry Statutory Performance Highlights

| $ bn | 2024 | Change |

| Loss Ratio | 78.7% | 5.1% |

| Expense Ratio | 25.3% | -0.6% |

| Dividend Ratio | 0.3% | -0.1% |

| Combined Ratio | 104.4% | 4.4% |

| Return on Surplus | 1.8% | -4.7% |

| Net Written Premiums | 417.4 | 8.0% |

| Underwriting Gain Excl Policy Divs | (24.0) | 275.8% |

| Investment Income | 33.5 | -12.6% |

| Realized Investment Gains | 2.3 | -37.0% |

| Policyholders’ Surplus | 1,043.8 | 8.1% |

| Net Income | 9.0 | -72.5% |

P&C insurance written premium growth

Written premium growth remains highly positive with direct written premiums (DWP) increasing by 8.6% and net written premiums 8% YoY.

Sharp increases in auto and homeowners premium rates in many jurisdictions led to personal lines DWP increasing by 11% for the period, while commercial lines DWP was up 6%, a reduction from the growth rates reported in 2024 and 2022.

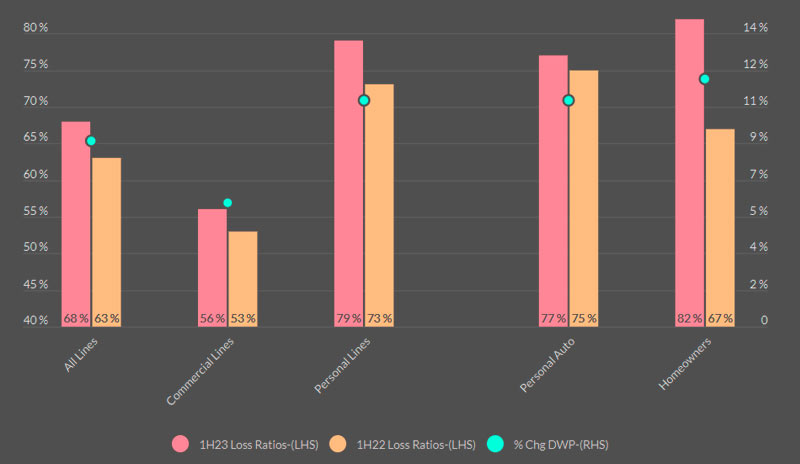

Industry reported direct loss ratios by segment show ongoing sharp divergence in underwriting results for personal lines versus commercial lines.

The personal insurance lines direct loss ratio rose by 6 percentage points YoY to 79% at 6M. The increase is in large part due to a 15 point increase in the homeowners loss ratio to 82% tied to higher catastrophe losses.

P&C Industry Statutory Direct Loss Ratios

The personal auto loss ratio

The personal auto loss ratio also remains elevated at 77% compared with 75% at 6M, despite substantial pricing and underwriting actions taken by carriers. Unfavorable loss severity patterns in physical damage and bodily injury coverages, as well as higher litigation related costs, continue to plague this line.

Personal auto results are poised to improve as CPI data indicates a 19% increase in US auto insurance rates, and loss severity trends are moderating, but a return to broader underwriting profits may still take some time.

Homeowners writers face challenges in managing aggregate catastrophe exposures in a more restrictive and costly reinsurance market, as well as properly insuring properties to value in a high inflation environment.

In contrast, the commercial lines sector loss ratio remains favorable with a 56% direct loss ratio in 1H2024 versus 53% in the prior year period. Product segments that are most profitable include workers compensation and other liability – claims made.

Industry Combined Ratios Increased to 104% in 2024 vs 100% in 2022

Commercial lines are positioned to maintain favorable underwriting results through 2024, but future performance is reliant on pricing actions keeping pace with loss cost trends, which will prove challenging under more volatile economic conditions.

Top 15 US P&C Insurers Combined Ratios

| Insurer | 2024 | % DWP Personal Lines |

| Berkshire Hathaway | 91% | 67% |

| Chubb | 92% | 15% |

| The Hartford | 94% | 20% |

| Progressive | 99% | 83% |

| AIG | 100% | 7% |

| Travelers | 101% | 38% |

| Auto-Owners | 106% | 54% |

| Liberty Mutual | 109% | 54% |

| Farmers Insurance | 114% | 81% |

| Allstate | 114% | 93% |

| USAA | 115% | 94% |

| Nationwide | 116% | 51% |

| State Farm | 116% | 92% |

| American Family | 117% | 84% |

| Erie Insurance | 121% | 70% |

| P&C Industry | 104% | 50% |

Industry statutory results contrasts with performance compiled for 40 GAAP reporting entities in Fitch’s recent report, as this group had an aggregate 97.1% CR and an 8.4% operating ROE for 2024.

The higher proportion of personal lines business written by several large mutual insurers greatly influences US statutory industry aggregate performance relative to the GAAP universe.

The 2024 statutory underwriting results for the 15 largest US underwriters reveals five mutual or reciprocal insurers with a 115% or higher 6M CR. Four large publicly traded underwriters posted a CR below 100% for the period.

FAQ

The industry faced higher natural catastrophe losses and ongoing challenges in the personal auto sector. This pushed the underwriting combined ratio (CR) to 104.4%, up from 100% in mid-2024, despite robust premium growth.

Insured natural catastrophe losses were estimated at $105 bn to $120 bn in 2024, the third-highest year since 2011. Hurricanes, floods, tornados, and freezes contributed significantly, surpassing the average annual loss of $70 bn since 2011.

According to Fitch Ratings, the outlook is neutral but stable to improving. Personal auto insurance is gradually recovering, commercial lines remain stable, and investment income is growing. However, concerns over future catastrophe losses and inflation-driven costs persist.

The personal lines direct loss ratio increased to 79%, driven by a 15-point rise in the homeowners loss ratio due to higher catastrophe losses. In contrast, commercial lines had a favorable loss ratio of 56%, down from 53% the previous year, with workers’ compensation and liability lines performing well.

The personal auto loss ratio remained elevated at 77%, affected by severe physical damage, bodily injury costs, and increased litigation expenses. While pricing and underwriting actions are helping, and CPI data shows a 19% increase in auto insurance rates, full recovery to profitability may take time.

Homeowners insurers are grappling with managing catastrophe exposures in a costly and restrictive reinsurance market. Additionally, high inflation is making it difficult to ensure properties are insured to their correct value.

In 2024, the top 15 US P&C insurers had varying CRs. Companies like Berkshire Hathaway and Chubb posted favorable CRs of 91% and 92%, respectively, while insurers like Allstate and State Farm had higher CRs at 114% and 116%, driven by their larger personal lines business.

……………………..

AUTHORS: James Auden, CFA – Managing Director, North American Insurance Fitch Ratings, Christopher Grimes, CFA – Senior Director Fitch Ratings, Laura Kaster, CFA – Senior Director, Fitch Wire North and South American Financial Institutions